Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- FX rate a focus as ECB expected to 'recalibrate' policy

- Sterling sags as No Deal becomes odds-on with the bookies

- European curves bull flatter, Treasuries a touch higher but within ranges

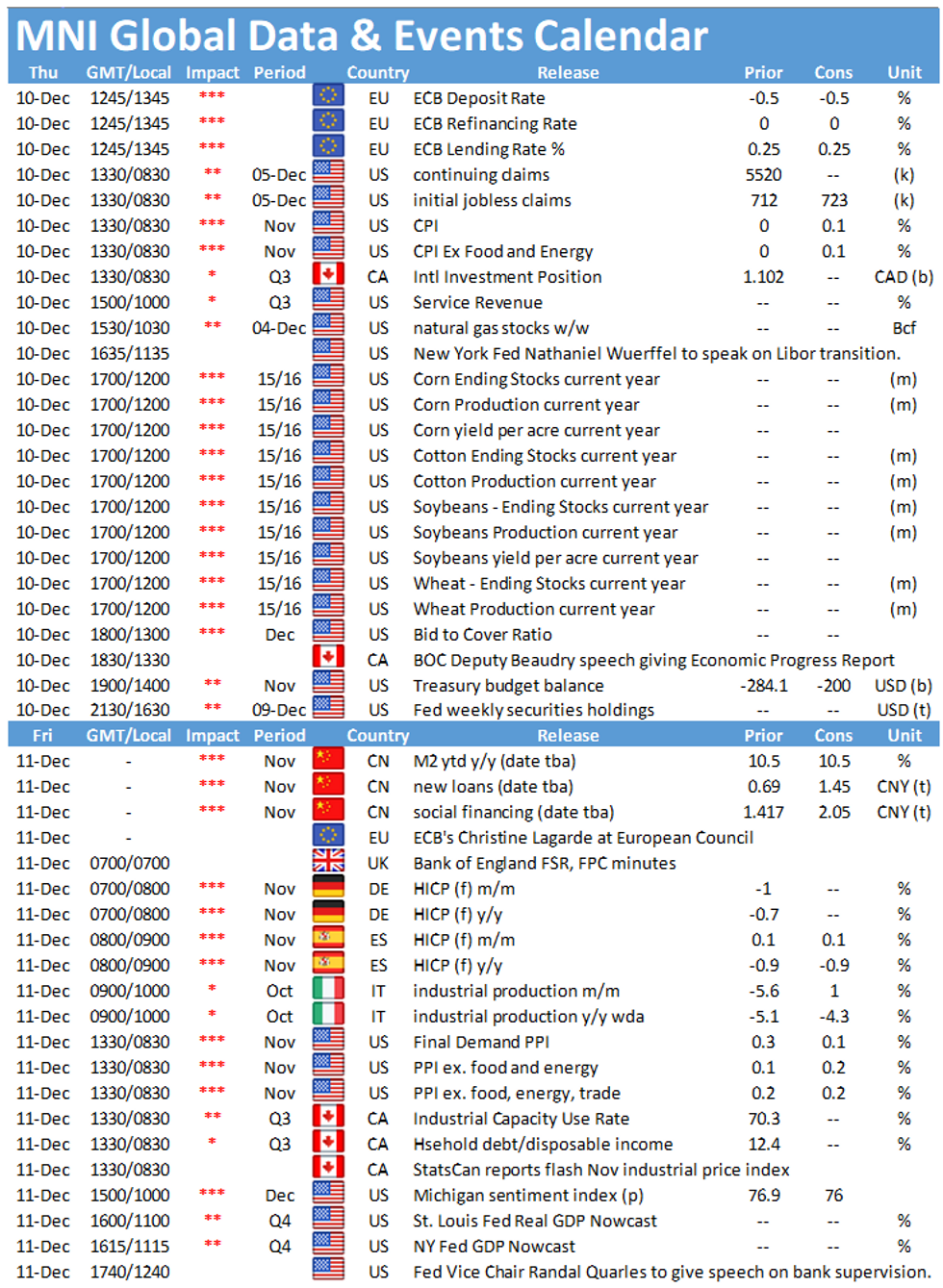

US TSYS SUMMARY: Higher But Rangebound, Attention On Frankfurt And D.C.

Tsys caught a brief bid in the Asia-Pac session with Brexit concerns at the fore, but eased off and went rangebound in early European hours as equities came off the lows.

- Mar 10-Yr futures (TY) up 4/32 at 137-24 (L: 137-21.5 / H: 137-25.5), sub-par volumes (~195k). The 2-Yr yield is down 0.4bps at 0.1449%, 5-Yr is down 1.1bps at 0.3925%, 10-Yr is down 1.3bps at 0.9229%, and 30-Yr is down 1.5bps at 1.6696%.

- Immediate attention is on the European Central Bank decision at 0745ET, presser 0830ET.

- The latter coincides with a solid U.S. data release: jobless claims alongside Nov CPI.

- In Washington, the Senate could vote today to approve the 1-week gov't funding extension that the House passed yesterday. Otherwise we still await progress on a COVID relief deal, with a gap to be bridged somewhere between Treas Sec Mnuchin's $916B proposal and the bipartisan group's $908B proposal (which that gap being much more complex than $8B).

- Some attention also on the FDA advisory committee meeting on approving the Pfizer/BioNTech COVID vaccine, goes all day (0900-1800ET), and on Congressional Oversight Commission hearing on CARES Act (1000ET).

- In supply: $65B of 4-/8-week bills at 1130ET, with $24B 30-Yr Bond auction at 1300ET. NY Fed buys ~$3.625B of 7-20Yr Tsys.

EGB/GILT SUMMARY: Curves Bull Flatter, With Gilts Leading

European sovereign curves have bull flattened this morning, with gilts leading the charge.

- Gilt yields are 3-9bp lower on the day with the long-end of the curve outperforming. The 2s30s spread is 4bp narrower.

- Bunds have similarly firmed and the curve has bull flattened. Last yields: 2-year -0.7872%, 5-year -0.8086%, 10-year -0.6230%, 30-year -0.2067%.

- OATs trade broadly in line with bunds. Cash yields are 1-2bp lower.

- BTPs have slightly outperformed core EGBs and the curve has flattened.

- Further ratcheting up tension ahead of the Brexit, the EU has published its contingency plans in the even of a no- deal outcome.

- UK monthly GDP for October came in above expectations (0.4% M/M vs 0.0% survey) alongside a better than expected outturn for industrial production and a slight miss for the index of services. French industrial production for October also surprised higher (1.6% vs 0.4% survey).

- Supply this morning came from Italy (BTPs, EUR5.75bn), Spain (Obli/ObliEi, EUR1.40bn) and Ireland (Bills, EUR0.75bn).

ITALIAN AUCTION RESULTS: Italy Sells E5.75bn of BTPs Vs E4.75-5.75bn Target

- E2.75bn of the 0% Jan-24 BTP: Average yield -0.30% (-0.19%), bid-to-cover 1.41x (1.41x), pre-auction mid-price 100.88

- E3.00bn of the 0.95% Sep-27 BTP: Average yield 0.19% (0.45%), bid-to-cover 1.40x (1.58x), pre-auction mid-price 104-98

SPANISH AUCTION RESULTS: Spain Sells E1.4bn of Obli/ObliEi Bonds Vs E0.75-2.25bn Target

- E0.921bn of the 1.25% Oct-30 Obli: Average yield -0.027% (0.22%), bid-to-cover 3.05x (3.16x), pre-auction mid-price: 112.19

- E0.482bn of the 0.65% Nov-27 ObliEi: Average yield -1.147% (-0.78%), bid-to-cover 1.92x (1.74x), pre-auction mid-price: 112.3.00

FOREX: Sterling Sags as Yet Another Deadline Looms

Following the lack of any material breakthrough over last night's dinner between the UK PM & EU's von der Leyen, GBP is the poorest performing currency in G10 as the market re-focuses on the next deadline of Sunday evening, at which time leaders on both sides will have to reach a decision over whether trade talks will continue or not, leaving a No Deal end to the transition period a very real prospect.

While GBP is weaker, it still trades north of the Monday lows of 1.3225, which should provide solid support going forward.

Antipodean currencies outperform, with AUD, NZD higher against most others. JPY, USD trade on the backfoot after a solid Tuesday showing.

Focus turns to the ECB rate decision, at which the central bank are seen recalibrating their policy toolkit.

FX OPTIONS: Expiries for Dec10 NY cut 1000ET (Source DTCC)

EUR/USD: $1.1800-10(E1.4bln), $1.1900-05(E1.0bln), $1.2000(E572mln), $1.2045-60(E1.1bln)

USD/JPY: Y103.50-60($1.3bln), Y104.00($836mln), Y104.25-35($898mln), Y104.90-105.00($1.2bln), Y105.35-40($661mln), Y105.50-55($838mln), Y105.75-85($1.4bln)

EUR/GBP: Gbp0.8890-00(E532mln), Gbp0.8970(E847mln), Gbp0.9075(E579mln)

AUD/USD: $0.7270-80(A$1.2bln), $0.7400-05(A$1.1bln), $0.7430(A$533mln), $0.7495-00(A$771mln)

AUD/NZD: N$1.0660(A$590mln)

USD/CNY: Cny6.50($904mln-USD puts), Cny6.60($1.4bln-USD puts), Cny6.70($726mln)

TECHS: Price Signal Summary - Gilts Hurtle Through 135.00

- EU FI technical conditions remain bullish.

- Bund (H1) is testing above 178.38, 76.4% of the Nov 4 - 11 sell-off. A clear break would open 178.55, Nov 9 high

- Gilts (H1) gapped higher at the open and cleared the 135.00 handle. This opens 135.67 next, the 1.236 projection of the Nov 11 - 30 rally from the Dec 2 low.

- Treasuries (H1) are unchanged and maintain a softer stance. Support and the downside trigger at 137-07+, Dec 4 low remains exposed.

- In FX, Sterling volatility remains the order of the day. Initial directional parameters in Cable are unchanged. Resistance is at 1.3539, Dec 7 and 1.3225, the Dec 7 low. EURGBP technical readings remain bullish despite this week's price swings. The key support to monitor is 0.8953 today, the former trendline resistance drawn off the Sep 11 high.

- On the commodity front, Gold key support lies at $1822.5, Dec 7 low. A break would signal scope a deeper pullback. Potential remains for gains to the $1888.9 level, 61.8% retracement of the Nov 9 - 30 sell-off. Brent (G1) bullish objectives are set at $50.00 and $50.45, 61.8% of Jan - Apr sell-off (cont). WTI (F1) bulls, eye $48.07, 0.764 projection of the Apr - Aug rally from the Nov 2 low.

EQUITIES: Continental Markets Buoyant, But Progress Shallow

European stocks trade at the upper end of the weekly range, with gains seen across core markets to narrow the gap with the Wednesday high. The UK's FTSE-100 outperforms, receiving a boost from the weaker domestic currency, to trade higher by 0.6%. Germany's DAX lags slightly, but still holds gains of close to 0.1% ahead of NY hours.

Across Europe, consumer staples, healthcare and energy names are outperforming, while tech and consumer discretionary sectors make up the bottom end of the table.

In US futures space, the e-mini S&P holds gains of close to 5 points, hovering just above the late Wednesday lows of 3659.50.

COMMODITIES: WTI Within $0.50 of Multi-Month High

Both WTI and Brent crude futures trade well, narrowing the gap with Friday's multi-month highs to just $0.50. Commodities more generally are faring well as equities inch higher and the weaker USD backdrop buoys prices. Further upside factors include wire reports that Chinese imports of oil for refining purposes are picking up, while while Indian demand is also holding well.

In metals space, gold and silver are marginally lower in response to the firmer outlook for equity markets. This keeps gold's spot price pinned between the 200-dma to the downside at 1808.87 and the 50-dma seen higher at 1876.62.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.