Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Bull flattening of the Treasury curve continues

- Delta variant concerns continue to mount, prompting widespread risk-off

- No notable data or speakers to distract, keeping focus on earnings

US TSYS SUMMARY: Bull Flattening Continues As 10Y Yields Hit Post-February Low

The bull flattening in the Tsy curve continued overnight, with equities lower/dollar higher on resurgent global COVID concerns. 10Y yields printed the lowest level since February (1.2452%) in the European morning as equity indices dropped sharply (EuroStoxx / FTSE -2%).

- The 2-Yr yield is down 0.6bps at 0.2156%, 5-Yr is down 2.9bps at 0.7444%, 10-Yr is down 3.8bps at 1.2519%, and 30-Yr is down 4.6bps at 1.8733%.

- Sep 10-Yr futures (TY) up 11/32 at 134-04 (L: 133-26 / H: 134-05) on elevated (~450k) volumes.

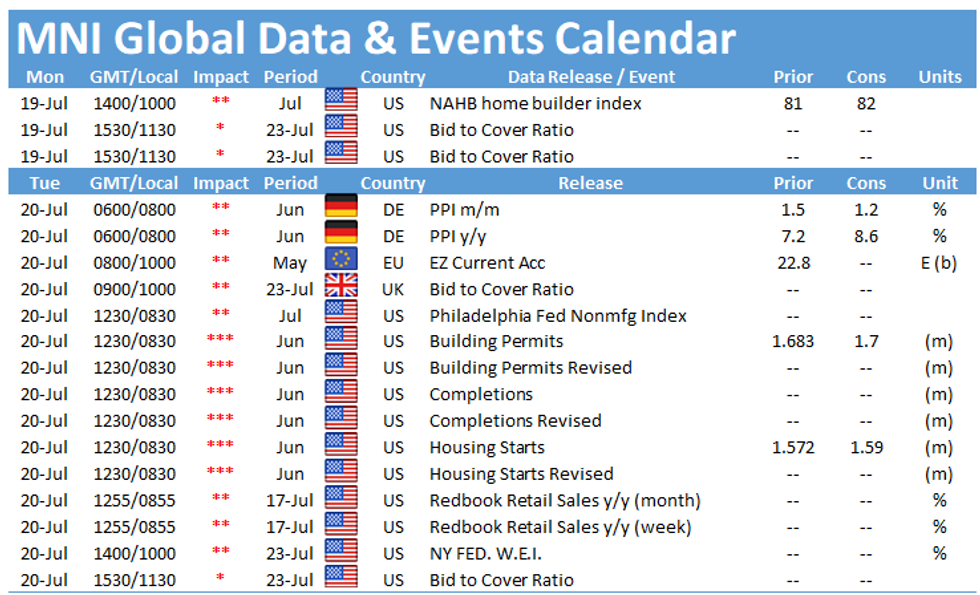

- Today's calendar is light: we're in the pre-FOMC meeting blackout period for Fed speakers, and the only data is NAHB Housing Market Index at 1000ET.

- Some attention on remarks by Pres Biden on the economic recovery at 1130ET. Also in D.C., Sen Maj Leader Schumer set to file cloture on the bipartisan infrastructure plan that would lead to a procedural vote on Wednesday. Still no firm deal yet though.

- Supply consists of $105B combined in 13-/26-week bill auctions. NY Fed buys ~$1.425B in 10-22.5Y Tsys.

EGB/GILT SUMMARY - Delta Variant Concerns Mount

Concerns about the potential impact of the spreading Delta variant on economic activity has underpinned the rally in sovereign bonds and losses for equities.

- Gilts have rallied with yields 1-4bp lower on the day and the curve bull flattening.

- Bunds have slightly lagged gilts with yields down 1-3bp and the curve 3bp flatter.

- It is a similar story for OATs with the 2s30s spread narrowing 2bp.

- BTPs have had a quieter start and trade near the Friday close.

- Despite concerns about rising infections, the UK government has persevered with its reopening strategy.

- Supply this morning came from Germany (Bubills, EUR5.55bn) and the Netherlands (DTCs, EUR2.49bn).

- There were no significant tier one data releases this morning.

- Focus this week will be on the ECB meeting, which follows the earlier than expected release of the strategy review. Although no material change to the main policy instruments is expected, some adjustment to forward guidance is possible in light of the reformulated inflation objective.

EUROPE OPTION FLOW SUMMARY

Eurozone:

3RZ1 100.12/99.75ps 1x2, bought for 2.5 in 2.1k

UK:

2LZ1 99.37c vs 0LZ1 99.50c, sold the 2yr at half in 11.5k

3LZ1 99.37c, bought for 8.5 in 3k (ref 99.225, 34 del)

US:

USU1 160/159ps, bought for 9 in 1k

FOREX: Risk Off Pervades, Boosting JPY, USD

- Stocks traded on the backfoot from the off Monday, with US futures pointing to a negative open on Wall Street later today. Downside in stocks and persistent pressure on global government bond yields have buoyed haven currencies, resulting in JPY and USD being among the strongest in G10 ahead of the NY crossover.

- As equities slip, commodities are trading poorly, resulting in WTI and Brent crude futures touching the lowest levels of the month. This has worked further against oil-tied FX, with CAD and NOK among the poorest performers of the day.

- EUR/USD downside sees the pair touch the lowest levels since April, narrowing the gap with key support and the bear trigger at the year's low of 1.1704.

- There are no major data releases due Monday, keeping focus on the central bank speakers slate. BoE's Haskel and ECB's Perrazzelli are due to speak. Earnings season continues, with healthcare, tech and communication services taking focus.

FX OPTIONS:

- EURUSD: 1.1750 (246mln), 1.1800 (430mln), 1.1805 (252mln), 1.1850 (480mln)

- EURGBP: 0.8550 (220mln)

Price Signal Summary - Equities Slip, Dollar Rallies

- In the equity space, price continues to pull away from recent highs. S&P E-minis have started the week on a softer note and the contract is extending the pullback from 4384.50 Jul 14 high. Attention turns to the key near-term support at 4279.25, Jul 8 low. EUROSTOXX 50 futures are also weaker this morning. The contract has probed 3951.50, Jul 8 low. A clear break would open 3914.00, May 20 low.

- In FX, the USD outlook remains bullish. The EURUSD needle still points south and the pair is trading lower. The focus is on 1.1704, Mar 31 low. Initial resistance is 1.1851, Jul 15 low. GBPUSD remains vulnerable and the pair has cleared support at 1.3733, Jul 2 low. This set the scene for weakness towards key S/T support and the bear trigger at 1.3669, Apr 12 low. USDJPY appears vulnerable and the sell-off on Jul 14, suggests the short-term risk remains bearish. The support to watch is 109.53, Jul 8 low and the short-term bear trigger. A break would open 109.19, Jun 7 low. AUDUSD is also sharply lower today and USDCAD has spiked higher reinforcing underlying USD strength.

- On the commodity front, Gold has pulled back from last week's high. The yellow metal maintains a bullish tone though and the pullback is considered corrective. Price however needs to clear last week's high print to confirm a resumption of the recent upleg. Key support to watch is at $1791.7, Jul 12 low. Brent futures are trading lower today and have breached support at $70.76, Jul 8 low. This signals scope for a deeper pullback towards $71.24, the Jun 17 low. WTI key support at $70.76, Jul 8 low has also been breached. This opens $67.59, Jun 2 low.

- Within FI, Bund futures trend conditions remain bullish. With 175.00 cleared, attention is on 175.88,1.236 projection of the May 19 - Jun 11 - Jun 22 price swing. Gilt futures remain below recent highs. The outlook is bullish. Key resistance is at 129.92, Jul 8 high. Key support to watch is 128.54/39, Jul 14 low and Jun 11 high and recent breakout level

EQUITIES: Energy, Financials Leading European Stocks Lower

- Stocks in Asa closedJapan's NIKKEI down 350.34 pts or -1.25% at 27652.74 and the TOPIX down 25.06 pts or -1.3% at 1907.13. China's SHANGHAI closed down 0.181 pts or -0.01% at 3539.123 and the HANG SENG ended 514.9 pts lower or -1.84% at 27489.78.

- European equities are sharply lower, with the German Dax down 294.24 pts or -1.89% at 15335.53, FTSE 100 down 123.59 pts or -1.76% at 6904.1, CAC 40 down 114.64 pts or -1.77% at 6351.19 and Euro Stoxx 50 down 81.85 pts or -2.03% at 3973.75.

- U.S. futures are being dragged down as well, with the Dow Jones mini down 350 pts or -1.01% at 34215, S&P 500 mini down 33 pts or -0.76% at 4285.5, NASDAQ mini down 62 pts or -0.42% at 14608.75.

COMMODITIES: Oil Sinks On OPEC+ Supply Deal, Broader Risk-Off

- WTI Crude down $2.06 or -2.87% at $70.64

- Natural Gas up $0.02 or +0.52% at $3.695

- Gold spot down $8.23 or -0.45% at $1806.81

- Copper down $6.3 or -1.46% at $427.75

- Silver down $0.32 or -1.25% at $25.4239

- Platinum down $26.82 or -2.43% at $1095.34

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok