Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Equities edge off highs, sit lower pre-NY

- Oil markets shows signs of stress as OPEC+ deal falls through

- US 10y yields at lowest since June 21

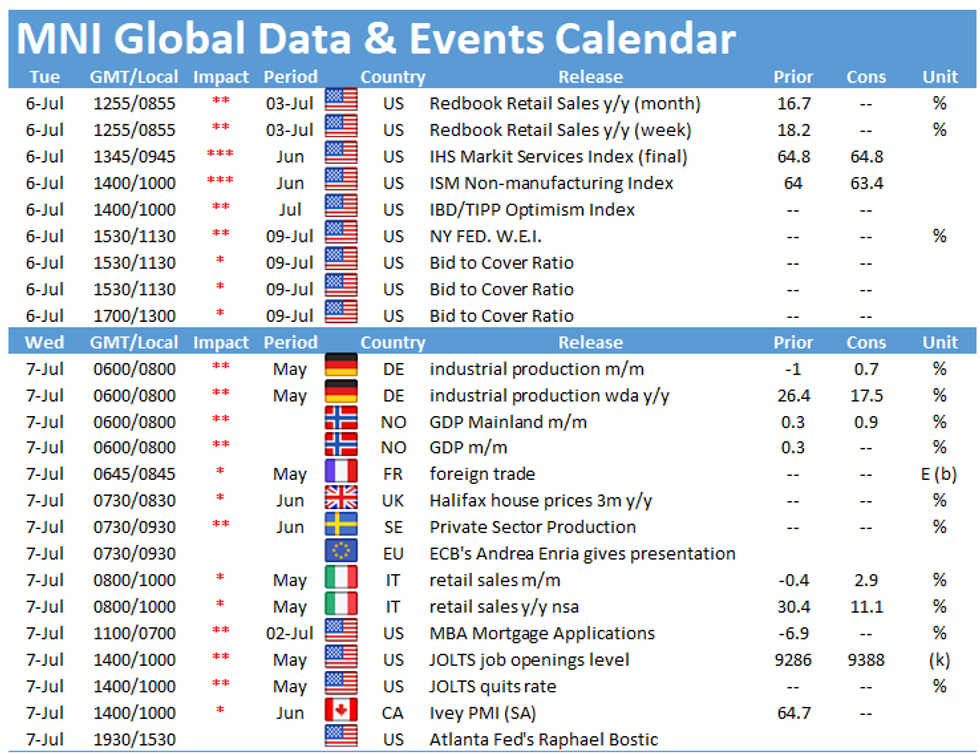

US TSYS SUMMARY: Modest Overnight Weakness Reverses, ISM Services Ahead

Tsys are mixed in the return to cash trading following the long weekend. A fairly light calendar lies ahead Tuesday.

- Modest weakness in futures Monday and overnight Tuesday reversed in European trading as equities slipped from the highs. WTI crude hitting best levels since 2014, weak German factory data, and RBA taking first steps to wind back stimulus were the major overnight talking points, though none had much impact on Tsys.

- The 2-Yr yield is up 0.2bps at 0.2357%, 5-Yr is down 0.5bps at 0.8525%, 10-Yr is down 0.3bps at 1.4204%, and 30-Yr is down 0.1bps at 2.039%.

- Sep 10-Yr futures (TY) up 3/32 at 132-24.5 (L: 132-18.5 / H: 132-26), decent volume (>360k).

- Data focus is Jun ISM Services at 1000ET, preceded by final Jun Services/Composite PMI.

- No scheduled Fed speakers ahead of the June meeting minutes Wednesday.

- In supply, $111B in 3-/6-month bills auctioned at 1130ET (and note, no supply Weds).

- NY Fed buys ~$12.425B of 0-2.25Y Tsys.

EGB/GILT SUMMARY: Bull Flattening

European sovereign bonds have traded firmer this morning and curves have bull flattened alongside broadly weaker trading in equities.

- The gilt curve has flattened with the 2s30s spread 2bp narrower.

- Bunt yields are 1-2bp lower with the long end of the curve similarly slightly outperforming.

- It is a similar story for OATs where yields have edged down 1-2bp across much of the curve.

- The UK construction PMI for June came in at 66.3 beating the 64.0 consensus.

- UK Health Secretary Sajid Javid has warned that coronavirus infections could soar to 100,000 a day once the remaining social restrictions are lifted.

- Supply this morning came from the UK (Gilts, GBP4.25bn), Germany (ILBs, EUR475mn allotted), France (Syndicated LT OAT, books last above EUR28bn), Spain (letras, EUR5.372bn), Belgium (TCs, EUR1.671bn), Austria (RAGBs, EUR1.3bn).

EUROPE ISSUANCE UPDATE

Germany allots:

E310mln 0.10% Apr-33 ILB, Avg yield -1.58% (Prev. -1.51%), Bid-to-cover 1.21x (Prev 1.02x)

E165mln 0.10% Apr-46 ILBl, Avg yield -1.38% (Prev. -1.27%), Bid-to-cover 2.13x (Prev 1.17x)

Austria sells:

E650mln 0.75% Oct-26 RAGB, Avg yield -0.50% (Prev. -0.46%), Bid-to-cover 2.82x

E650mln 0% Feb-31 RAGB, Avg yield -0.06% (Prev. -0.00%), Bid-to-cover 2.14x (Previous 2.20x)

UK DMO sells:

GBP2.75bln 0.25% Jul-31 Gilt, Avg yield 0.819% (Prev. 0.941%), Bid-to-cover 2.68x (Prev. 2.64x), Tail 0.1bp (Prev. 0.1bp)

French Syndication: Final terms for 30-year May-53 OAT

Spread set at OAT+3bps (initial guidance was OAT+5bps area)

Books above E28bln (exc JLM interest)

EUROPE OPTION FLOW SUMMARY

UK:

LU1 99.87/100.00/100.125c fly, sold at 3.5 in 10k

3LZ1 99.00/98.50ps 1x2, bought for 6 in 5k

FX:

EURUSD (expiry 5th November) 1.1450p, bought for 0.0031 in 1.78k

Contract value: $148,412.5 (~264mln)

FOREX: AUD Follows RBA Signpost: Easy Policy Not Forever

- AUD is among the session's best performers following the overnight RBA rate decision, in which the bank declined to roll their 3-year yield target from the Apr-24 line. The move was seen as a tacit admission that the Bank are taking their first step toward withdrawing extraordinary stimulus. As a result, AUD is better bid, with the AUD/USD now north of the 200-dma at $0.7576.

- Other majors are less directional, with the USD and EUR mixed. The NOK has been ebbing throughout the morning, reversing some of the week's strength on the back of buoyant oil prices.

- EUR/USD saw some early strength just ahead of the European open, touching $1.1895 before fading and returning to negative territory ahead of the NY crossover. This retains the bearish focus, with the Jul 2 1.1808 low the first target.

- Focus turns to the ISM Services Index, which is expected to slow slightly from last month's record high of 64.0. There are no central bank speakers of note.

FX OPTIONS: Expiries for Jul06 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1865-80(E1.6bln), $1.1900-10(E1.6bln)

- USD/JPY: Y109.60-70($1.6bln), Y111.00($2.2bln), Y111.20($615mln)

- USD/CNY: Cny6.45($1.7bln-USD puts)

Price Signal Summary - USD Bulls Return

- In the equity space, S&P E-minis maintain a strong bullish tone. The focus is on 4400.00 next, a round number resistance. EUROSTOXX 50 (U1) on the other appears vulnerable. Attention is on the bearish engulfing candle from Jun 18. A break of support at 4015.00, Jun 21 low would reinforce the importance of the engulfing line and signal scope for a deeper pullback towards 4000.00 and 3914.00, May 20 low.

- In FX, the USD is strengthening this morning and the outlook remains bullish. The EURUSD bear trigger is Friday's low of 1.1808. Resistance to watch is at 1.1909, Jun 30 high. Recent GBPUSD gains appear to be a correction. Attention is on a break of Friday's 1.3733 low that would open 1.3717, Apr 16 low. Resistance is at 1.3928, the 20-day EMA. USDJPY uptrend remains intact. The focus turns to 111.71/112.01, Mar 24, 2020 high and 1.0% 10-dma envelope. Scope also exists for a climb towards 112.23, Feb 20, 2020 high. Key short-term support lies at 110.42, Jun 30 low.

- On the commodity front, Gold is firmer. Attention is on the 50-day EMA that intersects at $1815.8. The area around the EMA represents a key short-term resistance and a clear break is required to suggest scope for stronger near-term gains. Brent (U1) focus is on $77.86, 1.382 projection of Mar 23 - May 18 - May 21 price swing. WTI (Q1) sights are set on $77.35, 1.618 projection of Mar 23 - May 18 - May 21 price swing.

- Within FI, Bund futures short-term directional triggers are; support at 171.67, Jun 22 low and resistance at 173.16, Jun 11 high. Resistance has been probed and the recent high has been 173.19, on Jul 2. A clear break higher is still required to signal scope for a stronger rally. Gilt futures last week tested and probed key resistance at 128.39, Jun 11 high. A clear break would strengthen a bullish case and open 128.50, 1.00 projection of the May 13 - 26 - Jun 3 price swing. Key pivot support is unchanged at 126.70, Jun 3 low.

EQUITIES: Stocks Edge Off Alltime Highs

- Following the trade hiatus on Monday, the e-mini S&P started the Tuesday session well and eked out a new alltime high of 4348. Price action has since faded, with the index slipping around 10 points off the high.

- European markets are in minor negative territory, with Germany's DAX underperforming, while the EuroStoxx50 ebbs by 0.4% or so. Europe's financials are the lagging sector, with communication services not far behind.

- Despite today's moves, the EuroStoxx Bank Index holds above support and ahead of the week's lows. Energy and healthcare names are at the top of the table.

COMMODITIES: OPEC Stress Already Felt As Saudi Arabia Boost OSP Margins

- Following the collapse of the prelim OPEC+ agreement yesterday, energy markets are already beginning to show the stress, with Saudi Arabia's Aramco this morning boosting selling prices for crude headed to Asia, the US and Europe across August, boosting margins against the benchmark by as much as $0.80/bbl.

- As a result, the likes of WTI and Brent crude futures are in positive territory, with both benchmarks hitting new cycle highs ahead of the Tuesday open.

- Gold is in positive territory, with spot hitting new weekly highs and topping $1,800/oz. The moves come despite a bounce in the USD, which is recovering from overnight lows. Gold has narrowed the gap with the 50-day EMA and first material resistance at $1815.80.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.