Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- E.C.B. SET TO HOLD POLICY STEADY TODAY, BUT PEPP BOOST SEEN COMING SOON

- STOCKS BOUNCE MODERATELY IN EUROPEAN TRADE, BUT FINANCIALS LAG

- MERKEL SAYS GERMANY IN "DRAMATIC SITUATION" AS VIRUS SPREADS

- B.O.J. TO EXTEND FACILITIES AS NEEDED, KURODA SAYS

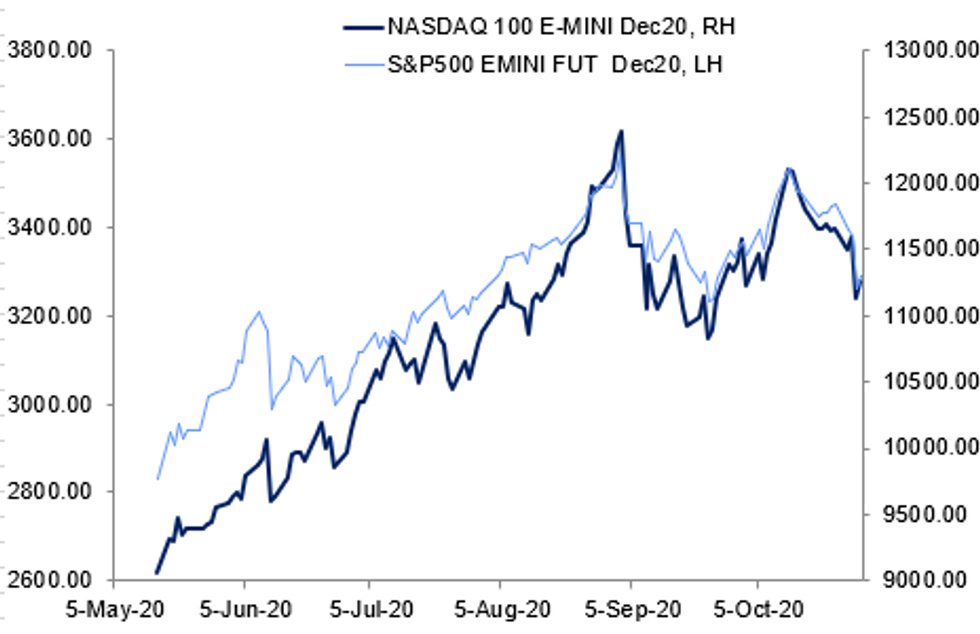

Fig. 1: Tech Leading Equity Bounce, With Heavy-Hitters Reporting Earnings After The Close

BBG, MNI

BBG, MNI

NEWS:

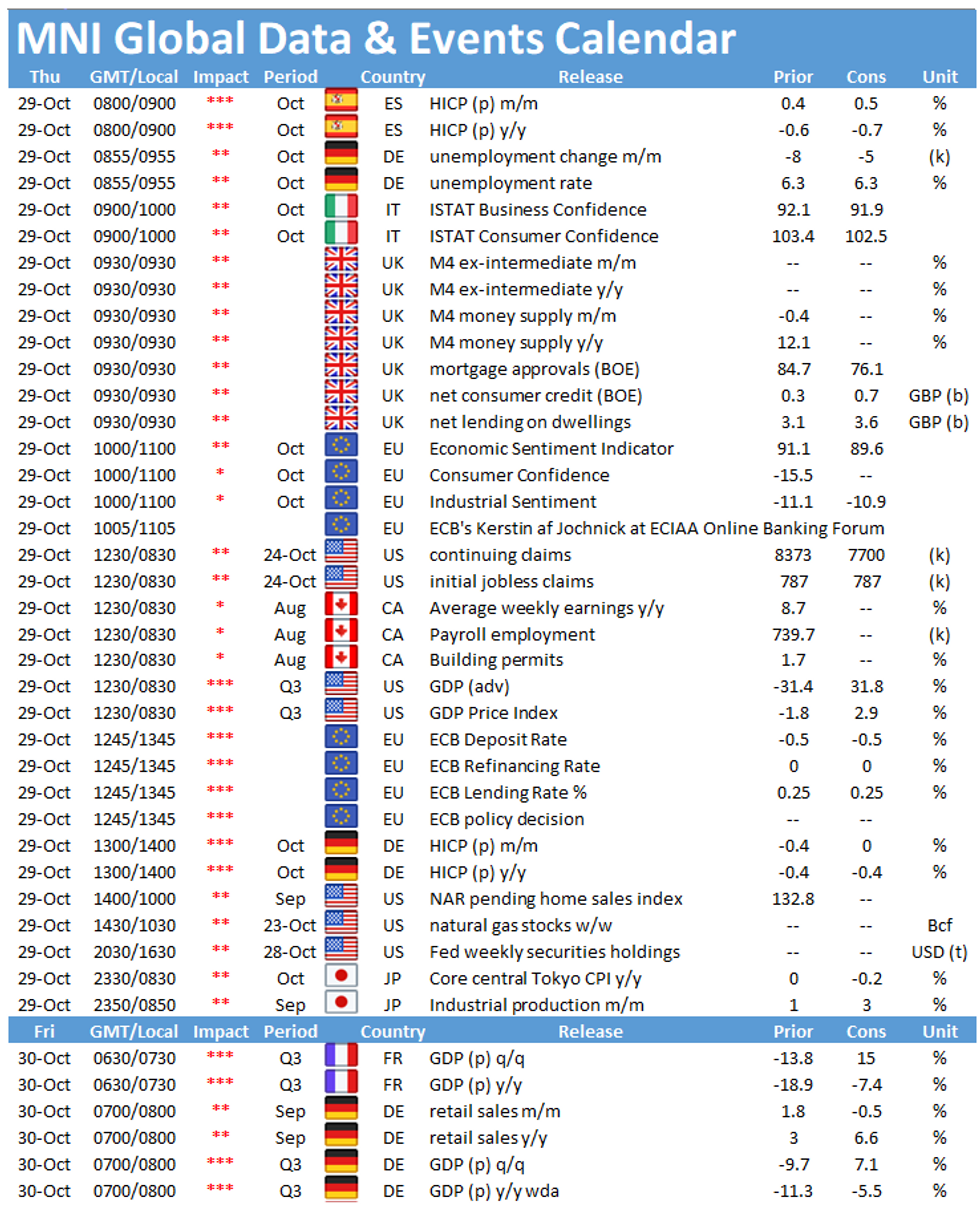

ECB (MNI PREVIEW): Please see the MNI website( CLICK HERE)and email for the full PDF of MNI's preview. The European Central Bank should adopt a 'wait-and-see' approach at its meeting on Thursday as it assesses the impact of the second wave of Covid-19 before adding to the EUR1.35 trillion envelope of its pandemic emergency purchase programme, although it could point to a faster pace of bond buys or authorise a fresh EUR120 billion for its pre-pandemic quantitative easing, sources told MNI.

EQUITIES: Equities bouncing slightly in Europe, with the EStoxx50 up around 0.25%. Across Europe, communication services are seeing the biggest bounce (sector's up 1.2%) but financials are still lagging with the sector flat as markets digest disappointing earnings releases from Credit Suisse and Standard Chartered. The e-mini S&P broke and closed below the 100-dma at 3302.29 yesterday forthe first time since end-February. Earnings take front and centre Thursday, with 3 $trillion companies due toreport: Amazon, Alphabet, Apple & Facebook are due after the close.

COVID/GERMANY (BBG): Chancellor Angela Merkel said Germany was heading into a dramatic situation as the rapid spread of the coronavirus stretches health-care services to their limit. Health-care authorities are no longer able to track infections back to their source and that leads to an exponential growth in infections, Merkel told lawmakers in German parliament on Thursday. "We are in a dramatic situation at the beginning of the cold season," Merkel said in a speech interrupted by opposition lawmakers in a sign of the tension over reviving strict curbs on movement. "I very much understand the frustration, and yes the despair, in these areas."

BOJ: The BOJ will extend its lending facilities if needed but a decision will not be taken until nearer March 31, when the current facilities are due to expire, Bank of Japan Governor Haruhiko Kuroda said Thursday, although he declined to comment when that decision could be, saying it was dependant on corporate financing developments and banks' lending attitude. He said the BOJ kept the policy under constant observation, but noted any extension, if forthcoming, would be on the same terms as current. The Bank of Japan board Thursday kept monetary policy and the forward guidance for policy rates unchanged, indicating policymakers remain vigilant about the impact of the coronavirus on the economy and financial markets, reserving some ammunition for future use.

CHINA: RTRS, citing traders, noted that China's major state banks have been swapping USD for CNY in the onshore FX market, as well as purchasing USD vs. yuan in late evening sessions.

CHINA: China's online retail boom continued in the first nine months of the year, with sales exceeding CNY8 trillion, a rise of 9.7% y/y, Gao Feng, a spokesman at the Ministry of Commerce said at Thursday's regular briefing. Online sales of goods reached CNY6.6 trillion, rising 15.3% y/y, accounting for 24.3% of the overall retail sales, said Gao.

FOREX: Citi revise their month-end FX rebalancing model, with the sharp fall in equities over the past few days resulting in a switch to moderate USD buying vs. A sell signal at the prelim update. The switch is driven by hedge rebalancing flows for both equity and fixed income investors being estimated as USD positive. Although European equities are underperforming vs. US, USD buy signals are seen in all pairs as Citi see more foreign ownership of US equities and higher hedge ratios across Europe.

OIL(Energy Intel): Members of the Opec-plus alliance are currently mulling a proposal to roll over their production cuts at current levels for another three months until Mar. 31 because of weaker than expected demand for oil, Opec delegates say. "There is talk of a three-month extension, but still not all countries have given their feedback," one Opec delegate told Energy Intelligence on Wednesday. Another delegate confirmed that work was already under way to build a consensus ahead of the alliance's next ministerial meeting on Nov. 30 and Dec. 1.

DATA:

MNI: SPAIN OCT FLASH HICP +0.3% M/M, -1.0% Y/Y; SEP -0.6% Y/Y

MNI: SAXONY OCT CPI 0.0% M/M, 0.0% Y/Y; SEP +0.1% Y/Y

MNI: NRW OCT CPI +0.3% M/M, -0.1% Y/Y; SEP -0.3% Y/Y

ITALY OCT BUSINESS CONFIDENCE INDEX 92.9; SEP 91.3

MNI: ITALY OCT CONSUMER CONFIDENCE INDEX 102.0; SEP 103.3

FIXED INCOME: Bond markets await the ECB decision

Treasuries have reversed some of yesterday's weakness as equities have recovered some of their losses after yesterday's rout. Bunds and gilts are largely unchanged on the day with Bunds having recovered some of the overnight weakness on the open.

- The main event of the day will be the ECB meeting and press conference. Any new measures will be announced at 12:45GMT/8:45ET with the press conference beginning at 13:30GMT/9:30ET. Most analysts expect fresh easing initiatives to be put off until December, with today's meeting setting the tone. However, new measures announced today cannot be ruled out. Peripheral spreads are a little wider as we await the meeting and continue to digest the lockdown measures announced by Merkel and Macron yesterday.

- The data calendar so far today has focused on inflation in Europe with Spanish HICP softer than expectations but some of the regional German inflation data has been a bit higher than expectations of the national print would suggest.

- TY1 futures are down 0-00+ today at 138-25 with 10y UST yields up 0.9bp at 0.782% and 2y yields down -0.5bp at 0.144%.

- Bund futures are up 0.05 today at 176.12 with 10y Bund yields down -0.1bp at -0.628% and Schatz yields down -0.4bp at -0.798%.

- Gilt futures are down -0.01 today at 136.18 with 10y yields up 0.4bp at 0.215% and 2y yields up 0.1bp at -0.66%.

FOREX: EUR Heavy Again as Merkel Paints Bleak Picture

Following the sharp sell-off this week, stocks have stabilised a little in Europe, but the bounce is shallow and there's no sign of a sharp recovery at this stage. This has translated into a mixed USD, leaving FX largely non-directional so far.

GBP is modestly outperforming, still getting some support from yesterday's Bloomberg report which suggested that gaps were narrowing between EU and UK negotiators. EUR is faring less well, with German Chancellor Merkel this morning painting a stark picture of Germany's current status - she stated that health authorities are near their limits and the situation is dramatic. EUR/USD sits just above the Wednesday lows at $1.1718. A break below here opens $1.1689 key support ahead of $1.1612.

The ECB rate decision takes focus going forward. While the ECB are not expected to pull the trigger on further policy action today, pressure is clearly building on the governing council given the fragile recovery and the looming risk of further lockdowns.

Weekly US jobless claims data are due as well as Q3 advance GDP numbers from the US, which are expected to show GDP growing at 32% on an annualized basis.

EQUITIES: Tech Outperforming, Financials Underperforming

A small bounce in European equities after a tough couple of days, though financials are underperforming following weak earnings releases. NASDAQ futures are outperforming, with the likes of Amazon, Alphabet, Apple, and Facebook reporting earnings today.

- Asian stocks closed mixed, with Japan's NIKKEI down 86.57 pts or -0.37% at 23331.94 and the TOPIX down 1.62 pts or -0.1% at 1610.93. China's SHANGHAI closed up 3.489 pts or +0.11% at 3272.727 and the HANG SENG ended 122.2 pts lower or -0.49% at 24586.6.

- European equities are slightly higher, with the German Dax up 48.99 pts or +0.42% at 11612.45, FTSE 100 up 12.09 pts or +0.22% at 5594.34, CAC 40 up 13.03 pts or +0.29% at 4584.08 and Euro Stoxx 50 down 1.35 pts or -0.05% at 2963.71.

- U.S. futures are higher led by tech, with the Dow Jones mini up 184 pts or +0.7% at 26593, S&P 500 mini up 27.75 pts or +0.85% at 3291.25, NASDAQ mini up 125.75 pts or +1.13% at 11258.5.

COMMODITIES: Oil Continues To Slide

Crude prices continue to slide despite a stabilisation in broader markets.

- WTI Crude down $0.51 or -1.36% at $36.9

- Natural Gas down $0.04 or -1.19% at $3.252

- Gold spot up $2.28 or +0.12% at $1879.42

- Copper down $0.05 or -0.02% at $306.35

- Silver down $0.17 or -0.71% at $23.2228

- Platinum down $1.93 or -0.22% at $868.83

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.