Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- R.B.A. COULD TAKE RATES TO 2.5%, SAYS LOWE (MNI STATE OF PLAY)

- MNI FEDERAL RESERVE MEETING PREVIEW: NEARING PEAK HAWKISHNESS

- EU COMMISSIONERS TO VOTE ON 6TH ROUND OF RUSSIA SANCTIONS

- GERMAN JOBS MARKET HOLDS STRONG THROUGH APRIL

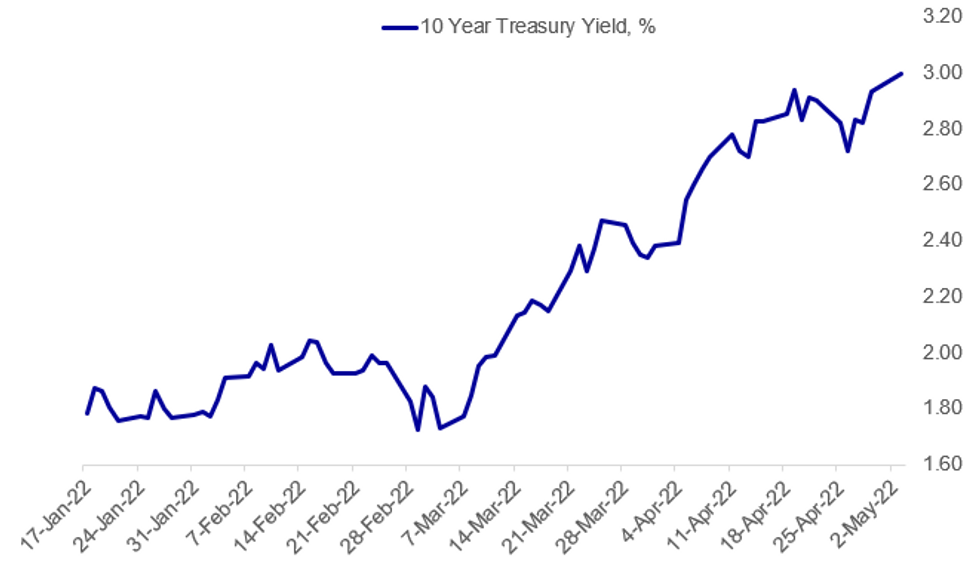

Fig. 1: 10 Year Yields Test 3% Tuesday As Fed Meeting Set To Get Underway

Source: BBG, MNI

Source: BBG, MNI

NEWS:

RBA: Reserve Bank of Australia Governor Philip Lowe said on Tuesday that official interest rates could reach between 1% and 1.5% by the end of this year and as high as 2.5% as the bank enters a tightening cycle. Responding to questions after the RBA increased the Official Cash Rate to 0.35% from a record low 0.10%, its first hike in over a decade and towards the upper end of expectations, Lowe said that it was “not unreasonable to expect” that the normalisation of monetary policy would see the OCR at 2.5%, although he declined to say how long it might take to get there. “It will depend how long these issues (around inflation) resolve,” said Lowe. “There are reasons to believe that inflation will moderate, but the labour market is also tightening.” Lowe said that that “we all knew interest rates couldn’t stay at these rates forever” and that it was now time to normalise policy and move away from emergency settings adopted during the pandemic.

MNI Fed Preview - May 2022: Nearing Peak Hawkishness: We've published our preview for theMay FOMC meeting - this week's decision will be the most hawkish in recent memory, with a 50bp hike and the launch of balance sheet reduction. However, already aggressive market hike pricing limits the potential hawkish impact. Focus will be on the FOMC’s openness to 75bp hikes and/or moving above “neutral”, and any hint of asset sales.

EU/RUSSIA: European Commissioners are due to vote on the sixth round of sanctions against Russia later this afternoon, with the likelihood that a form of oil embargo is included but with carve outs or long lead times for EU member states particularly reliant on Russian crude.

- College of Commissioners meeting takes place in Brussels at 1430CET (0830ET, 1330BST). No confirmation of whether Commission Pres. Ursula von der Leyen will announce sanctions in presser after meeting or in her address Wednesday morning to European Parliament plenary session.

- Euractiv reporting that Hungary and Slovakia will be offered “an exemption or a long transition period” on the oil embargo so not to impose a severe shock on both economies, which remain heavily reliant on Russian oil. Earlier this morning Hungarian Foreign Minister Peter Szijjarto stated that Hungary would not approve any oil embargo that made Russian O&G shipments to Hungary "impossible".

UK (BBG): Prime Minister Boris Johnson appeared to rule out a windfall tax on energy companies after BP Plc promised to channel billions of pounds of its profits into U.K. investments. If the country was to levy such a tax on energy firms’ earnings, which are surging due to high oil and gas prices, that would “discourage them from making investments we want to see, that in the end will keep prices lower for everybody,” Johnson said in an interview with ITV on Tuesday.

GERMANY / BANKS (BBG): German prosecutors are carrying out a raid on the Frankfurt offices of Morgan Stanley as part of their wider probe into the controversial Cum-Ex scandal that robbed tax payers of billions of euros. Authorities are searching a bank and the homes of two suspects in a probe over Cum-Ex and related strategies, according to a spokesman for Cologne prosecutors. More than 75 officers are taking part in the action, he said. Morgan Stanley confirmed that its premises were targeted and said the investigation relates to a “historic activity” and that the bank is “continuing to cooperate with the German authorities.”

DATA:

German Labour Market holds strong through April

GERMANY APR UNEMPLOYMENT RATE (SA) 5.0%; MAR 5.0%

GERMANY APR UNEMPLOYMENT NET CHANGE (SA) -13K; MAR -18K

- German unemployment data saw a fall of -13k of net unemployment in April, down 5k less than in March and a slightly more moderate reading than the 15k forecasted.

- This is the lowest reading in 12 months as the labour market becomes saturated, leaving the unemployment claims rate unchanged at 5.0%, on par with the pre-pandemic early 2020 level.

- In March, German employment exceeded the pre-crisis level by 0.1%. The April data highlights the strength of the German labour market despite new downside risks to growth associated with the onset of the Ukraine war.

UK FINAL APR MANUFACTURING PMI 55.8 (FLASH 55.3); MAR 55.2

Moderate Uptick in UK Manufacturing PMI

UK FINAL APR MANUFACTURING PMI 55.8 (FLASH 55.3); MAR 55.2

FINAL MFG PRINT 0.5 POINTS STRONGER THAN FLASH

- The April final print saw UK manufacturing growth improve more than expected to 55.8, picking up 0.8 points from March.

- Output growth increased from the 5-month low seen in March, with intermediate and investment good industries seeing solid growth.

- Increased new business, improved delivery and reduction of backlogs were underlying upwards growth drivers.

- Outlooks managed to remain in positive territory, albeit the lowest seen in 16 months.

- Cost inflation saw selling prices accelerate at new records, input costs were the second-highest in 30 years. Exports slumped due to weakened foreign demand, with the Ukraine war, China lockdown, Brexit and transportation dragging on business.

MNI: EUROZONE MAR PPI +5.3% M/M, +36.8% Y/Y, FEB +31.5%r Y/Y

Producer Prices at fresh highs, Energy up 11.1% compared to Feb

EUROZONE MAR PPI +5.3% M/M, +36.8% Y/Y, FEB +31.5%r Y/Y

EUROZONE MAR PPI EX. ENERGY +2.1% M/M, +13.6% Y/Y, FEB +12.3%r Y/Y

- Euro area industrial producer prices accelerated 5.3% m/m in March, rising to a new record high of +36.8% y/y.

- This data highlights the initial effects of the Russian invasion of Ukraine, where initial sanctions saw a spike in energy prices of +11.1% compared to the month prior.

- This compared to +1.3% m/m seen pre-invasion in February.

- Intermediate goods rose 2.8% m/m and non-durables by 2.4% m/m.

MNI: EUROZONE MAR UNEMPLOYMENT RATE 6.8%; FEB 6.9%r

FIXED INCOME: Hitting new cycle lows again

- Core fixed income hit new cycle lows across the board again this morning (with TY, Bund, gilt and BTP futures all hitting multiyear lows). There have been no real headline drivers of the moves, but the moves have been partially reversed over the minutes leading up to writing. The initial trigger was probably spillover from a more hawkish-than-expected RBA, which raised rates by 25bp to 0.35% (rather than the 15bp hike that had been expected). Gilts have been the underperformers across the curve, but there appears no headline drivers behind this, either.

- German and Eurozone unemployment data have come in largely in line with expectations while Eurozone PPI was a few tenths higher.

- Probably the data higlight of the day will be US JOLTs, due for release at 15:00BST ahead of tomorrow's FOMC policy decision (which is widely expected to confirm a 50bp hike). We also have the final print of US durable goods and factory orders (both due at 13:30BST).

- TY1 futures are down -0-23+ today at 118-13+ with 10y UST yields up 4.6bp at 2.983% and 2y yields up 4.4bp at 2.762%.

- Bund futures are down -0.43 today at 153.16 with 10y Bund yields up 4.2bp at 0.979% and Schatz yields up 1.6bp at 0.269%.

- Gilt futures are down -0.80 today at 117.64 with 10y yields up 9.0bp at 1.994% and 2y yields up 7.5bp at 1.654%.

FOREX: AUD on Top Following Chunkier Rate Hike

- AUD outperforms all others early Tuesday, with the RBA surprising markets overnight with a 25bps rate hike to 0.35% vs. Expectations of a 15bps tweak. In the subsequent press conference, governor Lowe flagged that the bank could raise rates as high as 1.5% by the end of 2022, and to 2.5% at a cyclical peak.

- In response, AUD/USD made light work of Monday's 0.7082, rallying to just shy of 0.7150 before the pair faded somewhat.

- NZD is softer in comparison, helping AUD/NZD surge well north of the 1.10 handle for the first time since August 2020. Strength north of 1.1065 would mark fresh four year highs.

- GBP is trading more solidly following the return of UK traders after Monday's bank holiday. GBP/USD is back above the 1.25 level for now, although the outlook remains bearish following last week's acceleration of the downtrend. Price has recently cleared 1.2974, Apr 13 low and 1.2676, last printed in September 2020. This has reinforced bearish conditions. The trend remains oversold, however, a reversal pattern is still required to signal a short-term base and a possible reversal.

- US factory orders and final March durables goods data cross alongside JOLTS at 1500BST/1000ET, with BoC's Rogers also on the docket. Members of both the Fed's FOMC and BoE's MPC remain in pre-meeting media blackout periods.

EQUITIES: Cyclical Stocks Lead Early European Gains

- European equities are mostly higher, led by Energy, Consumer Discretionary, and Financial stocks, with the German Dax up 80.61 pts or +0.58% at 14019.62, FTSE 100 down 24.21 pts or -0.32% at 7522.49, CAC 40 up 52.51 pts or +0.82% at 6485.26 and Euro Stoxx 50 up 25.71 pts or +0.69% at 3758.99.

- U.S. futures are flat, with the Dow Jones mini up 12 pts or +0.04% at 32994, S&P 500 mini up 2.75 pts or +0.07% at 4154, NASDAQ mini up 4.75 pts or +0.04% at 13077.75.

- Several Asian markets were closed for holidays.

COMMODITIES: Precious Metals Weaken As Rates Rise

- WTI Crude down $1.04 or -0.99% at $104.13

- Natural Gas up $0.2 or +2.72% at $7.678

- Gold spot down $8.84 or -0.47% at $1853.99

- Copper up $5.5 or +1.29% at $432.3

- Silver down $0.05 or -0.24% at $22.5858

- Platinum up $7.3 or +0.78% at $945.99

LOOK AHEAD:

| Date | GMT/Local | Impact | Flag | Country | Event |

| 03/05/2022 | - | *** |  | US | Domestic-Made Vehicle Sales |

| 03/05/2022 | - |  | EU | ECB Lagarde & Panetta in Eurogroup Meeting | |

| 03/05/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 03/05/2022 | 1300/1500 | | EU | ECB Lagarde High School Q&A | |

| 03/05/2022 | 1400/1000 | ** | | US | factory new orders |

| 03/05/2022 | 1400/1000 | ** | | US | JOLTS jobs opening level |

| 03/05/2022 | 1400/1000 | ** | | US | JOLTS quits Rate |

| 03/05/2022 | 1515/1615 |  | UK | BOE Mutton Panellist at Bankers Association | |

| 03/05/2022 | 1630/1230 |  | CA | BOC Sr Deputy Rogers speaks on operational independence | |

| 04/05/2022 | 2300/0900 | * |  | AU | IHS Markit Final Australia Services PMI |

| 04/05/2022 | 2301/0001 | * | | UK | BRC Monthly Shop Price Index |

| 04/05/2022 | 0130/1130 | ** | | AU | Retail Trade |

| 04/05/2022 | 0130/1130 | ** | | AU | Lending Finance Details |

| 04/05/2022 | 0600/0800 | ** |  | DE | trade balance |

| 04/05/2022 | 0715/0915 | ** |  | ES | IHS Markit Services PMI (f) |

| 04/05/2022 | 0745/0945 | ** |  | IT | IHS Markit Services PMI (f) |

| 04/05/2022 | 0750/0950 | ** |  | FR | IHS Markit Services PMI (f) |

| 04/05/2022 | 0755/0955 | ** | | DE | IHS Markit Services PMI (f) |

| 04/05/2022 | 0800/1000 | ** | | EU | IHS Markit Services PMI (f) |

| 04/05/2022 | 0830/0930 | ** | | UK | BOE M4 |

| 04/05/2022 | 0830/0930 | ** | | UK | BOE Lending to Individuals |

| 04/05/2022 | 0900/1100 | ** | | EU | retail sales |

| 04/05/2022 | 1100/0700 | ** | | US | MBA Weekly Applications Index |

| 04/05/2022 | 1215/0815 | *** | | US | ADP Employment Report |

| 04/05/2022 | 1230/0830 | ** | | CA | International Merchandise Trade (Trade Balance) |

| 04/05/2022 | 1230/0830 | ** | | US | Trade Balance |

| 04/05/2022 | 1345/0945 | *** | | US | IHS Markit Services Index (final) |

| 04/05/2022 | 1400/1000 | *** | | US | ISM Non-Manufacturing Index |

| 04/05/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 04/05/2022 | 1800/1400 | *** | | US | FOMC Statement |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.