Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- BARNIER'S CONCILIATORY LANGUAGE SPARKS RENEWED BREXIT DEAL OPTIMISM

- PELOSI, MNUCHIN MAKE ANOTHER RUN AT STIMULUS MCCONNELL OPPOSES

- AREAS IN ENGLAND COULD SEE 3-WEEK LOCKDOWN IN NOVEMBER (TIMES RADIO)

- BOJ SEES NO NEED FOR POLICY STRATEGY REVIEW NOW (MNI INSIGHT)

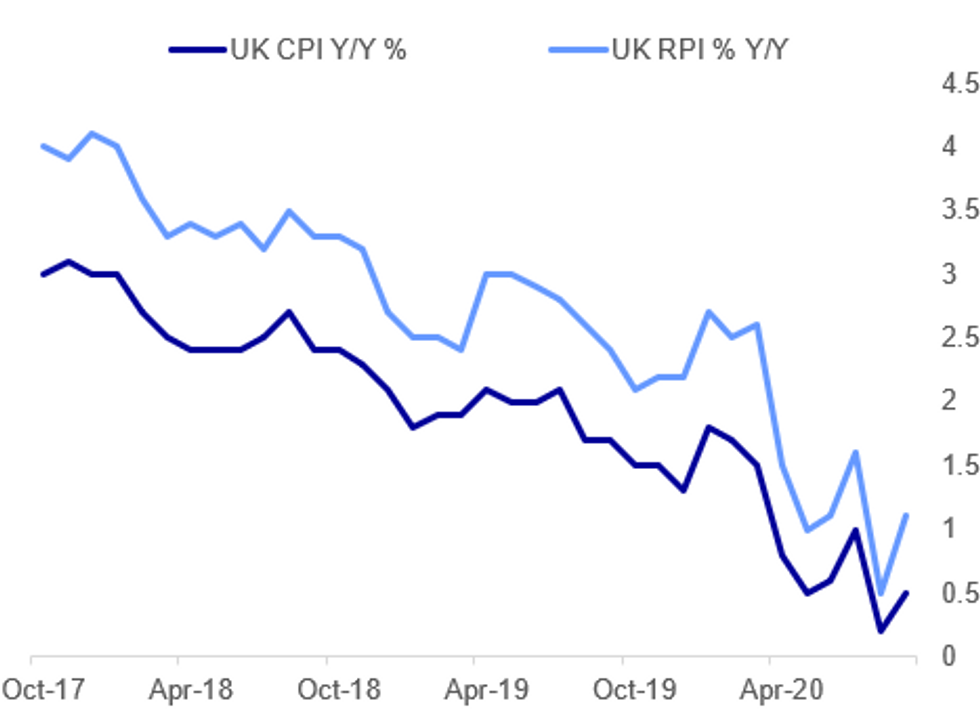

Fig. 1: UK CPI Weaker Than Expected In September

BBG, MNI

BBG, MNI

NEWS:

EU/UK: Chief negotiator with the EU Michel Barnier speaking to European Parliament plenary session:- "We will seek the necessary compromises on both sides in order to do our utmost to reach an agreement and will do so right up until the last day that it's possible to do so. Our doors will always remain open right up until the very end."

- "We want a deal that will be mutually beneficial to both parties in respect of the autonomy and sovereignty of both sides a deal, reflecting a balanced compromise,"

- "An agreement is within reach. If both sides are willing to work constructively you're both sides are willing to compromise. And if we're able to make progress in the next few days on the basis of legal texts. "

- The passages above uses much more conciliatory language towards the UK than that used previously.

EU/UK: EUCO President Charles Michel delivering statement to European Parliament after the 15-16 Oct EUCO summit.

- Gives similar lines that have come from EU institutional leaders numerous times before on Brexit: 'EU wants a deal, but not at any cost', 'the UK cannot have its cake and eat it', on LPF: 'its a question of fair competition', 'the UK has a big decision to make', 'time is very short, we are ready to negotiate', 'EU is ready for no deal'.

- Says that loss of access to UK fishing waters would cause extraordinary damage to the EU's fishing fleet.

US (BBG): Treasury Secretary Steven Mnuchin and House Speaker Nancy Pelosi will try Wednesday to bridge remaining gaps in their talks over comprehensive coronavirus relief, blowing past Pelosi's self-imposed Tuesday deadline amid signs of progress toward a pre-election deal.But Senate Majority Leader Mitch McConnell, who is pressing ahead with his own, more targeted plan, warned the White House against agreeing to anything akin to Pelosi's more sweeping proposal. The speaker agreed to continue talking beyond her original Tuesday cut-off, saying an agreement with the Trump administration needs to be done by the weekend to get a bill passed by the end of next week, ahead of Election Day Nov. 3.

UK: Tom Newton Dunn at Times Radio tweets: "There is deep doubt among Govt scientists that Tier 3s will work because cases now so high in them. Plans are being actively worked up by Chris Whitty for local 3 week circuit breaker lockdowns in Tier 2 as well as Tier 3 areas across England next month, TimesRadio has learned."

* Hospital admissions from COVID-19 stood at an average of 241 per day across week to Oct 18 in NW England, and at 185 per day in NE England and Yorkshire(the regions where tier 3 restrictions have been put in place in some areas). * In London, under tier 2 restrictions, average daily hospital admissions forCOVID-19 stood at 78 over the week leading to Oct 18.

UK DATA: Y/Y inflation ticked up in Sep to 0.5%, falling slightly short of market expectations looking for an increase to 0.6%. Core inflation edged up to 1.3%, hitting a two-month high. The largest upward contributions arose from transport and restaurants and hotels. The end of the Eat Out Help Out scheme led to an increase of prices in restaurants. According to the ONS inflation would have been 0.8% in Aug without the scheme and the VAT cut which is still in place. Air fares showed the biggest upward contribution within transport as fares didn't fall as much as a year ago. The ONS noted that car sales increased as consumers are trying to avoid public transport. Output inflation declined for the sixth consecutive month, falling by 0.9%, while input inflation eased for the eighth successive month, recording -3.7% in Sep. Petroleum products revealed the largest downward contribution to output inflation, while the biggest negative contribution to input inflation came from crude oil.

UK DATA: Underlining the fiscal challenges UK authorities face in the wake of the Covid-19 pandemic, the country's debt-to-GDP ratio soared to a 60-year high in September, data released Wednesday by the Office for National Statistics showed. Public debt (public sector net debt excluding public sector banks, PSND ex) rose by 259.2 billion in the first six months of the financial year to reach 2,059.7 billion at the end of September 2020, or around 103.5% of gross domestic product (GDP); this was the highest debt to GDP ratio since the financial year ending (FYE) 1960.

BOJ (MNI INSIGHT): The Bank of Japan sees no current need for a strategy review that would include studying forward guidance and a widening of its communication tools with markets as economic and financial conditions don't yet warrant a change, MNI understands. For full article contact sales@marketnews.com

DATA

UK DATA: UK Inflation Edged Up After EOHO Scheme End

- SEP CPI +0.4% M/M, +0.5% Y/Y VS +0.2% Y/Y AUG

- SEP CORE CPI 0.6% M/M, +1.3% Y/Y VS +0.9% Y/Y AUG

- SEP OUTPUT PPI -0.1% M/M; -0.9% Y/Y VS -0.9% Y/Y AUG

- SEP INPUT PPI -1.1% M/M; -3.7% Y/Y VS -5.5% Y/Y AUG

FIXED INCOME: Brexit talks and fiscal optimism the familiar themes

Optimism on both a Brexit deal and that US stimulus talks are not completely dead have helped sentiment this morning with fixed income markets lower, although they have they have retraced some of their losses.

- In terms of Brexit, EU Chief Negotiator Barnier addressed the European Parliament and his language was much more conciliatory. He said that "an agreement is within reach" and hoped to make progress "in the next few days".

- UK CPI was a little softer than expected but had very little impact on markets, the big event of the day for the UK will be a speech by the BOE's Ramsden on monetary policy at a Society of Professional Economists event.

- We will also hear from the ECB's de Guindos and Lane and the Fed's Mester, Kaskari, Kaplan, Barkin, Quarles and Bullard as well as receive the Beige Book.

- TY1 futures are down -0-4 today at 138-18+ with 10y UST yields up 2.3bp at 0.810% and 2y yields up 0.6bp at 0.150%.

- Bund futures are down -0.23 today at 175.58 with 10y Bund yields up 1.7bp at -0.590% and Schatz yields up 0.7bp at -0.779%.

- Gilt futures are down -0.35 today at 136.11 with 10y yields up 3.3bp at 0.219% and 2y yields up 0.4bp at -0.67%.

FOREX: Sterling Strong On Sovereignty Pledge

The to-and-fro of Brexit talks continue to exert influence on GBP, which is outperforming all others in G10 early Wednesday. EU negotiator Barnier appeared to formally agree on and assert UK sovereignty, removing a further blockage to the resumption of trade talks between the two parties. While rules surrounding fisheries and a level playing field still need to be agreed on, the market is still erring toward the likelihood of a deal.

GBP/USD rallied convincingly through the $1.3012 50-dma in response, with $1.3083 the next upside target.

The USD is still on the backfoot, prompting another multi-week low in the USD index. The move lower in the greenback comes despite weaker equities today, with US futures indicating a lower open later today.

Canadian retail sales and inflation data are the highlights Wednesday. Speaker highlights include BoE's Ramsden, ECB's Lane as well as six further Fed speakers.

EQUITIES: Weakening After A Strong Start

A weak start to equities in European trading, following a fairly strong start. No particular catalyst seen, but market participants clearly awaiting further clarification on the US fiscal stimulus outlook.

- Asian equities closed mixed, with Japan's NIKKEI up 72.42 pts or +0.31% at 23639.46 and the TOPIX up 11.86 pts or +0.73% at 1637.6. China's SHANGHAI closed down 3.078 pts or -0.09% at 3325.025 and the HANG SENG ended 184.88 pts higher or +0.75% at 24754.42.

- European stocks are sharply lower, with the German Dax down 163.74 pts or -1.29% at 12567.02, FTSE 100 down 85.87 pts or -1.46% at 5802.33, CAC 40 down 62.46 pts or -1.27% at 4865.01 and Euro Stoxx 50 down 42.66 pts or -1.32% at 3184.66.

- U.S. futures are weaker, with the Dow Jones mini down 64 pts or -0.23% at 28118, S&P 500 mini down 7.75 pts or -0.23% at 3424.5, NASDAQ mini down 51.75 pts or -0.44% at 11609.

COMMODITIES: Weaker Dollar, Stronger Gold/Silver

Precious metals are sharply higher as the dollar index plumbs six-week lows, while crude oil is underperforming.

- WTI Crude down $0.68 or -1.63% at $41.05

- Natural Gas up $0.05 or +1.61% at $2.958

- Gold spot up $10.16 or +0.53% at $1916.42

- Copper up $3.3 or +1.05% at $318.15

- Silver up $0.33 or +1.33% at $24.9461

- Platinum up $1.4 or +0.16% at $876.46

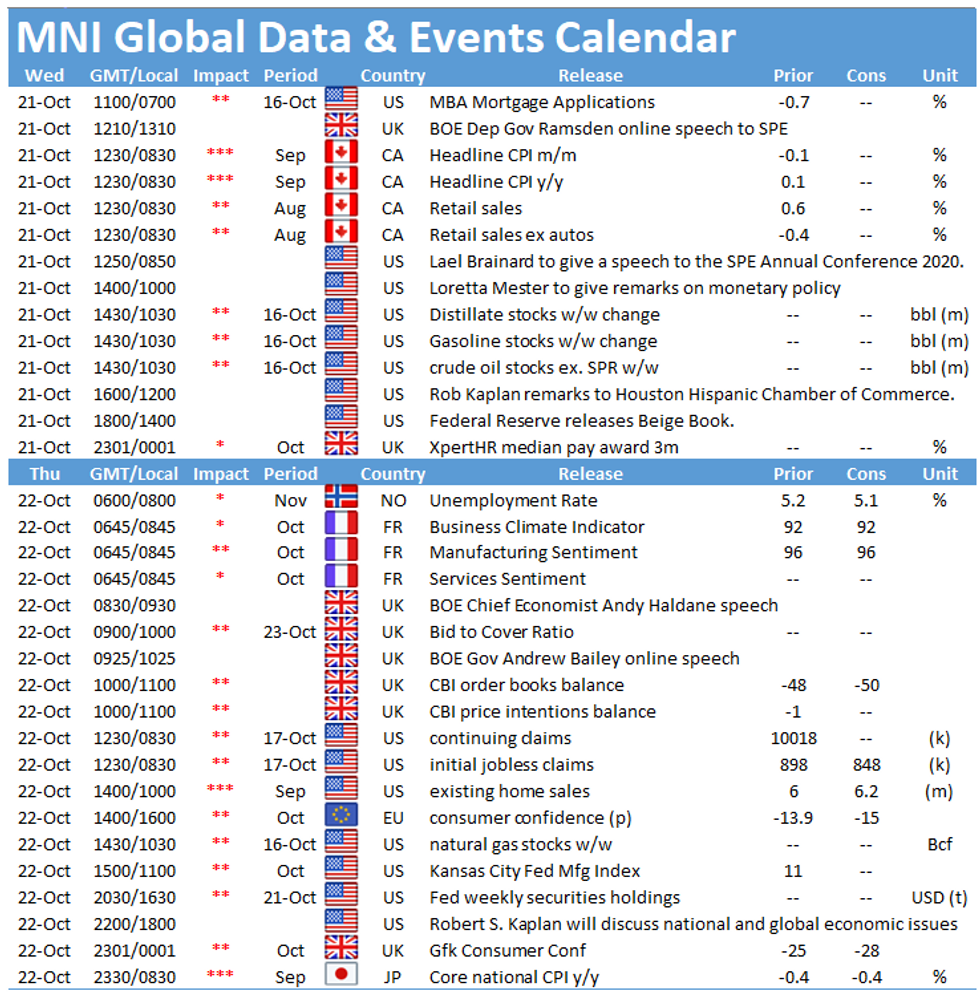

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.