Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- TECH EQUITY SELL-OFF CONTINUES; TREASURIES, BUNDS ALSO WEAKER

- U.K. GOVT TO OUTLINE POST-PANDEMIC AGENDA TODAY

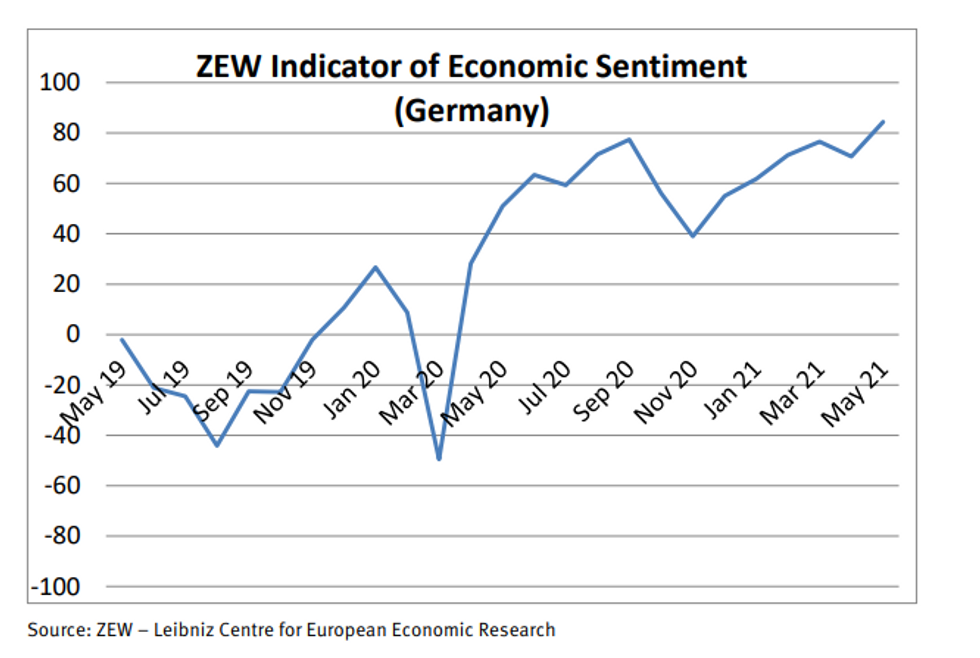

- ZEW SURVEY SHOWS GERMAN INVESTOR CONFIDENCE HITTING 21-YR HIGHS

- FRANCE: LE PEN TELLS MACRON HE RISKS "CIVIL WAR" AFTER MILITARY WARNING

- GERMAN INFLATION COULD GO OVER 3%: ECB'S SCHNABEL

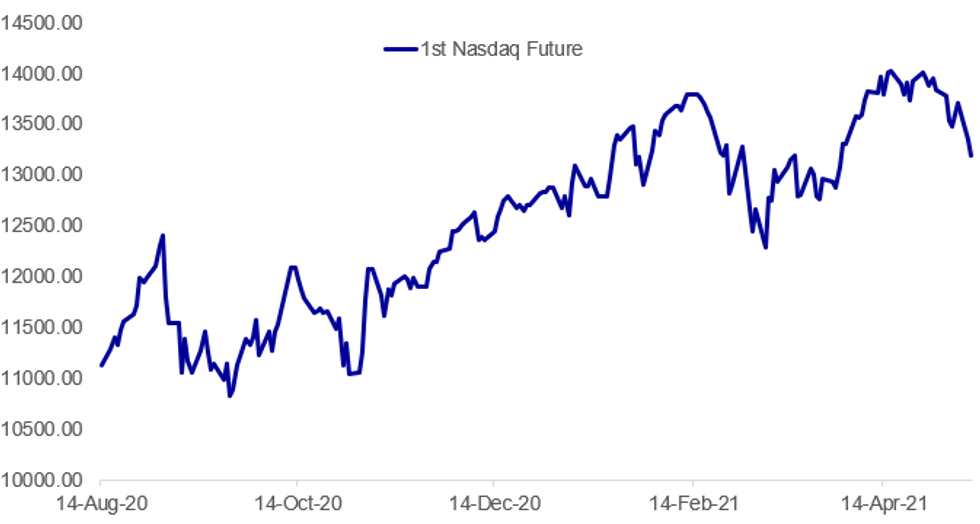

Fig. 1: Nasdaq Losses Continue

BBG, MNI

BBG, MNI

NEWS:

TECH STOCHS (BBG): The worldwide slump in technology stocks deepened Tuesday, with investor angst over inflation and stretched valuations adding to fresh signs of regulatory scrutiny in China. Losses in Taiwan Semiconductor Manufacturing Co. and Samsung Electronics Co. helped send MSCI Inc.'s gauge of Asian tech stocks to its biggest drop since Feb. 26, while futures on the Nasdaq 100 slumped in Asia after the underlying index's 2.6% slide on Monday. The Hang Seng Tech Index sank as much as 4.5%, extending its tumble from a February high to about 30%. Meituan drove declines after the Chinese e-commerce giant's business practices were criticized by an influential consumer advocacy group, just days after the company's CEO shared and then deleted a poem on social media that some interpreted as a veiled criticism of Beijing.

U.K.: Tuesday's State Opening of Parliament will see the UK government outline its legislative programme for the upcoming parliamentary session, with expectations that around 25 new bills will be contained, giving a clear indication of the direction Prime Minister Boris Johnson is looking travel. Ministers have indicated that the speech will focus on a delayed environment bill ahead of the Cop26 gathering on climate change later in the year. It is also expected to see the inclusion of bills focusing on skills training and post-16 education -- aimed at both 'levelling up' inequality across the country and helping in the post-pandemic economic recovery.

FRANCE (BBG): Far-right leader Marine Le Pen said France is at risk of a civil war as she prepares to tackle President Emmanuel Macron in next year's election. After a group of retired generals last month hinted at the threat of a military uprising, another open letter to the president -- this time unsigned but attributed to serving officers -- stoked further controversy Sunday with a warning of "chaos and violence." "It's a lucid assessment," Le Pen told reporters Monday at a campaign event in western France. "There's always a risk of civil war." Le Pen, who could run Macron close in the presidential ballot according to the latest polls, said that she isn't calling for insurrection and urged those who supported the latest letter to join her movement.

GERMANY/ECB: Inflation in Germany could rise above 3% in the short-term, European Central Bank Executive Board member Isabel Schnabel said in an interview Tuesday with German broadcaster n-tv. However, the increase is likely to be only temporary, with the central bank expected to look through it, she added. "If we actually see that there was suddenly a very rapid development of inflation, which is really not in evidence at the moment, then of course we would have to adjust our measures and of course we would have to do that gradually," Schnabel said. "This must be prepared above all through communication. Everyone would then have the opportunity to gradually adapt to it."

EU/CHINA: The already-clear cracks in the EU's supposedly united front in the face of China were exposed further yesterday when Hungary vetoed a joint statement intended to accuse Beijing of a crackdown on democratic freedoms in Hong Kong.

- German Foreign Minister Heiko Maas called the decision "absolutely incomprehensible", with the statement already having been watered down in tone to try to gain Budapest's approval. To reporters Maas stated that "This is not the first time that Hungary has broken away from [the EU's] unity when it comes to the issue of China, I think everybody can work out for themselves where the reasons are — because there are good relations between China and Hungary".

- EU High Representative for Foreign Affairs and Security Policy Josep Borrell stated that he would attempt one more go at securing support from all 27 member states for a resolution on China, but said that if that was not possible then, "we have to take positions that don't reflect unanimity".

- Hungary was the first EU recipient of Chinese COVID-19 vaccines, something that has allowed the country to speed ahead of most other EU peers in its vaccination efforts. The close relations between Budapest and Beijing have also seen Chinese FDI flood into Hungary, but at the expense of many other EU nations' trust in Hungary as a reliable partner when attempting to provide a united European front against Beijing's actions in Hong Kong or Xinjiang.

DATA:

ZEW Expectations Sentiment Surges in May

GERMANY MAY ZEW ECONOMIC SENTIMENT +84.4; APR +70.7

GERMANY MAY CURRENT CONDITIONS -40.1; APR -48.8

- ZEW Expectations jumped 13.7pt to 84.4 in May, stronger than expected (BBG: 71.0).

- This follows a small downtick in Apr and now stands at the highest level since Feb 2000.

- The ZEW Current Conditions improved further by 8.7 to -40.1 in May, which is better than anticipated (BBG: -41.6) and the highest level since the beginning of the pandemic.

- Nevertheless, the the current conditions index remains in significantly negative territory, hence the divergence between the expectations and the current situation persists.

- Financial market experts are more optimistic as third wave is slowing down says ZEW President Achim Wambach.

- "The experts expect a significant economic upswing in the coming six months. The economic outlook for the euro area and the United States has improved considerably as well", Wambach added.

- EZ economic sentiment surged by 17.7pt to 84.0 in May, while current conditions rose sharply by 14.1pt to -51.4.

- Inflation expectations for the EZ increased 2.5pt to 77.6, with the majority of financial experts projecting inflation to rise further in the next 6 months.

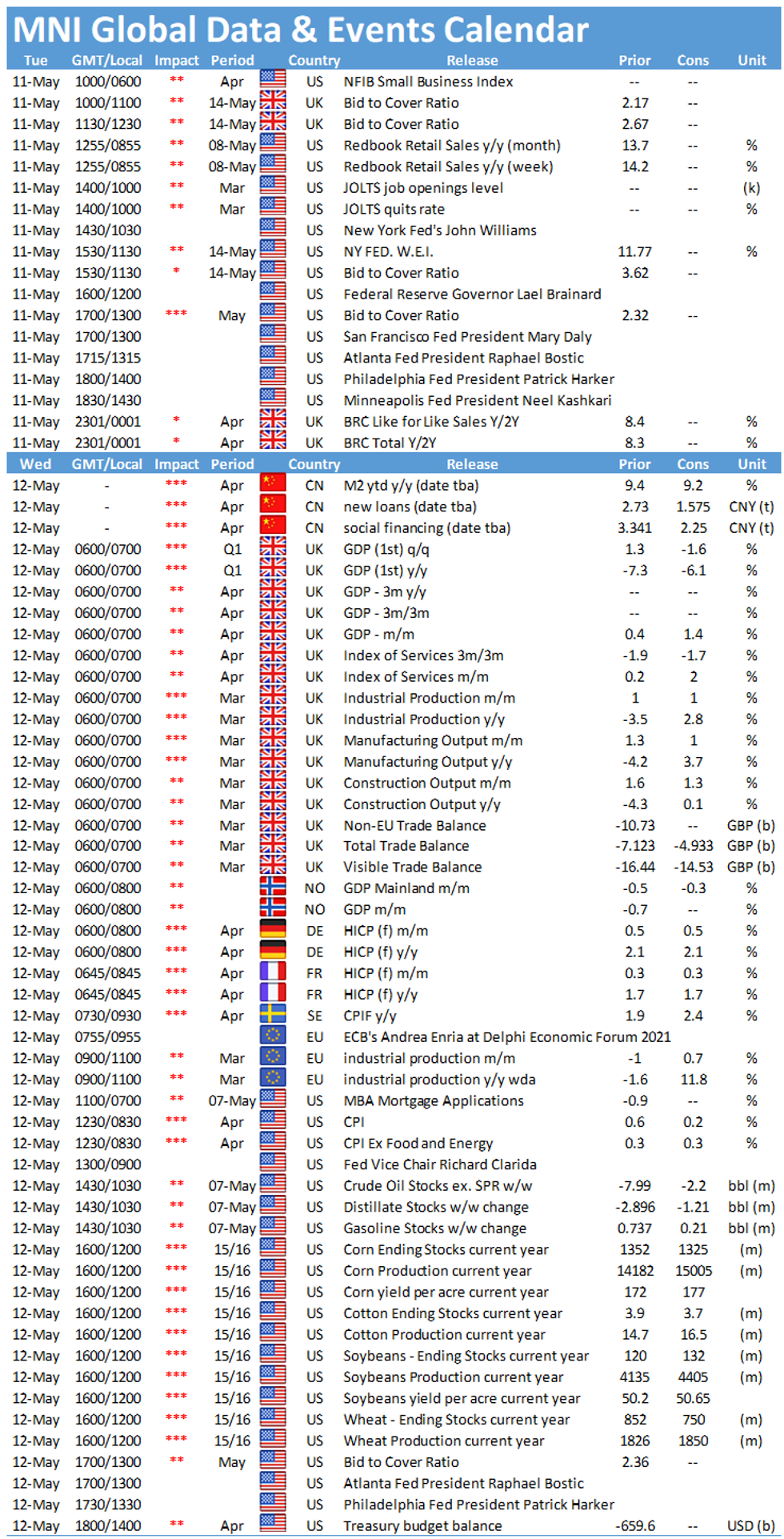

FIXED INCOME: Looking ahead to tomorrow's US CPI print

Core fixed income has been under pressure this morning as markets look ahead to tomorrow's US CPI print.

- Consensus is looking for tomorrow's CPI print to come in at 3.6% Y/Y on a headline basis. This would be the highest level since 2011 and easily eclipse the 2.9% high seen in July 2018. Core CPI is expected to pick up above 2% with the M/M print expected at 0.3%M/M.

- Despite the focus being on US CPI, it has been European core FI that has borne the brunt of the losses today with Bunds underperforming gilts (with 10-year yields up 4.7bp and 4.1bp respectively).

- Against this backdrop, Germany is holding a syndication to launch a new 30-year Green Bund but demand has remained strong with the spread set at the benchmark minus 2bps.

- The rest of the calendar remains relatively light with Italian IP weaker than expected, the German ZEW stronger and only NFIB and JOLTs data from the US today.

- There are a number of Fed speakers scheduled (Williams, Brainard, Daly, Bostic, Harker, Kashkari) while BOE's Bailey is due to talk on LIBOR alternatives.

- Gilt futures are down -0.48 today at 127.80 with 10y yields up 4.3bp at 0.830% and 2y yields up 2.5bp at 0.058%.

- Bund futures are down -0.76 today at 169.53 with 10y Bund yields up 4.8bp at -0.165% and Schatz yields up 1.3bp at -0.680%.

- BTP futures are down -0.56 today at 146.43 with 10y yields up 5.2bp at 0.979% and 2y yields up 1.8bp at -0.271%.

FOREX: Equity Sell-Off Still Hanging Over Markets

- Yesterday's US equity market sell-off is lingering across the continent today, with European markets lower by 1% or more. Currency markets aren't following suit, however, with the JPY the poorest performer so far in G10 (EUR/JPY sits just below yesterday's multi-year high of 132.53) while AUD, EUR hold their ground.

- EUR/USD trades firmer, with the pair eyeing yesterday's 1.2178 high for direction, with this morning's ZEW survey lending some support. The expectations component hit the highest since January 2000 at 84.4.

- Scandi currencies are higher early Tuesday, with SEK and NOK among the best performers in G10 so far. This has kept both USD/NOK and USD/SEK well within reach of the 2021 cycle lows, with markets watching 8.1493 and 8.2058 in each respective pair.

- The data slate is light Monday, with no major releases on the docket. This keeps focus on the central bank speaker slate with a large number of Fed members due. Williams, Brainard, Daly, Bostic, Harker and Kashkari all speak, with Knot and de Cos of the ECB also due.

EQUITIES: Tech Rout Continues

- Asian stocks closed mostly lower, with Japan's NIKKEI down 909.75 pts or -3.08% at 28608.59 and the TOPIX down 46.35 pts or -2.37% at 1905.92. China's SHANGHAI closed up 13.854 pts or +0.4% at 3441.845 and the HANG SENG ended 581.85 pts lower or -2.03% at 28013.81

- European equities are off sharply, with the German Dax down 319.69 pts or -2.08% at 15104.65, FTSE 100 down 148.44 pts or -2.08% at 6984.66, CAC 40 down 118.55 pts or -1.86% at 6271.21 and Euro Stoxx 50 down 79.02 pts or -1.96% at 3949.04.

- U.S. futures are lower, with the Dow Jones mini down 172 pts or -0.5% at 34496, S&P 500 mini down 30.25 pts or -0.72% at 4153.25, NASDAQ mini down 163.75 pts or -1.23% at 13193.

COMMODITIES: Copper Defies Broader Sell-Off

- WTI Crude down $0.51 or -0.79% at $64.44

- Natural Gas down $0.02 or -0.58% at $2.915

- Gold spot up $0.15 or +0.01% at $1834.64

- Copper up $5.5 or +1.17% at $475.6

- Silver up $0.11 or +0.39% at $27.341

- Platinum down $0.43 or -0.03% at $1245

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.