Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

A reminder that tomorrow delivers September inflation data and trade figures.

- The market expects CPI y/y at 0.2% (forecast range is -0.1% to 0.3%, prior was 0.1%). The PPI is projected at -2.4% y/y (forecast range is -2.2% to -2.8%, prior was -3.0%).

- The official manufacturing PMI prints for September showed an increase in both input prices (59.4 from 56.5) and output prices (53.5 form 52.0). The non-manufacturing PMI saw price measures rises as well, albeit by a lower magnitude.

- Base effects may also aid the PPI, while energy prices have generally been trending higher.

- CPI may be impacted by volatile pork prices, which surged +11% in August. Some retracement may flow through to the broader food index. Better retail spending trends may aid the non-food basket at the margin.

- On the trade side, exports are expected at -8.0% y/y (forecast range is -6.0% to -12.0%, prior -8.8%). Imports are forecast at -6.3% y/y (forecast range is -1.0% to -7.5%, prior -7.3%). The trade surplus is projected at $70.60bn (prior $68.20bn).

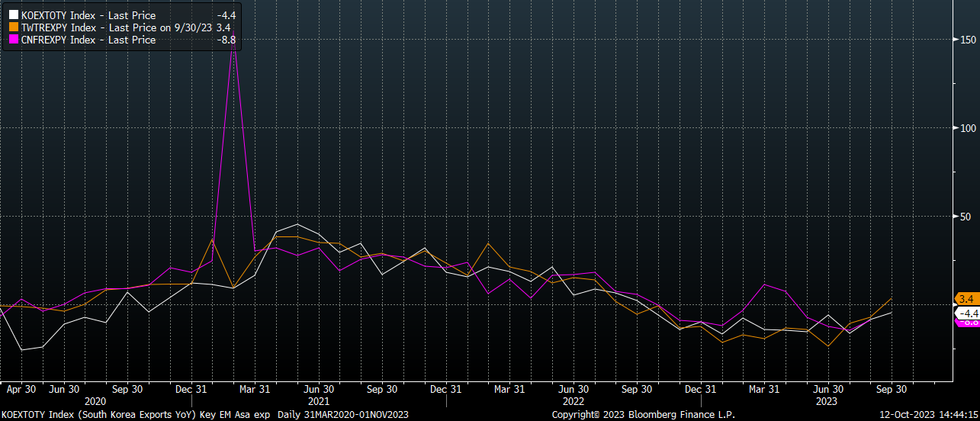

- South Korea and Taiwan export figures have already printed for September, surprising on the upside (particularly for Taiwan). This suggests some modest upside risks for tomorrow's China export print, see the chart below (China is the pink line). Still, there have been divergences in the trends of each series in recent years.

- The manufacturing PMI export sub index rose in September to 47.8, still sub the 50.0 expansion/contraction point, but 0.8ppts higher on levels from a year ago.

Fig 1: North East Asia Export Trends

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok