Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS

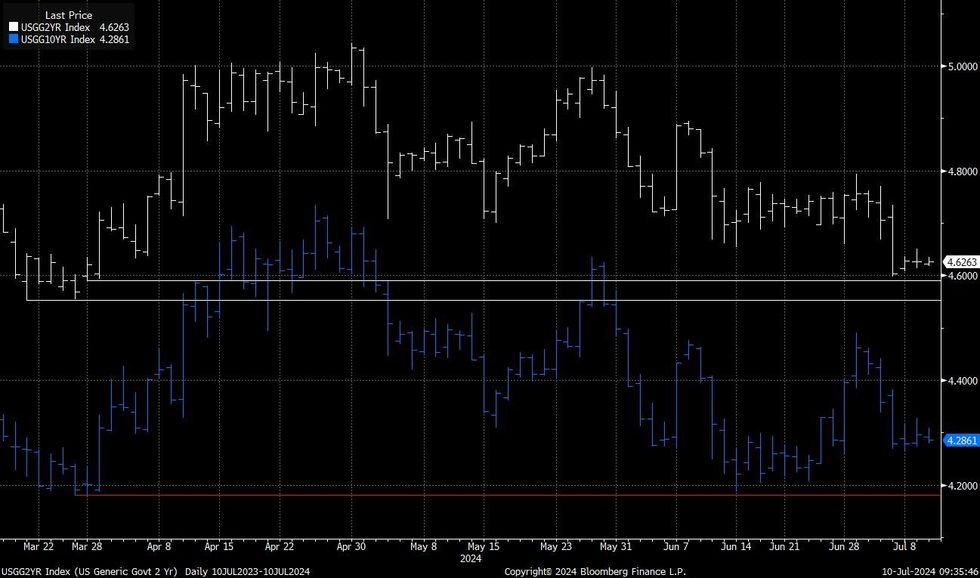

2s and 10s have failed to breach late March yield lows. Bulls will be eying potential triggers for a range break.

- Tomorrow’s CPI release provides the next major fundamental input, although we note that there is an unusually wide range of estimates for the core readings and uncertainty surrounding some sub-indices, heightening the need for caution when interpretating the data.

- Also, we believe that a ‘hawkish’ surprise presents the greatest risk to prevailing market positioning, raising the bar for dovish market interpretation of the data.

- More broadly, the recent run of disappointing U.S. labour market and economic activity data leaves the door open to a data-dependent Fed cut in September.

- Fed fund futures price ~20bp of cuts through the Sep FOMC and ~50bp through year end, representing a cut at 2/4 remaining ’24 meetings.

- This seems relatively fair to us at this juncture, so a dovish adjustment to ’25 FOMC pricing may present the most likely avenue for a move lower in yields.

- This could come via a continued moderation in the U.S. economic exceptionalism thesis.

- Zooming out, we caution that the election presents a medium-term source of uncertainty for markets and could limit any moves lower in yields.

Fig. 1: U.S. 2- & 10-Year Tsy Yields (%)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok