Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- MNI: PMIs See Sharp Decline With Weaker Jobs, Prices

- BOE RAMSDEN :TODAY'S PMI CONSISTENT WITH UK ECONOMY BEING IN RECESSION, Rtrs

- JAPAN PM KISHIDA: ACCEPTED ECONOMY MINISTER YAMAGIWA'S RESIGNATION, Bbg

US Tsys: Carry-over Short End Bid, Stocks Strong

Tsys trading mixed - bods weaker but off midmorning lows, short end firmer (but well off overnight highs) amid ongoing debate over hawkish policy and risk of over-hiking from Friday.

- No obvious headline trigger as bonds reversed early support - no react to Chicago Fed National Activity Index higher than expected at 0.1 vs. -0.1 est, August revised to 0.1 from 0.0.

- Weak US S&P Global PMI preliminary reports see short-end Tsys rally appr 4bps, US$ recede. The S&P composite surprisingly fell from 49.5 to 47.3 (cons 49.3), the second sharpest monthly decline since 2009 barring the initial pandemic period.

- Quiet second half w/ Fed in policy blackout through the Nov 2 FOMC. No substantive reaction to Rishi Sunak replacing Liz Truss as PM.

- Tuesday data on tap (prior, est): FHFA House Price Index MoM (-0.6%, -0.6%); S&P CoreLogic CS 20-City MoM SA (-0.44%, -0.80%); YoY (16.06%, 14.10%); Consumer Confidence (108.0, 106.0); Richmond Fed Mfg Index (0, -5).

- Q3 equity earnings annc pick up in earnest tomorrow: sampling of pre-open annc: United Parcel Service (UPS) $2.847 est; General Motors (GM) $1.893 est; General Electric (GE) $0.468 est;

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00115 to 3.06571% (-0.0172 total last wk)

- 1M -0.00914 to 3.57643% (+0.14257 total last wk)

- 3M -0.03157 to 4.32686% (+0.16472 total last wk) * / **

- 6M +0.00200 to 4.87700% (+0.18971 total last wk)

- 12M -0.10957 to 5.36600% (+0.19243 total last wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 4.35843% on 10/21/22

- Daily Effective Fed Funds Rate: 3.08% volume: $99B

- Daily Overnight Bank Funding Rate: 3.07% volume: $265B

- Secured Overnight Financing Rate (SOFR): 3.02%, $955B

- Broad General Collateral Rate (BGCR): 3.00%, $387B

- Tri-Party General Collateral Rate (TGCR): 3.00%, $372B

- (rate, volume levels reflect prior session)

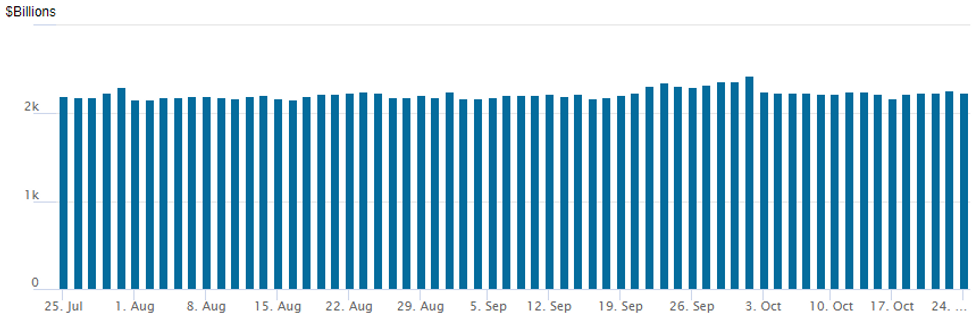

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $2,242.044B w/ 102 counterparties vs. $2,265.071B in the prior session. Prior record high stands at $2,425.910B on Friday, September 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Carry-over upside call trade in SOFR options overnight following Fri's strong rebound in 2s-10s amid speculation over a 75bps hike at year end (WSJ/Timiraos) underscored by midday comments from SF Fed Daly (FOMC needs to start considering a slowing the pace of interest rate hikes in order to avoid tightening monetary policy too much).

- SOFR Options:

- Block, +10,000 SFRZ2 95.75/95.87 call spds, 1.0

- Update +60,000 SFRZ2 95.75/95.87 call spds, 0.75

- -3,000 SFRF3 95.75 calls 5.0 ref 95.125

- Block, 15,000 SFRZ2 95.75/96.00/96.25 call flys, 0.75

- 8,500 Block/screen SFRZ2 95.37/95.50/95.56/95.68 call condors

- 3,000 short Aug 95.25 puts

- Block, 8,880 SFRZ2 95.00/95.12/95.25/95.37 put condors, 5.0-5.5

- Treasury Options saw better put volumes :

- 4,000 TYZ 104.25 puts, 5

- 4,200 FVZ 105.25 puts, 26

- Block, 10,000 FVZ2 105 puts, 25.5 ref 106-04.75

- 5,000 TYZ 109/110 put spds, 25-27

- 10,000 Block/screen TYZ 108 puts, 33-32

- Block, total 15,000 FVZ 105.25 puts, 28-23

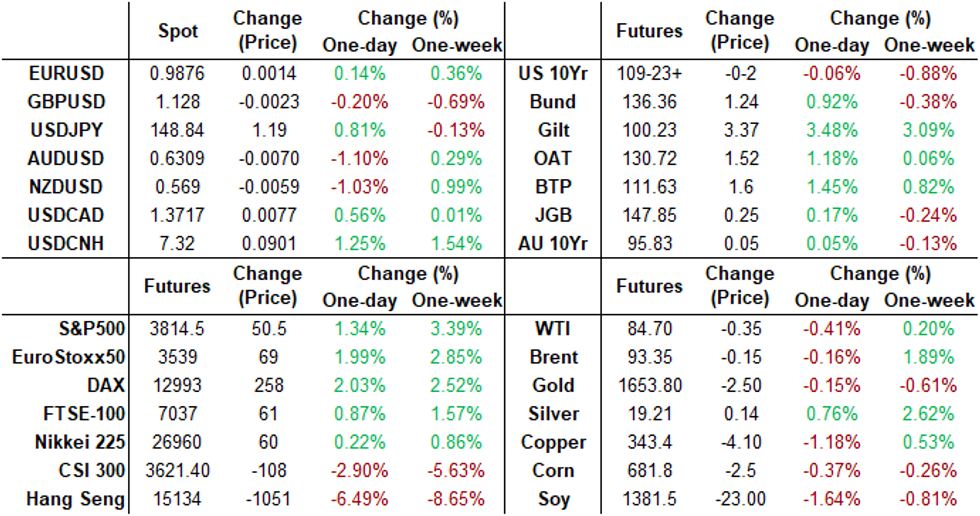

EGBs-GILTS CASH CLOSE: UK Yields Drop Sharply As Sunak Seals Win

GIlts easily outperformed global core FI peers Monday, with ex-UK Chancellor Sunak's victory in the Conservative leadership race appearing to augur renewed political and policy certainty.

- Indeed, 30Y UK yields nearly returned to pre-mini budget levels, with the UK curve bull steepening as BoE hike pricing subsided. BoE's Ramsden was the lone Europe central bank speaker, and said it was "really important" for the MPC to get fiscal clarity in time for the November policy decision.

- The German curve bull flattened. Weaker-than-expected European PMIs didn't bring any immediate market reaction upon release, but helped set a constructive tone for the FI session.

- Periphery EGBs outperformed Bunds: 10Y Greek spreads fell 12.4bp, with gains accelerating after PDMA announced a FRN auction Tuesday.

- The ECB decision looms large Thursday - our preview, looking for a 75bp hike, went out today (see here).

CLOSING YIELDS / 10-YR PERIPHERY EGB SPREADS TO GERMANY:

- Germany: The 2-Yr yield is down 3.5bps at 2.006%, 5-Yr is down 6.4bps at 2.148%, 10-Yr is down 8.7bps at 2.33%, and 30-Yr is down 10.4bps at 2.338%.

- UK: The 2-Yr yield is down 37.2bps at 3.427%, 5-Yr is down 33bps at 3.823%, 10-Yr is down 30.8bps at 3.746%, and 30-Yr is down 30.4bps at 3.756%.

- Italian BTP spread down 7.4bps at 225.6bps / Greek down 12.1bps at 252.2bps

EGB Options: ECB Week Starts With Euribor Downside Unwinds

Monday's Europe rates / bond options flow included:

- RXZ2 142/146 call spds, bought for 49 in 14k

- ERZ2 97.50/97.25/97.00 put fly sold at 1.75 in 5k (hearing unwind)

- ERZ2 97.75/97.50/97.25 put fly sold at 5.75 in 5k (also potentially unwinding: was bought for 3.25 in 10.5k (Sep 13th))

FOREX: CNH, AUD & NZD Consolidate Overnight Weakness Amid Sour Risk Backdrop

- Sentiment across global currency markets remains sour to start the week as Chinese stock markets registered one of their worst sessions since the financial crisis of 2008. Amid the declines, the yuan weakness extended and USDCNH is now seen comfortably north of the 7.30 mark.

- Technical trend readings are unsurprisingly in a bull mode position. Moving average studies, a positive price sequence of higher highs and higher lows and rising momentum, all point to a continuation higher in the pair. Initial resistance is seen at 7.3693, a Fibonacci projection of the Sep 12 - 28 - Oct 5 price swing.

- Markets will remain on watch for any further intervention following state banks supposedly selling dollars to contain the CNY weakness last week. Initial support is at 7.1611, the 20-day EMA.

- Amid the more pessimistic risk backdrop, AUD and NZD both sold off over 1% during APAC trade and have consolidated their declines throughout Monday.

- EURUSD (+0.10%) has largely shrugged off a dire set of PMI manufacturing and services numbers from across Germany and France, with conviction light ahead of the ECB rate decision on Thursday.

- In similar vein, GBP remains close to unchanged as the election of Rishi Sunak as the new PM provides a slightly more optimistic view for UK investors.

- Japanese authorities have yet to confirm that they were behind the steep JPY rallies seen on Friday and overnight on Monday. Despite the rapid sell-off to fresh lows at 145.56, JPY is also among the poorest performers on Monday following a firm USDJPY bounce to around the 149 level.

- A fairly light data calendar on Tuesday with German IFO and US consumer confidence expected. The ECB meeting remains the key event risk this week with central bank meetings in both Canada and Japan also in focus.

FX: Expiries for Oct25 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9745-50(E1.2bln), $0.9775-90(E1.3bln), $0.9800-05(E927mln)

- USD/JPY: Y145.00($2.4bln), Y145.65($1.45bln), Y150.00($1.2bln)

- GBP/USD: $1.1435(Gbp1.0bln)

- AUD/USD: $0.6600(A$759mln)

- USD/CAD: C$1.3500($550mln), C$1.3900($500mln)

- USD/CNY: Cny7.2000($830mln), Cny7.2500($1.0bln)

Late Equity Roundup: Maintaining Gains

Stocks continue to trade near top end NY session range, Health Care and Consumer staples sectors leading SPX eminis currently trading +48.25 (1.28%) at 3812.25; DJIA +482.67 (1.55%) at 31564.87; Nasdaq +81.6 (0.8%) at 10940.79.

- SPX leading/lagging sectors: Health Care (+2.00%) as pharmaceuticals and biotech shares outpace equipment makers. Consumer Staples (+1.79%) next up, road and rail stocks supporting followed by Financials (+1.69%) as insurance names outpace banks. Laggers: Real Estate (+0.06%), Materials (+0.17%) and Consumer Discretionary (+0.18%), autos and consumer services weighing on the latter.

- Dow Industrials Leaders/Laggers: Carry-over bid in United Health (UNH) +8.10 at 541.83, Amgen (AMGN) +7.81 at 259.75, Home Depot (HD) +7.00 at 282.53. Laggers: Chevron (CVX) -0.27 at 172.92, Disney (DIS) -.11 at 101.93 and

Nike (NKE) -0.06 at 88.44. - Reminder: Q3 equity earning annc's pick up in earnest tomorrow: sampling of pre-open annc: United Parcel Service (UPS) $2.847 est; General Motors (GM) $1.893 est; General Electric (GE) $0.468 est;

E-MINI S&P (Z2): Key Short-Term Resistance Remains Exposed

- RES 4: 4023.44 61.8% retracement of the Aug 16 - Oct 13 downleg

- RES 3: 3923.88 50.0% retracement of the Aug 16 - Oct 13 downleg

- RES 2: 38300.64 50-day EMA

- RES 1: 3820.00 High Oct 5 and a bull trigger

- PRICE: 3811.50 @ 1455ET Oct 24

- SUP 1: 3641.50 Low Oct 21

- SUP 2: 3590.50/3502.00 Low Oct 17 / 13 and the bear trigger

- SUP 3: 3491.13 50.0% retracement of the 2020 - 2022 bull cycle

- SUP 4: 3453.78 1.618 proj of the Aug 16 - Sep 7 - 13 price swing

S&P E-Minis is holding on to the bulk of its recent gains and maintains a firmer short-term tone. A bullish theme follows the reversal from 3502.00, the Oct 13 low. The recovery suggests the contract has entered a corrective phase and if correct, this is allowing an oversold trend condition to unwind. Attention is on resistance at 3820.00, the Oct 5 high and a bull trigger. Key support is unchanged at 3502.00. Initial support is at 3641.50, the Oct 21 low.

COMMODITIES: Natural Gas Slides On Reduced Short-Term Disruption Fears

- Another volatile session for crude oil, on balance edging lower on weak China demand, with volatility from uncertainty of both demand and supply. Goldman sees WTI averaging $99.8/bbl in 2022, $105/bbl 2023, Brent averaging $104.2/bbl in 2022, $110/bbl 2023.

- European gas meanwhile saw large declines, with TTF falling -13% due to the warm start to the winter and increasing storage levels to 93.4%, easing fears of short-term supply disruptions.

- WTI is -0.4% at $84.70, with resistance seen at $87.14 (Oct 20 high) and support at $81.3 (Oct 18 low).

- Relatively limited activity in CLZ2 strikes today, with the most active seen in $85/bbl and $90/bbl calls followed by $75/bbl puts.

- Brent is -0.2% at $93.34, with resistance seen at $95.17 (Oct 12 high) and support at $88.67 (61.8% retrace of Sep 26 – Oct 10 rally).

- Gold is -0.4% at $1651.4, extremely briefly touching a high of $1670.5 that forms initial resistance with sterner resistance potentially at the 50-day EMA of $1693.4, whilst support is seen at the bear trigger of $1615 (Sep 28 low).

Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 25/10/2022 | 0600/0800 | ** |  | SE | PPI |

| 25/10/2022 | 0700/0900 | ** |  | ES | PPI |

| 25/10/2022 | 0800/1000 | *** |  | DE | IFO Business Climate Index |

| 25/10/2022 | 0855/0955 |  | UK | BOE Pill at ONS ‘Understanding the cost of living through statistics’ | |

| 25/10/2022 | 0900/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 25/10/2022 | 1000/1100 | ** | | UK | CBI Industrial Trends |

| 25/10/2022 | 1230/0830 | ** |  | US | Philadelphia Fed Nonmanufacturing Index |

| 25/10/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 25/10/2022 | 1300/1500 | ** |  | BE | BNB Business Sentiment |

| 25/10/2022 | 1300/0900 | ** | | US | S&P Case-Shiller Home Price Index |

| 25/10/2022 | 1300/0900 | ** | | US | FHFA Home Price Index |

| 25/10/2022 | 1400/1000 | *** | | US | Conference Board Consumer Confidence |

| 25/10/2022 | 1700/1300 | * | | US | US Treasury Auction Result for 2 Year Note |

| 25/10/2022 | 1755/1355 | | US | Fed Governor Christopher Waller |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.