Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- MNI BRIEF: EU Struggles For Agreement On New Russia Sanctions

- FED’S COLLINS: RISK OF OVERTIGHTENING ON RATES HAS INCREASED, Bbg

- KRUGMAN: CPI REPORT IS PORTRAIT OF WHERE ECONOMY WAS LAST WINTER, Bbg

- KRUGMAN: ECONOMY'S SITUATION NOW `PROBABLY A LOT MORE FAVORABLE', Bbg

- FTX Files for Chapter 11 Bankruptcy; CEO Resigns, DJ

Key links: MNI INTERVIEW: Cooldown in Oct CPI Overstated -Fed's Meyer / MNI US Inflation Insight, Nov'22: Progress But Too Soon To Declare Victory / MNI INTERVIEW: Americans Fear Recession, Weaker Jobs-UMich

Tsys Weaker, But Near Highs, Dec Step-Down Still Alive

Still weaker, Tsys near top end of session (and overnight range, for that matter) amid two-way positioning ahead the weekend. Light volumes (TYZ2<650k) due to Veterans Day/bank holiday despite full session hours on screen.

- Tsys pared back a small portion of Thu's post-CPI rally, opening moderately lower Friday. Markets still digesting the Oct CPI data: An unexpectedly softer U.S. CPI report for October paints a rosier picture of moderating inflation than is likely the case, Atlanta Fed economist Brent Meyer told MNI.

- Roughly 60% of the CPI basket is still rising at rates above 5%, and alternative measures of underlying inflation remain "very elevated, reflecting broad-based price pressure," he said.

- Little react to preliminary November reading of consumer sentiment from the University of Michigan of 54.7 vs. 59.5 est. Rates and equities gradually pared losses (stocks posting gains in the second half) as participants square up ahead the weekend, slow start to next week.

- Fed Gov Waller kicks things off Sunday evening from Australia. PPI data on Tuesday. Tsy coupon supply starts Wednesday w/ $15B 20Y Bond, 10Y TIPS re-open on Thursday.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N +0.00000 to 3.81486% (-0.00143/wk)

- 1M +0.00215 to 3.87529% (+0.01715/wk)

- 3M -0.04357 to 4.60614% (+0.05585/wk) * / **

- 6M -0.04957 to 5.08400% (+0.07271/wk)

- 12M -0.18000 to 5.45129% (-0.21514/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 4.64971% on 11/10/22

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Robust option trade Friday, despite the Veterans Day bank holiday hampering underlying futures volumes (TYZ2<650k by the close). Mixed flow appeared to favor downside put buying in SOFR and Treasury 10Y options, carry-over vol selling in the former (-17,750 SFRU3 95.37 straddles, 82.0 (-34,750 SFRU3 95.50 straddles yesterday from 84.5-83.0).- SOFR Options:

- Block, -10,000 SFRZ2 97.00/Blue Nov 97.75 call spd, 0.5, steepener/Blues sold over

- Block, 20,000 SFRM3 95.25/95.75 call spds, 14.25/splits ref 95.155

- Block, 20,000 SFRH3 95.00/95.50 put spds, 30.0-30.5 ref 95.13

- Block, +5,000 SFRM3 94.75/95.50 put spds, 38.0 ref 95.145

- Blocks, total +40,000 SFRH 95.25/95.5 put spds, 40.0 ref 95.12

- 2,000 SFRM/SFRU 93.50/94.00/94.50 put fly spd

- 1,000 SFRZ2 95.50/95.56/95.62/95.68 call condors

- Block, 2,500 SFRZ2 95.12/95.37/95.62 2x3x1 put flys, 10

- 2,250 SFRZ2 95.12/95.37 2x3 put spds

- 2,000 SFRG3 95.18/95.37 call spds

- 2,000 SFRZ2 95.62/96.12/96.62 call flys

- Block, 1,900 SFRG3 95.18/95.37 call spds, 6.0 vs. 95.11

- Blocks, -17,750 SFRU3 95.37 straddles, 82.0 (-34,750 SFRU3 95.50 straddles yesterday from 84.5-83.0)

- 4,000 SFRZ2 95.75/95.87 call spds

- Eurodollar Options:

- 7,500 Mar 97.50 calls, 1.0

- 2,000 Dec 95.25/95.47 call spds

- Treasury Options:

- 2,500 TYZ 114 calls, 5 ref 112-06.5

- 8,200 TYZ 109 puts, 3 ref 112-06.5

- +7,500 TYZ 109.25 puts, 3 ref 112-06.5

- 5,000 TYZ 113/114 call spds, 13 ref 112-11

- 3,500 FVZ 108.5 calls ref 107-28

- 1,300 FVZ 109/110 call spds, ref 107-25

- 2,000 TYZ 110/111 put spds, 8 ref 95.485

EGBs-GILTS CASH CLOSE: Bunds Give Up Thursday's Gains

German yields rose sharply to close the week as ECB dovishness was reconsidered, reversing most of Thursday's fall, with Gilts also weakening but outperforming Bunds. Trading was thinner than usual, with several US markets on holiday.

- ECB and BoE terminal rate hike pricing bounced from Thursday's lows, returning to pre-US CPI release levels.

- UK Sept GDP came in weaker than expected, but the reading was distorted by the impact of an additional bank holiday. No real surprises for the BoE.

- ECB's de Cos said the QT start date could be announced in December.

- Periphery spreads were mixed: BTPs gave back some of Thursday's spread tightening, while GGBs outperformed.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 12.7bps at 2.207%, 5-Yr is up 16bps at 2.087%, 10-Yr is up 15.1bps at 2.16%, and 30-Yr is up 11.4bps at 2.112%.

- UK: The 2-Yr yield is up 6.2bps at 3.165%, 5-Yr is up 5.8bps at 3.367%, 10-Yr is up 6.6bps at 3.358%, and 30-Yr is up 8.5bps at 3.491%.

- Italian BTP spread up 5.3bps at 204.5bps / Greek down 6.1bps at 237.5bps

EGB Options: Limited Bund Trade To End The Week

Friday's Europe rates / bond options flow included:

- RXZ2 139/136ps 1x2, bought in 1.7k vs RXZ2 142c sold in 3.4k, traded for 23.

- RXF3 142/144cs, bought for 33 in 5.5k

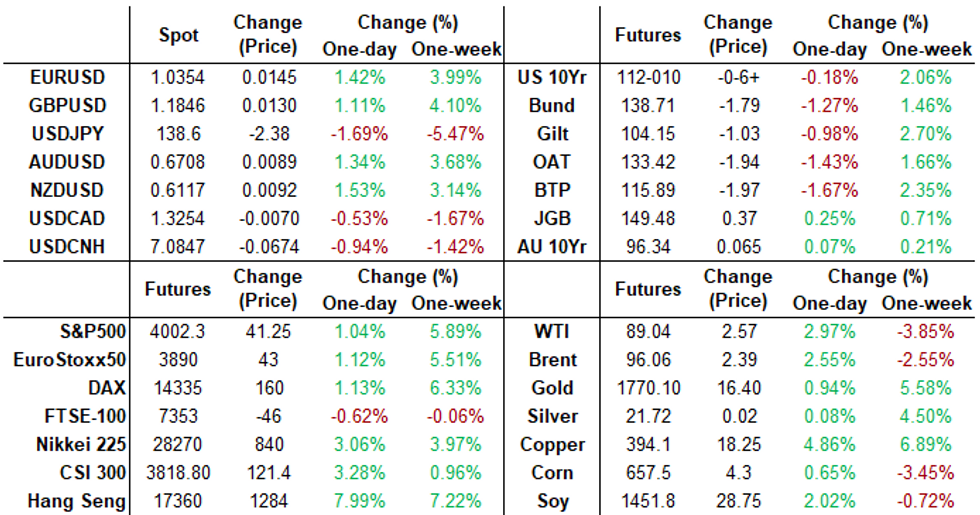

FOREX: USD Index Extends Two-Day Decline To 3.2%

- Despite several comments from both Fed members and treasury Secretary Yellen highlighting that it is too early to declare victory over inflation, the greenback continues to slide following the lower US CPI figures on Thursday.

- Furthermore, overnight news of China’s freshly optimised COVID restrictions (which include a rollback of the country’s international travel restrictions and reduced quarantine time for international travellers) has resulted in a fresh round of risk-positive flows as we approach the end of the trading week.

- The extension of USD weakness has been broad based, with EUR, JPY, AUD and NZD all rising over 1% and extending the impressive rallies from Thursday. EURUSD looks set to retest the significant resistance zone between 10350-68, with the latter level representing the Aug 10, high.

- USDJPY also maintained high levels of volatility, briefly printing 138.78 during the European session, an impressive 769 pips below yesterday’s opening price. Price action stabilised somewhat during the US (Veteran’s Day Holiday) session but remains within 50 pips of the lows approaching the close.

- The Swiss Franc (+1.82%) is among the strongest performers in G10, receiving an additional tailwind from forceful SNB rhetoric, confirming the bank will use "all measures necessary" which could include currency intervention. USDCHF is rapidly approaching key resistance at 0.9371, the August lows.

- A much quieter week for data next week, with UK and Canadian CPI the highlights on Wednesday.

Expiries for Nov14 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0000(E1.2bln), $1.0025-30(E568mln)

- GBP/USD: $1.1715(Gbp557mln)

- AUD/USD: $0.6920-30(A$903mln)

- EUR/JPY: Y146.00(E1.4bln)

Late Equity Roundup: Extending Highs, SPX Nears Resistance

Stocks adding to Thu's huge post-CPI relief rally, SPX nearing technical resistance as it extends rally in late trade, Energy, Communication Services and Consumer Discretionary outperforming. SPX eminis currently trading +44.75 (1.13%) at 4006.5; DJIA +52.86 (0.16%) at 33772.25; Nasdaq +231.6 (2.1%) at 11346.96.- SPX cleared a key resistance at 3928.00, the Nov 1 high Thu -- strengthening short-term bullish condition and price has establishing a sequence of higher highs and higher lows on the daily scale. This signals scope for gains towards 4023.44 next, a Fibonacci retracement.

- SPX leading/lagging sectors: Energy (+3.23%) sector lead by oil and gas shares: Occidental Petro (OXY) +5.60%, Phillips66 +5.46%, Devon Energy (DVN) +4.20%. Next up: Communication Services (+2.95%) lead by media and entertainment shares: Paramount +14.48%, WBD +10.5%, DIS +4.95%, NFLX +5.3%. Laggers: Health Care (-1.66%), Utilities (-1.36%) and Consumer Staples (-0.59%).

- Dow Industrials Leaders/Laggers: Goldman Sachs (GS) +8.07 at 386.38, Nike (NKE) +7.19 at 106.68, Home Depot (HD) +5.15 at 316.85. Laggers: United Health (UNH) - 30.40 at 513.77, Amgen (AMGN) -7.20 at 283.73, JNJ -5.57 at 168.96.

E-MINI S&P (Z2): Bullish Outlook

- RES 4: 4175.00 High Sep 13 and a key resistance

- RES 3: 4146.63 76.4% retracement of the Aug 16 - Oct 13 downleg

- RES 2: 4100.00 Round number resistance

- RES 1: 4023.44 61.8% retracement of the Aug 16 - Oct 13 downleg

- PRICE: 4008.50 @ 1500ET Nov 11

- SUP 1: 3830.80 50-day EMA

- SUP 2: 3750.00 Low Nov 9

- SUP 3: 3704.25 Low Nov3 and key short-term support

- SUP 4: 3641.50 Low Oct 21

S&P E-Minis rallied sharply higher Thursday and in the process cleared a key resistance at 3928.00, the Nov 1 high. The break of this hurdle strengthens a short-term bullish condition and price has established a sequence of higher highs and higher lows on the daily scale. This signals scope for gains towards 4023.44 next, a Fibonacci retracement. On the downside, key short-term support has been defined at 3704.25, the Nov 3 low.

COMMODITIES: Oil Boosted By China Reducing Quarantine Rules, Still Ends Wk Lower

- Crude oil prices extended yesterday’s post-US CPI rally with a sharper increase with China reducing international travel and quarantine restrictions, whilst OPEC+ will remain cautious on production according to Saudi Arabia’s energy minister. Demand fears have continued to weigh over the week though, with prices still down 3-4.5%.

- Reuters reports that insurers could stay away from new contracts if there aren’t additional details from G7/EU on oil price cap.

- WTI is +2.4% at $88.52, having cleared resistance at $89.24 (Nov 9 high) to potentially open key resistance at $93.74 (Nov 7 high). Most active strikes in the CLZ2 have been $92/bbl and $91/bbl calls.

- Brent is +2.0% at $95.50 off a high of $96.92, remaining below the bull trigger of $99.56 (Nov 7 high).

- Gold is +0.5% at $1765.1, finding resistance at $1765.5 (Aug 25 high), clearance of which could open the psychological $1800.0.

- Weekly: WTI is -4.5%, Brent is -3.1%, Gold is +5.0%, US Nat Gas -8.4%, EU TTF Gas -14.8% as EU gas prices extend declines with strong LNG flows and near full storage levels.

Monday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 13/11/2022 | 2130/1630 |  | US | Fed Governor Christopher Waller | |

| 14/11/2022 | 0001/0001 |  | UK | Rightmove House Prices | |

| 14/11/2022 | 1000/1100 |  | EU | ECB Panetta Speech at CEPR-EABCN Conference | |

| 14/11/2022 | 1000/1100 | ** | | EU | Industrial Production |

| 14/11/2022 | - | | UK | House of Commons Returns | |

| 14/11/2022 | - |  | TH | APEC Leaders’ Summit | |

| 14/11/2022 | 1345/0845 |  | CA | BOC's Macklem opening remarks at diversity conference | |

| 14/11/2022 | 1600/1100 | ** | | US | NY Fed survey of consumer expectations |

| 14/11/2022 | 1615/1715 | | EU | ECB de Guindos Speech at Euro Finance Week | |

| 14/11/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 14/11/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 14/11/2022 | 1630/1130 | | US | Fed Vice Chair Lael Brainard | |

| 14/11/2022 | 2330/1830 | | US | New York Fed's John Williams |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.