Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- Tsy Sec Yellen: "Q3 GDP data shows ample signs of strength in the US economy."

- ECB DIDN'T MEAN TO IMPLY SLOWER HIKING WITH `PROGRESS' REMARK, Bbg

- ECB LAGARDE: WE'LL DECIDE PRINCIPLES OF PORTFOLIO REDUCTION IN DEC, Bbg

- PENTAGON WON’T RULE OUT NUCLEAR USE AGAINST NON-NUCLEAR THREATS, Bbg

US TSYS: Bonds Near Post-ECB Highs

Treasury futures trade stronger after the bell, see-sawing in relative narrow range since surging higher in midmorning trade; 30YY currently -.0338 at 4.1042% vs. 4.0571% L/4.2033% H.

- Impetus largely after ECB policy annc: though in-line w/ expected 75bp rate hike, markets fixated on discussion over ECB forward rate guidance turns dovish (though ECB Lagarde admits job of normalizing rates not finished, did not discuss QT).

- Not as striking as Wed's less than expected 50bp hike from the BOC, but US markets nervous over additional 75bp rate hikes going into year-end, are eager to take the cue and (continue) to unwind restrictive expectations into year end.

- As noted Wed, foreign central bank decisions unlikely to sway the FOMC, particularly next wk's annc where 75bp is considered a lock. Fed Chairman Powell likely to push back on less hawkish rate hike optimism and reiterate Sep messaging/DOT plot guidance. (Reminder: next employment report (covering October) is on November 4 - after the FOMC. An in-line read will likely tip the scales back toward 75bp hike in Dec).

- Data roundup: Tsys pared losses after round of mixed to in-line data: Q3 GDP better than exp (+2.6% vs. +2.4% est), core PCE and weekly jobless claims largely in-line (continuing claims higher 1.438M vs. 1.390M est), durable goods weaker than exp (0.4% vs. 0.6% est).

- Tsys dip/pare gains slightly after $35B 7Y note auction (91282CFT3) tails: 4.027% high yield vs. 4.017% WI; 2.43x bid-to-cover vs. 2.57x last month.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N +0.00243 to 3.06329% (-0.01843/wk)

- 1M +0.12157 to 3.75386% (+0.16829/wk)

- 3M +0.04085 to 4.41471% (+0.05628/wk) * / **

- 6M -0.00357 to 4.92829% (+0.05329/wk)

- 12M -0.02100 to 5.37243% (-0.10314/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 4.41471% on 10/27/22

- Daily Effective Fed Funds Rate: 3.08% volume: $99B

- Daily Overnight Bank Funding Rate: 3.07% volume: $282B

- Secured Overnight Financing Rate (SOFR): 3.03%, $972B

- Broad General Collateral Rate (BGCR): 3.00%, $402B

- Tri-Party General Collateral Rate (TGCR): 3.00%, $381B

- (rate, volume levels reflect prior session)

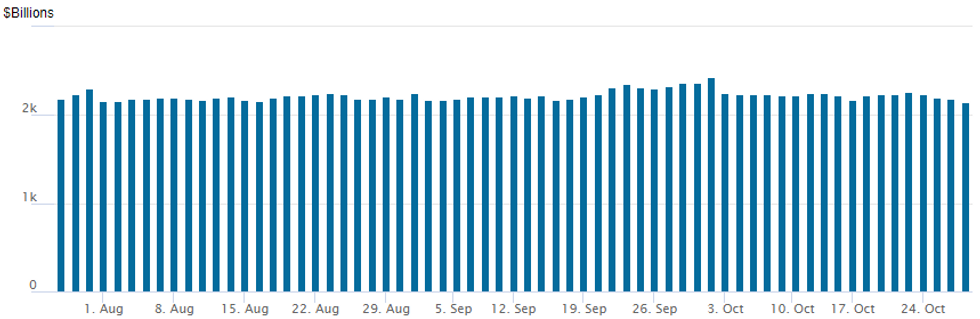

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $2,152.485B w/ 97 counterparties vs. $2,186.856B in the prior session. Prior record high stands at $2,425.910B on Friday, September 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Thursday FI option trade centered on two-way call positioning as opinion over FOMC hike pricing into year-end fluctuated. Much better Tsy option volumes, Eurodollar volumes scant.- Some highlight trade/blocks included: +10,000 TYZ2 113.25 calls, 35 ref 111-21 followed by another 12k on screen soon after. Same premium paid for the TYZ 113 calls a few minutes prior - moving up strikes as underlying continues to rally.

- Traders reporting two-way skew trade in upside calls as underlying ratchets higher: -5,000 TYZ2 109.5/113.75 call over risk reversal after +7,500 wk2 TY 112/TYF 113 call diagonal from 20-21.

- On the flipside: early put buyers fading the initial post-ECB bounce: Block, +10,000 TYZ 109.25 puts, 30, another 9,000 on screen in addition to 4,000 TYZ2 108/109 put spds, 10 ref 111-15.5.

- SOFR Options:

- +10,000 SFRF3 95.12/95.25/95.62/96.25 call condors, 2.25

- +4,000 SFRM3 96.87 calls, 7.5 vs 95.22/0.08%

- Block 6,000 SFRX2 95.50/95.62/95.75 call flys, 2.0 vs. 95.44/0.10%

- Eurodollar Options:

- +1,000 Jan 95.43/95.75 1x2 call spds, 0.25 cr

- Treasury Options:

- +5,750 TYZ 108/108.25/109.5 broken put flys steady to TYZ 112.25/112.75 call spds

- Block, 6,500 w4 TY 110.25/111.25 2x3 call spds

- -5,000 TYZ2 109.5/113.75 call over risk reversal

- +7,500 wk2 TY 112/TYF 113 call diagonal from 20-21

- Block, 10,000 TYZ2 113.25 calls, 35 re 111-21

- Block, +10,000 TYZ2 113 calls, 35 ref 111-18, another 8.5k on screen

- Block, +10,000 TYZ 109.25 puts, 30

- +2,000 TYZ 114 calls, 17

- 4,000 TYZ2 108/109 put spds, 10 ref 111-15.5

- 2,000 TYZ2 114/116 call spds 4 over wk1 TY 113 calls

- 1,250 TYZ 111.25/111.75/112.25/112.75 call condors, 44

- Block, 15,000 TYZ2 112.75/114 call spds, 16 vs. 110-30.5/0.12%

- 3,000 USZ 115/117/118/120 USZ2 put condors

- Block: 10,000 FVZ2 105.5/106.75 put spds, 31.5 vs. 106-20/0.30%

EGBs-GILTS CASH CLOSE: ECB Takes A Dovish Turn

EGBs rallied strongly Thursday in the wake of the ECB's policy decision, with the expected 75bp hike accompanied by a Statement pointing to a softer rate hike path ahead.

- In particular phrase “expects to raise interest rates further” dropped “over the next several meetings”, with the ECB emphasising a meeting-by-meeting approach.

- Terminal rate pricing fell 30bp (2.55% Jul 2023), helping the short-end / belly of the German curve outperform.

- Periphery EGBs outperformed with BTPs gaining most: initially on the more dovish ECB rate outlook and accelerating after Lagarde said the Governing Council "deliberately" didn't discuss QT in a substantive way.

- The UK curve underperformed Germany at the short end, but outperformed through the rest of the curve. The BOE confirmed the first QT Gilt sale will take place on Nov 1.

- German state inflation is the highlight first thing Friday morning.

CLOSING YIELDS / 10-YR PERIPHERY EGB SPREADS TO GERMANY:

- Germany: The 2-Yr yield is down 17.2bps at 1.773%, 5-Yr is down 17.9bps at 1.818%, 10-Yr is down 14.9bps at 1.962%, and 30-Yr is down 9.6bps at 2.011%.

- UK: The 2-Yr yield is down 14bps at 3.138%, 5-Yr is down 18.3bps at 3.48%, 10-Yr is down 17.3bps at 3.403%, and 30-Yr is down 16.8bps at 3.51%.

- Italian BTP spread down 17.2bps at 204.6bps / Greek down 8.6bps at 244.3bps

EGB Options: Unwinding Upside Ahead Of ECB, Buying It After ECB

Thursday's Europe rates / bond options flow included:

- DUZ2 107.50 call sold at 14 and 16.5 in 7.5k

- DUZ2 106.80/106.20 1x2 put spread bought for 10 in 2k. Total of 5k, paying 10 &10.5

- RXZ2 140/142/143 broken call flys for 37 in 2k

- ERM3 97.50/97.625/98.25 call ladder bought for -1 (net credit) In 40K

- 2RH3 98.00/98.25 call spread sold at 4 in 2.5k. Hearing unwinding of upside

FOREX: ECB Fails To Bolster Recent Euro Optimism, Greenback Recovers

- Having recently broken above 2022 channel resistance, EURUSD extended gains overnight to trade at a six-week high of 1.0094, however, Thursday saw a sharp reversal for the single currency.

- Despite the ECB delivering its second 75bps hike in two meetings, the Governing Council appeared to suggest a slowdown is likely, following “substantial progress” in the withdrawal of monetary policy accommodation.

- EURUSD is hugging intra-day lows approaching the APAC crossover, back below parity and down 1.15% for the session. On the downside, support to watch is 0.9856, the former bear channel resistance.

- Losses have been even more pronounced in EURJPY (-1.32%). Despite the sharp fall, moving average studies continue to highlight a bullish backdrop and the cross will focus on strong support at 143.80, Monday’s low and just below the 20-day exponential moving average.

- Single currency declines have boosted the USD index (+0.80%), however, some strong performances in emerging markets, especially in LatAm FX, are offsetting the greenback resurgence with dollar indices remaining substantially lower on the week.

- Bank of Japan highlights the Friday calendar in APAC trade, with their decision and Monetary Policy Statement due. A mixture of European GDP and CPI data releases will follow. Canadian GDP crosses alongside US Core PCE Price Index, before US pending home sales and UMich confidence data rounds off the week.

FX: Expiries for Oct28 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9800(E892mln), $0.9900(E551mln), $0.9975(E632mln), $1.0000(E1.6bln), $1.0100(E758mln), $1.0200(E912mln)USD/JPY: Y147.00($505mln)

- EUR/JPY: Y146.50(E1.0bln)

- GBP/USD: $1.1000(Gbp1.3bln), $1.1210(Gbp758mln)

- USD/CAD: C$1.3690-05($550mln)

- USD/CNY: Cny7.00($4.0bln)

Late Equity Roundup: META Hammered, Down Near 25%

Stocks pared gains (DJIA) / inched lower (SPX/NDX) late Thursday, Communications Services and Information Technology sectors weighing. SPX eminis currently trading -22 (-0.57%) at 3819.25; DJIA +244.85 (0.77%) at 32084.92; Nasdaq -181.9 (-1.7%) at 10789.36.

- SPX leading/lagging sectors: Communication Services (-4.02%) weighed by interactive media/services: META (formerly Facebook) gave back nearly 25% of it's share price on the day: -31.75 at 98.07; Information Technology (-1.09%) follows as hardware and equipment peripherals underperform: Micron (MU) -5.3%, Apple -3.32%, Intel (INTC) -2.88%.

- Leaders: Industrials (+1.46%) lead by machine makers (Caterpillar/CAT +8.52% after strong earnings +$3.95 vs. $3.178 est) followed by Financials (+0.91%), Utilities (+0.74%) and Energy (+0.59%) the latter lead by oil and gas names (Marathon/MRO +2.09%, Phillips 66/PSX +1.78%, Valero/VLO +1.52%).

- Dow Industrials Leaders/Laggers: Caterpillar (CAT) surges +15.70 at 212.66, McDonalds (MCD) +8.91 at 265.52, Honeywell (HON +7.20 at 197.47. Laggers: Microsoft (MSFT) extends Wed's sell-off -4.99 at 226.33, Apple (AAPL) -4.99 at 144.36, Intel (INTC) -0.78 at 26.43.

E-MINI S&P (Z2): Short-Term Trend Needle Points North

- RES 4: 4023.44 61.8% retracement of the Aug 16 - Oct 13 downleg

- RES 3: 3981.25 High Sep 14

- RES 2: 3923.88 50.0% retracement of the Aug 16 - Oct 13 downleg

- RES 1: 3874.25 High Oct 26

- PRICE: 3824.00@ 1515ET Oct 27

- SUP 1: 3752.20/3641.50 20-day EMA / Low Oct 21

- SUP 2: 3590.50/3502.00 Low Oct 17 / 13 and the bear trigger

- SUP 3: 3491.13 50.0% retracement of the 2020 - 2022 bull cycle

- SUP 4: 3453.78 1.618 proj of the Aug 16 - Sep 7 - 13 price swing

S&P E-Minis maintains a bullish tone and the contract is holding the bulk of its recent gains. This week’s climb has resulted in a break of the 3820.00 hurdle, Oct 5 high. Furthermore, price is trading above the 50-day EMA, at 3831.76. The break higher strengthens the short-term bullish condition and signals scope for a climb towards 3923.88, a Fibonacci retracement. On the downside, key short-term support has been defined at 3641.50.

COMMODITIES: Crude Oil Eyes Key Resistance After Demand Boost

- Crude oil has been boosted further today by slightly stronger than expected Q3 GDP (2.6% vs 2.4 cons) with a larger beat for consumption although the gloss was taken off by disappointing core durable goods orders at the tail end of the quarter.

- Further, US petroleum exports hit a record 11.4mln bpd last week as domestic inventories are at historic lows, with gasoline prices jumping as NY area supplies hit ten-year seasonal lows, whilst Iraq’s parliament has voted in a new oil minister.

- WTI is +1.3% at $89.08 having cleared resistance at $88.66 (Oct 12 high) to open key resistance at $92.34 (Oct 10 high). More optimism around the recovery of Chinese demand could be needed to breach this level.

- Brent is +1.2% at $96.84 off a session high of $97.25 that came closer to the key near-term resistance of $98.75 (Oct 10 high).

- Gold is -0.3% at $1660.0, pulling away from initial resistance at yesterday’s high of $1674.9 but still some way off support at the bear trigger of $1615.0 (Sep 28 low).

Friday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/10/2022 | 0430/0630 | *** |  | DE | North Rhine Westphalia CPI |

| 28/10/2022 | 0530/0730 | ** |  | FR | Consumer Spending |

| 28/10/2022 | 0530/0730 | *** | | FR | GDP (p) |

| 28/10/2022 | 0600/0800 | *** |  | SE | GDP |

| 28/10/2022 | 0600/0800 | ** | | SE | Retail Sales |

| 28/10/2022 | 0645/0845 | *** | | FR | HICP (p) |

| 28/10/2022 | 0645/0845 | ** | | FR | PPI |

| 28/10/2022 | 0700/0900 | *** |  | ES | GDP (p) |

| 28/10/2022 | 0700/0900 | *** | | ES | HICP (p) |

| 28/10/2022 | 0700/0900 | * |  | CH | KOF Economic Barometer |

| 28/10/2022 | 0800/1000 | *** | | DE | GDP (p) |

| 28/10/2022 | 0800/1000 | *** | | DE | Bavaria CPI |

| 28/10/2022 | 0800/1000 | ** |  | IT | PPI |

| 28/10/2022 | 0900/1100 | *** | | IT | HICP (p) |

| 28/10/2022 | 0900/1100 | ** |  | EU | Economic Sentiment Indicator |

| 28/10/2022 | 0900/1100 | * | | EU | Consumer Confidence, Industrial Sentiment |

| 28/10/2022 | 0900/1100 | * | | EU | Business Climate Indicator |

| 28/10/2022 | 0900/1100 | *** | | DE | Saxony CPI |

| 28/10/2022 | 1030/1330 |  | RU | Russia Central Bank Key Rate Decision | |

| 28/10/2022 | 1200/1400 | *** | | DE | HICP (p) |

| 28/10/2022 | - | *** |  | JP | BOJ policy announcement |

| 28/10/2022 | 1230/0830 | *** |  | CA | Gross Domestic Product by Industry |

| 28/10/2022 | 1230/0830 | ** |  | US | Personal Income and Consumption |

| 28/10/2022 | 1230/0830 | ** | | US | Employment Cost Index |

| 28/10/2022 | 1400/1000 | ** | | US | NAR pending home sales |

| 28/10/2022 | 1400/1000 | *** | | US | Final Michigan Sentiment Index |

| 28/10/2022 | 1500/1100 | | CA | Finance Dept monthly Fiscal Monitor (expected) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.