Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- U.S. Tsys stuck to a narrow band overnight, with a downtick in e-minis eyed, even as Asia-Pac equity indices surged on the back of Wednesday’s developments. Tsys and e-minis were more cautious given U.S. warnings re: the potential for Russian deployment of chemical and/or biological weapons in Ukraine, while the proximity to today’s U.S. CPI print kept most on the sidelines.

- The USD was bid for most of Asia-Pac trade, although that has waned a little.

- The latest ECB monetary policy decision headlines the Eurozone economic docket on Thursday. U.S. CPI data then provides the focal point during NY hours. Participants will also look to the headlines surrounding the face-to-face meeting of the Russian & Ukrainian Foreign Ministers.

ECB: MNI ECB Preview - March 2022: Hawks Stand Down, For Now

- Having appeared to be gearing up to normalise monetary policy, the ECB’s calculus has now changed following the Russian invasion of Ukraine.

- For the time being, the direction of travel for monetary policy remains unchanged, but any momentum building behind a near-term tightening has subsided.

- The ECB will reconfirm the December policy calibration, but the narrative on the medium-term inflation outlook will now reflect the new two-way risks that have resulted from the Ukrainian crisis.

- For the full publication please see ECB Preview March 2022.pdf

US: MNI CPI Preview: Non-Core Components To Run Wild

Consensus has headline CPI surging +0.8% M/M in Feb on energy and less so food prices, of which the largest effects aren’t likely to show until March. That would see year-on-year inflation rise from 7.5% to 7.8% Y/Y.

- Whilst normally looked through, non-core gains will add pressures to areas that consumers feel the most and carry the risk of a further drifting in survey-based inflation expectations.

- Core inflation is seen at +0.5% M/M from the +0.58% M/M in Jan on a possible dip in used car prices, but with reasonable strength in other categories. That sees year-ago inflation rise from 6.0% to 6.4% Y/Y, potentially the peak for the cycle.

- The full report including MNI analysis and previews of 12 sell-side analysts has been e-mailed to subscribers and can be found here.

BONDS: Core FI Mixed Overnight, Risk Aplenty On Thursday

TYM2 +0-03 at 126-20+ into European hours, sticking to a 0-06+ range in Asia, while cash Tsys print 1.5-2.5bp richer. Tsys stuck to a narrow band overnight, with a downtick in e-minis eyed, even as Asia-Pac equity indices surged on the back of Wednesday’s developments. Tsys and e-minis were more cautious given U.S. warnings re: the potential for Russian deployment of chemical and/or biological weapons in Ukraine, while the proximity to today’s U.S. CPI print kept most on the sidelines. Flow was headlined by a 10K block roll from a long in the FVJ2 118.00 puts into the FVK2 117.00 puts. The latest ECB monetary policy decision will provide some interest ahead of NY hours. On top of the aforementioned CPI print, the NY session will bring weekly jobless claims data, average hourly earnings and 30-Year Tsy supply. Participants also eye headlines surrounding the face-to-face meeting between the Russian & Ukrainian Foreign Ministers.

- JGB futures were heavy, building on overnight losses as domestic equities surged and the rise in local PPI data topped expectations. The cover ratio crumbled at the latest round of 20-Year JGB supply, printing below 3.00x to hit the lowest level observed at a 20-Year JGB auction since the multi-year low observed back in October. Things were smooth enough on the pricing side, the price tail saw a modest widening, while the low price topped broader dealer expectations (BBG dealer median looked for a low price of 97.35). Market volatility continues to limit demand when it comes to JGB auctions. Not much was observed in the way of a meaningful immediate reaction in JGB futures or cash 20s post-auction, but the soft cover played into the weakness witnessed later in the afternoon, as 20s led the way lower on the curve. Futures were -33 at the close, while cash trade saw yields rise by 1.0-2.5bp across the curve. There wasn’t much in the way of meaningful domestic headline flow, outside of PM Kishida flagging the need for coordinated government strategy when it comes to combatting the well-documented inflationary pressures.

- Aussie bonds futures pulled back from their early peak as we moved through the session, with firmer Melbourne Institute inflation expectations data and Australian PM Morrison calling for an uptick in defence spending helping the direction of travel. That left YM -3.4 & XM -4.8 come settlement, with volume supported by roll activity. There was nothing in the way of notable market reaction when it came to the resignation of RBA Deputy Governor Debelle, with speculation already apparent re: his successor. The Bill strip twist steepened, with the front end helped by lower BBSW fixings (3- & 6-Month tenors).

JAPAN: Offshore Investors Bought Japanese Bonds & Sold Japanese Stocks Last Week

A quick look at the latest round of weekly international security flow data out of Japan revealed another week of net selling of foreign bonds on the part of Japanese investors, while the same cohort were once again net buyers of foreign equities (the net size of both of these rounds of flows wasn’t anything spectacular).

- Meanwhile, more interest will fall on foreign investors’ net flows surrounding Japanese assets. Foreign investors deployed the largest round of net weekly buying of Japanese bonds since early December, while foreign net sales of Japanese equities hit the highest level observed since September.

| Latest Week | Previous Week | 4-Week Rolling Sum | |

|---|---|---|---|

| Net Weekly Japanese Flows Into Foreign Bonds (Ybn) | -364.3 | -328.4 | -2571.3 |

| Net Weekly Japanese Flows Into Foreign Stocks (Ybn) | 285.7 | 110.1 | 451.7 |

| Net Weekly Foreign Flows Into Japanese Bonds (Ybn) | 1332.2 | -223.2 | 1157.9 |

| Net Weekly Foreign Flows Into Japanese Stocks (Ybn) | -910.3 | -402.6 | -1603.2 |

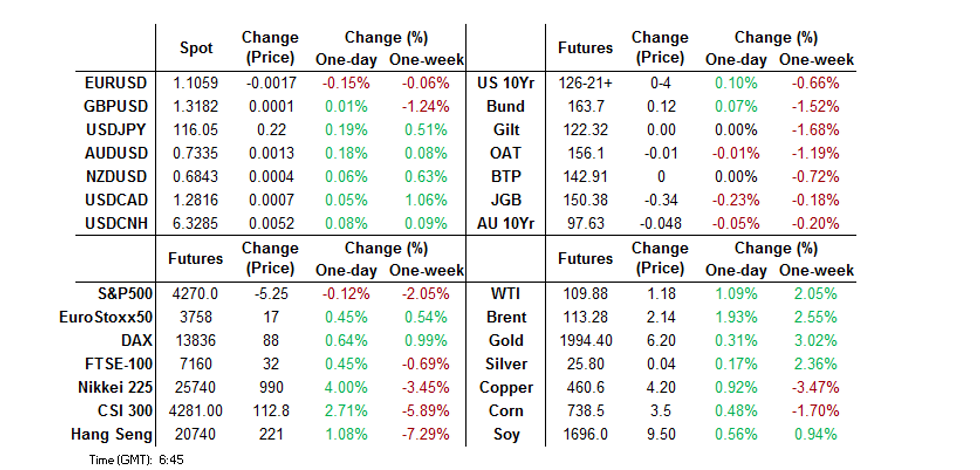

FOREX: USD Generally Firmer In Asia

The broader USD was bid in Asia-Pac dealing, finding some demand ahead of Thursday’s major risk events (see below for more on that), while some worry from the U.S. re: the potential for Russia to deploy chemical and/or biological weapons in Ukraine also played into the USD bid. A softer than expected CNY fixing pushed flows further in the USD’s favour, although the mover has moderated from extremes.

- EUR/USD lost some ground on the aforementioned USD bid, with the rate last dealing ~20 pips lower around $1.1050. Still, the recovery from fresh cycle lows registered earlier in the week has been impressive. Note that the EUR was the second worst performing currency in the G10 FX sphere in YtD terms come the close of play last week (with only the SEK providing worse YtD performance). Fortunes have changed during the current week, with the EUR finding itself second in the G10 currency sphere (only bettered by the SEK).

- The combination of buoyant Japanese equity markets, a generally firmer dollar in the G10 FX space, an uptick in oil (the level of Japan’s dependence on energy imports leaves it particularly exposed to crude price dynamics) and Tokyo fix-related demand pushed USD/JPY higher. The rate prints 25 pips firmer on the day, sitting at Y116.10. A reminder that meaningful resistance is located at the Feb 10 high/Jan 4 high & bull trigger (Y116.34/35).

- AUD fared better than most of its peers, looking through the unexpected resignation of RBA Deputy Governor Debelle, trading flat vs. the USD into European hours.

- The latest ECB monetary policy decision headlines the Eurozone economic docket on Thursday. Having appeared to be gearing up to normalise monetary policy, the ECB’s calculus has now changed following the Russian invasion of Ukraine. For the time being, the direction of travel for monetary policy remains unchanged, but any momentum building behind a near-term tightening has subsided. The ECB will reconfirm the December policy calibration, but the narrative on the medium-term inflation outlook will now reflect the new two-way risks that have resulted from the Ukrainian crisis. U.S. CPI data then provides the focal point during NY hours. Participants will also look to the headlines surrounding the face-to-face meeting of the Russian & Ukrainian Foreign Ministers.

FOREX OPTIONS: Expiries for Mar10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0950(E744mln), $1.1000(E1.8bln), $1.1020-25(E1.0bln), $1.1075-80(E652mln), $1.1150-55(E706mln)

- GBP/USD: $1.3280-00(Gbp603mln), $1.3500(Gbp758mln)

- USD/JPY: Y114.65-75($1.2bln), Y114.90($750mln), Y115.30-40($1.5bln), Y115.80-00($580mln), Y116.40($560mln)

- USD/CAD: C$1.2550($860mln), C$1.2750($755mln), C$1.2900($1.2bln)

EQUITIES: Higher In Asia After Crude Retreat

Virtually all Asia-Pac equity indices trade higher on a positive lead from U.S. and European markets, with the largest rallies observed in Japanese and Chinese benchmarks. Energy-related stocks across the region broadly lagged peers, tracking a pullback in major crude benchmarks on Wednesday.

- The Nikkei 225 has added 4.0% at writing, snapping a 4-day streak of losses, and is on track to record its largest daily gain in nearly ~21 months. Virtually all sub-indices within the index trade firmer at writing, with 221 of the 225 constituents recording gains. The largest gains were observed in materials and real estate, while energy and utilities brought up the rear.

- The CSI300 is 1.9% better off at writing, led by gains in richly valued consumer staples and healthcare equities. The index has risen off 20-month lows recorded on Wednesday, coming as several dozen Chinese large-caps were noted to have taken the unusual step of announcing corporate performance this week, ahead of expectations. The move has been broadly interpreted as being meant to “soothe” investor nerves, with state media also observed to have published articles emphasising the strength and stability of the Chinese economy on Thursday.

- U.S. e-mini equity index futures deal 0.2% to 0.3% softer at typing.

GOLD: Lower In Asia

Gold deals ~$15/oz lower to print $1,976.6/oz at writing. The precious metal trades around Wednesday’s troughs as hope for a diplomatic resolution to (or de-escalation in) the Russia-Ukraine conflict has received a boost, with Foreign Ministers from both Ukraine and Russia due to meet for talks later today.

- To recap, gold closed ~$60/oz lower on Wednesday, with the move lower facilitated by Ukrainian leaders expressing openness to discussing Ukrainian neutrality (as opposed to insisting on NATO membership), a major sticking point in talks with Russia. However, other Russian demands, particularly on the recognition of Russia’s annexation of Crimea and the sovereignty of Ukrainian separatists in the East, continue to be non-starters, while Ukrainian FM Kuleba has stated that his expectations of the talks “are low”.

- Participants removed some of the inflation-linked price premium for gold on Wednesday as major crude benchmarks took a tumble, with WTI and Brent closing ~$15 lower apiece on the day, while broad U.S. real yields moved away from their recent trough.

- Elsewhere, the U.S. has emphatically rejected Poland’s proposal to transfer Polish jet fighters to Ukraine, easing some worry re: increased western involvement in the war in Ukraine.

- From a technical perspective, bullion has broken below support at $1,981.2/oz (Mar 8 low), exposing the next support level at $1,929.9 (Mar 4 low). Conversely, resistance is situated at $2,070.4/oz (Mar 8 high).

OIL: Higher In Asia

WTI is +$1.10 and Brent is +$2.70 at writing, printing ~$109.8 and ~$113.8 respectively. Both benchmarks operate far below cycle highs registered earlier in the week as hope surrounding a diplomatic resolution in the Russia-Ukraine conflict has risen, helping to unwind some of the geopolitical risk premium re: the situation. On that matter, focus has turned to “high-level” talks between the Foreign Ministers of Ukraine and Russia in Turkey, due to happen later today.

- To recap Wednesday’s price action, WTI and Brent closed ~$15 lower on the day, declining to session lows after a tweet from the UAE’s ambassador to the U.S. suggested that the UAE would support crude output increases in OPEC+ to address ongoing tightness in global crude supplies. Both benchmarks have since risen off their worst levels, after the UAE’s energy minister reaffirmed the country’s commitment to the current pace of OPEC+ output increases (essentially walking back the ambassador’s earlier remarks).

- Elsewhere, U.S. weekly EIA inventory data on Wednesday again pointed to persistent tightness in oil supplies, with drawdowns observed in crude, gasoline, distillate, and Cushing hub inventories.

- Looking to technical levels, resistance for WTI and Brent is seen at their Mar 9 highs of $124.66 and $131.64 respectively. On the other hand, Wednesday’s price action has seen both benchmarks break below previously defined support, exposing the next support level at Mar 1 lows of $95.32 for WTI and $98.30 for Brent.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 10/03/2022 | 0700/0800 | * |  | NO | CPI Norway |

| 10/03/2022 | 1245/1345 | *** |  | EU | ECB Deposit Rate |

| 10/03/2022 | 1245/1345 | *** | | EU | ECB Main Refi Rate |

| 10/03/2022 | 1245/1345 | *** | | EU | ECB Marginal Lending Rate |

| 10/03/2022 | 1330/0830 | ** |  | US | Jobless Claims |

| 10/03/2022 | 1330/0830 | *** | | US | CPI |

| 10/03/2022 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 10/03/2022 | 1330/0830 | * |  | CA | Intl Investment Position |

| 10/03/2022 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 10/03/2022 | 1630/1130 | ** | | US | NY Fed Weekly Economic Index |

| 10/03/2022 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 10/03/2022 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 10/03/2022 | 1800/1300 | *** | | US | US Treasury Auction Result for 30 Year Bond |

| 10/03/2022 | 1900/1400 | ** | | US | Treasury Budget |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.