Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

The September NFIB small business survey showed the headline optimism index dipped to 90.8 from 91.3 prior, slightly missing expectations of 91.0. That was the weakest reading since May, and came as owners expecting better business conditions over the next 6 months fell 6 points to net negative 43%.

- The usual pain points for small firms remain inflation (23% of owners identifying this as their "single most important problem", unch from August), and labor quality (also 23%). 57% reported "few or no qualified applicants" for job openings, which was the highest level in a year, with "positions not able to fill right now" and net hiring plans at a 4-month high 43%.

- Against a tight labor market backdrop, output price pressures remain a potential concern for the broader economy, with a net 23% planning to raise compensation in the next 3 months (albeit down 3pp from Aug), and a net 29% (up 2pp) raising average selling prices, a 3 month high.

- While the inflation and labor market components have eased significantly from the most extreme readings of the post-pandemic period, they remain elevated. Inflation "single most important problem" peaked at 41% and was 30% a year ago vs 23% currently; "quality of labor" at 23% was steady from 22% a year ago but vs 29% highs, and "cost of labor" at 9% steady from a year ago). In other words, stabilizing at high levels, which is consistent with continued inflationary pressures in the pipeline.

- Looking at financing conditions: loan availability was net -8%, the tightest since March's bank crisis and the 2nd tightest of this cycle, while the % that saw borrowing needs satisfied hit a 10-month low and expectations for easier credit conditions deteriorates 4pp to a joint-cycle worst -10% as interest rates picked up.

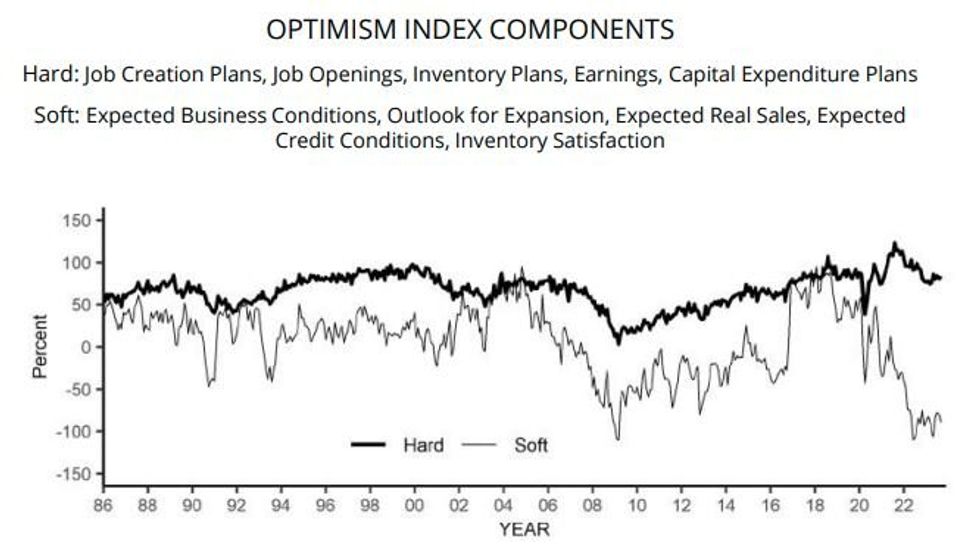

- While expectations remain weak and the overall optimism index more consistent with a recession than solid GDP growth, we again point out the divergence between the "hard" components of the index remaining solid vs the depressed "soft" components - see chart. The relative strength of the "hard" figures has been more closely aligned with actual economic activity in the past 2 years.

Source: NFIB

Source: NFIB

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok