Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

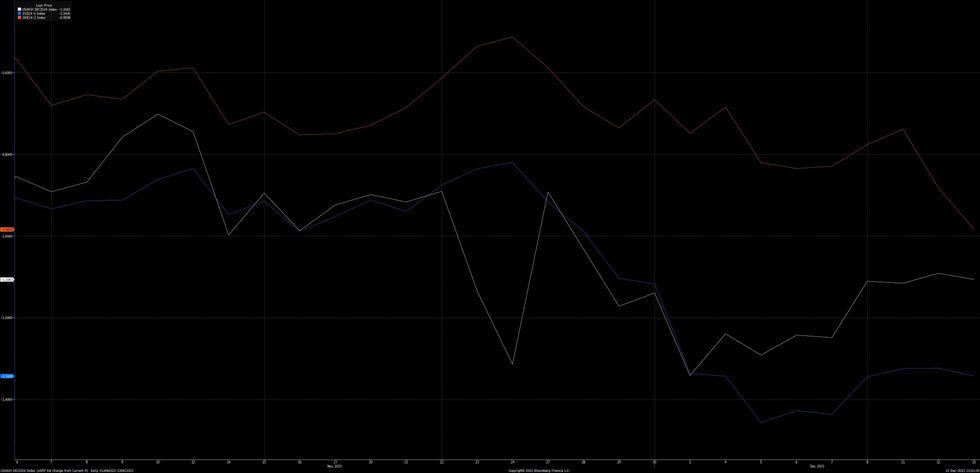

A quick overview of market pricing re: major central banks ahead of the final Fed, ECB and BoE meetings of ’23:

- Fed: ~111bp of cuts are currently priced through ’24, with the first 25bp cut fully discounted come the end of the May ’24 FOMC. A reminder that dovish comments from Fed Governor Waller and a run of economic data pushed Fed Funds futures to briefly price in ~135bp of ’24 cuts in recent times, before the latest NFP and CPI data prints helped take the edge of off that dovish swing. The Fed has retained the optionality for further hikes in recent post-meeting statements and we don’t expect this to change today.

- ECB: With the ECB ultimately calling time on the hiking cycle, barring any surprises, focus has moved to QT and rate cuts. A subsequent adjustment towards a more centrist stance on the part of some of the traditionally hawkish voices on the Governing Council, as well as data-driven expectations, briefly allowed ~150bp of cuts to show in ’24 pricing. Latest market pricing shows ~135bp of cuts through ’24, with the first 25bp cut more than fully discounted through the May ’24 meeting and greater than even odds of a 25bp cut priced for the March ’24 gathering.

- BoE: UK STIR pricing has seen a degree of ‘catching down’ to global peers in recent sessions, with the softer-than-consensus AWE data within yesterday’s labour market report, as well as today’s softer-than-expected economic activity and GDP data, driving matters. 98.5bp of cuts now show through ’24 on the whole, with the first 25bp cut more-than-fully discounted come the end of the June ’24 MPC, alongside greater than even odds of a 25bp cut come the end of the April '24 MPC. Perceptions surrounding inflation stickyness and wage dynamics are the widely cited reasons for BoE pricing not being as dovish as Fed & ECB peers.

- Our previews for the impending central bank decisions can be found below:

- Fed

- ECB

- BoE

Fig. 1: Market Pricing Of Fed, ECB & BoE Rate Cuts Through Dec '24 Meetings (%)

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok