Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

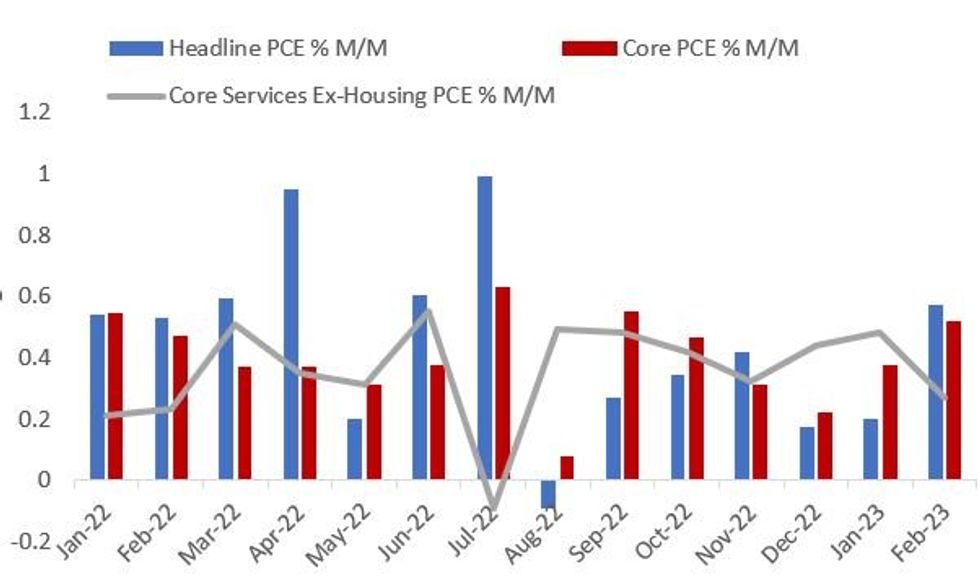

The February PCE price deflators came in on the soft side in February vs consensus:

- Unrounded headline PCE deflator: +0.263% M/M (prior +0.573%, expected +0.3%)

- Unrounded core PCE deflator: +0.300% M/M (to be even more specific, 0.2998% - prior +0.519%, expected +0.4%)

- Note also a downward revision to core PCE prices (Jan to 0.5% from 0.6% prior) as well as the slightly softer-than-expected Feb print of 0.3% (vs 0.4%).

- The Bloomberg-calculated PCE Core Services Ex-Housing - the Fed's favored metric - fell to +0.27% M/M in Feb from +0.48% prior. That's the weakest such reading since a contraction in July 2022 and the second-weakest since Feb 2022.

- Cumulatively, that's a decent miss. With the revisions taken into account the undershoot was on the order of the +0.2% downside read we'd noted in our PCE preview that would be required to move the needle (and indeed, US rates have rallied.)

- The softness in core-core services is notable for giving the Fed scope to pause on May 3, but the April 28 PEC reading will be more definitive in that regard.

Bloomberg estimate of core services ex-housing. Source: BEA, MNI

Bloomberg estimate of core services ex-housing. Source: BEA, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok