Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

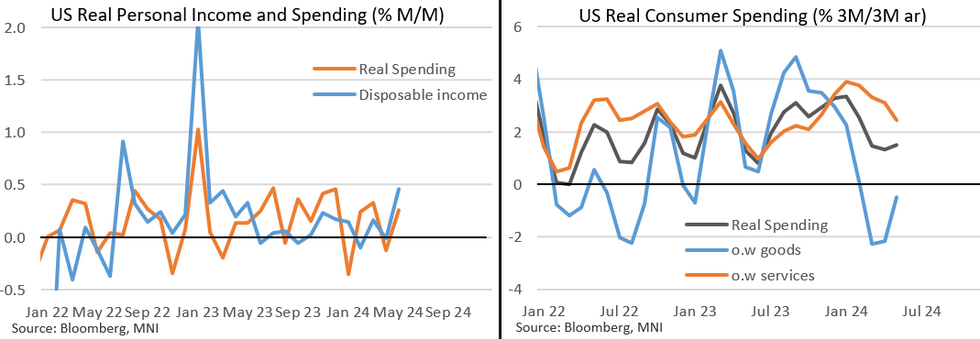

May's PCE report showed a pickup in disposable income and a slight uptick in overall spending in May, though subdued consumption (especially for services) and an unexpected jump in the household savings rate suggests some caution by consumers in mid-quarter.

- Real disposable income rose by the fastest in 16 months at +0.5%, following on from 3 cumulatively flat months. Nominal income growth came in at 0.5% M/M (0.48% unrounded), vs 0.3% prior - bringing the 3M/3M annualized rate of growth to 5.7%, down from 6.2% prior but still very elevated by historic standards. That in turn was driven by a bounceback in employee compensation to 0.6% M/M from 0.2% prior, with wages and salaries +0.7%, leaving disposable income growth at +0.45% M/M, up from 0.25% prior.

- Nominal spending ticked higher to 0.2% M/M (almost in line with the 0.3% consensus at 0.248%, but still a slight disappointment given April was revised down 0.1pp to 0.1%), Goods and services purchases each rose a similar amount (0.2% and 0.3% respectively), with overall real spending up 0.3% M/M (vs -0.1% prior).

- The real spending figure was in line with consensus expectations, and keeps the 3M/3M annualized rate at 1.5% after April's 11-month low 1.3%. That's equal to the Q1 real PCE figure of 1.5%. In other words, real spending in Q2 looks much more subdued than the 3+% rates at the turn of the year. On a Y/Y basis, real personal consumption expenditure was up 2.4% (goods +1.7%, services 2.8%).

- On a price-adjusted basis, goods consumption jumped to +0.6% from -0.1% prior, led by durables; real services consumption in contrast has been flatlining at 0.1-0.2% M/M the past 3 months, with a 3rd sequential slowdown in May to 0.10%.

- Of note, the household savings ratio unexpectedly rose to a 4-month high 3.9%, up from 3.7% prior (rev up from 3.6%). With the growth in disposable income comfortably exceeding that of spending, the overall picture is of slightly more cautious American households in mid-Q2.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok