Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

UK DATA

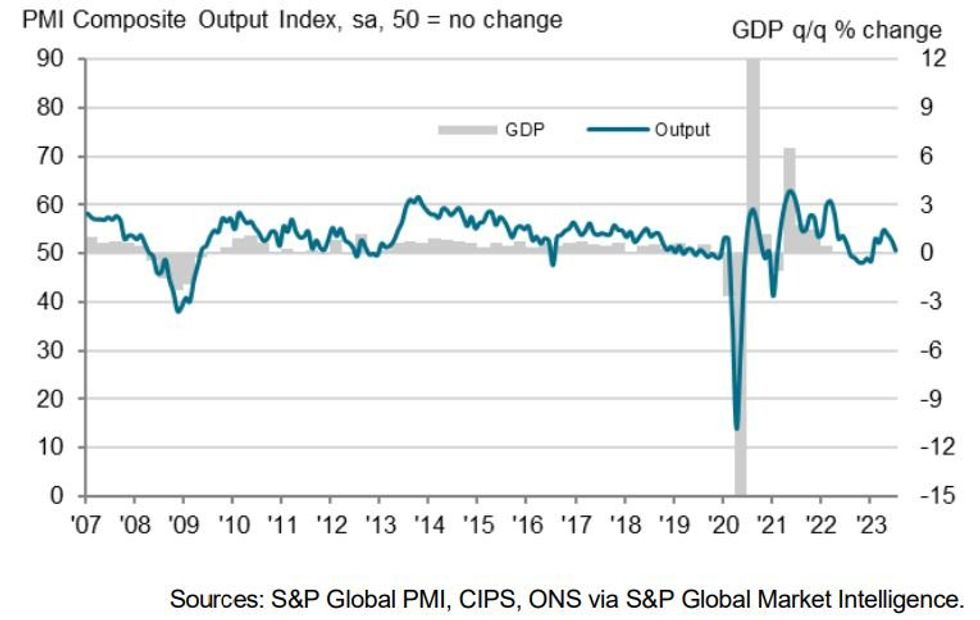

UK flash July PMI readings disappointed to the downside, with manufacturing at 45.0 (vs 46.0 expected, 46.5 prior), and services at 51.5 (vs 53.0 expected, 53.7 prior), dragging the Composite reading to 50.7 vs 52.8 prior.

- The Composite reading was the weakest reading in six months and as telegraphed by similar readings across Eurozone counterparts earlier in the morning, soft demand was evident, though on the bright side, price pressures are also easing.

- With supply chain issues fading, the S&P Global/CIPS report noted manufacturing suppliers' delivery times fell to a record low (index began in Jan 1992), helping manufacturing output charges ease for a 2nd consecutive month, with composite prices charged the slowest in nearly 2.5 years. Services inflation painted a slightly different picture, with average prices charged posting a "robust rise".

- New business failed to expand for the first month in 6, with "marginal" services growth offset by falling manufacturing sales amid "heightened economic uncertainty, inventory reduction, and the impact of rising borrowing costs on spending decisions."

- As with Germany and France earlier, new export orders also contributed to the weaker demand picture, falling at the fastest pace since Nov 2022.

- And expectations moderated to the weakest since Dec 2022, in part because of concerns over the "impact of higher borrowing costs on customer demand".

- That said, employment continued to expand (for the 4th month running), but eased slightly since June.

- Overall the report assesses that “forward-looking indicators, such as order book inflows, levels of work-in-hand and future business expectations, all point to growth weakening further in the months ahead, adding to a risk of GDP falling in the third quarter.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok