Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMANY

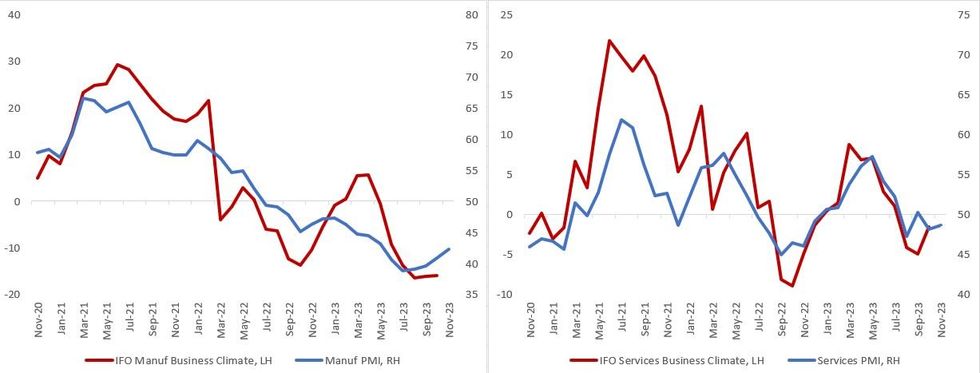

Today’s better-than-expected November Flash PMIs (manufacturing at 42.3 vs 41.2 consensus and 40.8 prior, services at 48.7 vs 48.5 consensus and 48.2 prior, composite 47.1 vs 46.3 consensus and 45.9 prior), while undoubtedly poor, provide further evidence that the contraction in German economic activity may no longer be deteriorating - merely shrinking at a moderately recessionary pace.

- In this context, Friday's IFO will be informative. The current median consensus estimate for the overall business climate reading is 87.5, vs 86.9 prior - with both expectations and current assessment improving. MNI had noted at the time that October's reading pointed to very weak growth, but the first monthly increase after 5 consecutive declines suggested a potential trough for the economy in Q3.

- The German manufacturing PMI has been consistently contractionary but bottomed out in July, compared with the manufacturing IFO business climate which rebounded to positive territory in summer but as of October is yet to recover higher.

- The service sector readings of both surveys have been much more closely aligned over the past year, though through the summer the PMI was slightly less contractionary than the IFO.

- Notably from a demand perspective, the German PMIs suggested that although new orders across the private sector "decreased solidly and for the seventh month in a row", "the rate of decline was the weakest since June" - another potential sign of a nascent bottoming of demand.

- To be sure, growth still looks recessionary for Q4 (real GDP consensus -0.1% Q/Q), and there are no signs of a significant pickup in activity in the near future. On that note, the Q3 Final GDP reading will be published first thing on Friday (no revision expected to -0.1% Q/Q flash), with further details on the composition of growth.

Source: IFO, PMI, MNI

Source: IFO, PMI, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok