Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CONSUMER CYCLICALS

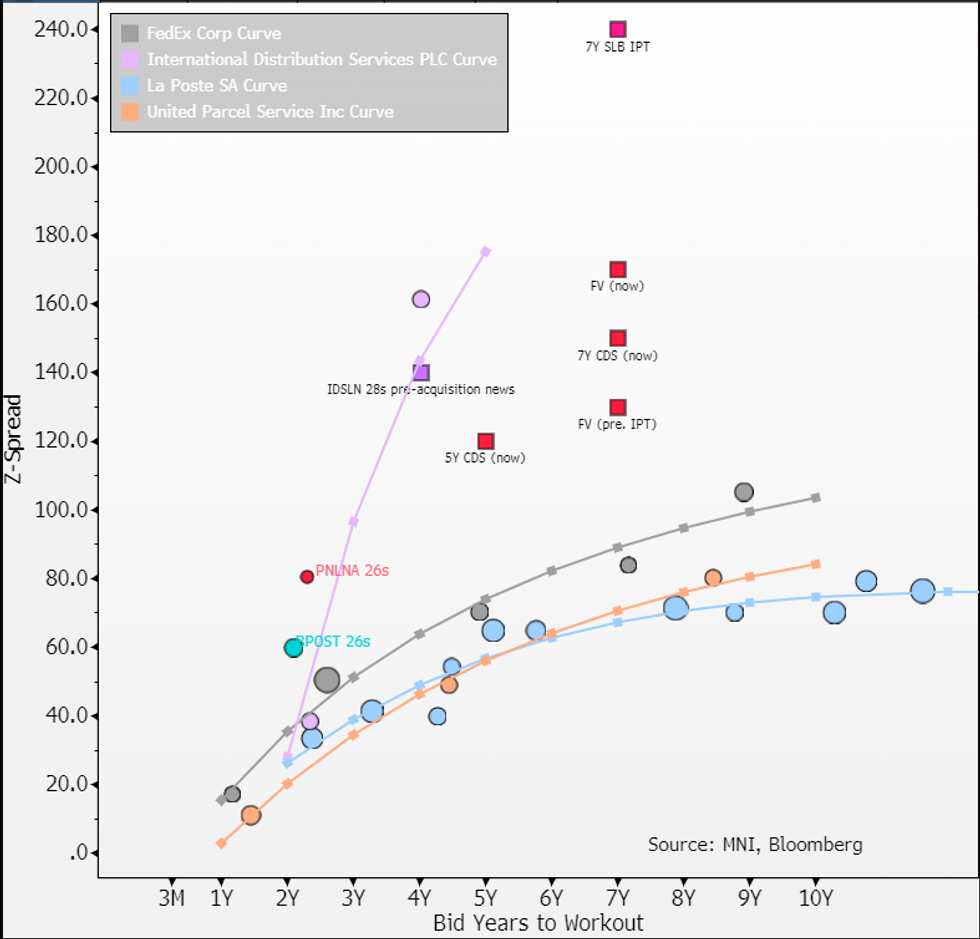

IPT: exp €300M 7Y SLB MS+240/250 vs. FV +170 (revised from +130) still -70 in. PX action since IPT; PNLNA 5Y CDS +8 at +120, PNLNA 26s +3, IDSLN28s -1 (Z+161)

We revise our approach to FV & effectively ignore ratings and higher rated comps and instead 1) apply Main basis of -20 to 7Y CDS at +150 & 2) curve it to dislocated (our view) IDSLN28s. MS+170 is the revised FV based on both. Cheap view stays on IDSLN28s for now, we may add this line depending on tightening into guidance/final.

- Looks like PostNL will get the IDS (NR/BBB Neg) treatment here; IDS28s priced a 5Y last year at MS+210 (mere 10bps in from IPT!) with 2x cover. The £250m 7Y came alongside it, pricing flat to IPT at UKT+290.

- The question for us is will we see a repeat of the IDSLN28s in secondary; it came in 70bps over 6months to pre. acquisition news levels. For investors that left a 385bp spread & 550bp yield return.

- IDSLN28s is a cheap view for us right now but we are struggling to be motivated to extend duration into PNL even at revised FV of +170. 7Y CDS mids are around +150, roll down into more liquid 5Y is 30bps. If basis comes lower than -50bps (i.e. +200) we think investors can eye this for value implied by basis & CDS roll-down.

- Roll & neg. basis is similar reasoning we had for a cheap view on new Elo 4Y earlier this year; its 14bps in (was -20 in last week).

Is IPT coming this wide justified?

- The treatment both curves are getting is harsh with little regard for any e-commerce driven parcel growth for PostNL (it is already majority of the revenue). It is the latter that is supporting ratings in IG as well.

- Reminder; BS is levered substantially on current FCF (though in target on net/EBITDA), high operating leverage means earnings vol for EBIT (which moves leverage) & dividend pay-outs are hefty - all credit negatives we've mentioned in FV.

- Still IPT is pointing to it coming wide of 'in structural decline' BBB & combustibles heavy tobacco names Imperial & Altria. They run much higher margins/FCF conversion though, much larger scale (global) and are lower levered.

- FV of +170 will now give 15bps over tobacco while shorter duration IDSLN28s gives +35 despite the larger scale.

Background on PostNL & Initial FV linked.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok