Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

JAPAN DATA

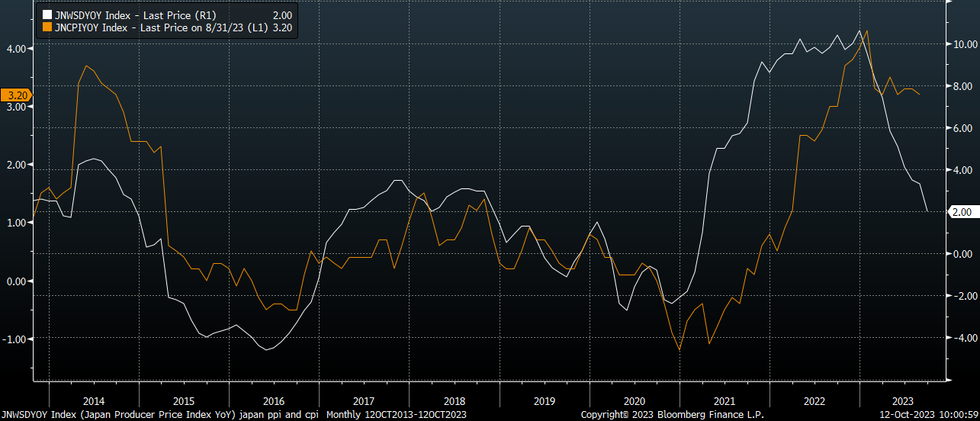

Japan data has printed for PPI, machine orders and bank lending. Most focus is likely to rest on the September PPI, which came in weaker than expected. In m/m terms we fell -0.3%, versus a +0.1% forecast and 0.3% prior. This left y/y momentum at 2.0%, versus 2.4% forecast and 3.3% prior.

- The main drag in m/m terms came from petroleum, coal (-4.1%), and utilities (-2.4%). Manufacturing was also down modestly (-0.3%). In y/y terms it is hard to find many sub-categories with stronger momentum compared to August.

- The chart below overlays the PPI y/y, versus headline CPI for Japan, also in y/y terms.

- Still, import prices rose 2.1% m/m, as petroleum, coal, gas, rose 4.5% for the month. Import prices remain in deep negative territory in y/y terms though.

- August core machine orders were down -0.5% m/m (against a 0.6% forecast rise). In y/y terms, we fell -7.7%, against a -6.7% forecast. We are up from recent cyclical lows but only modestly.

- Bank lending trends for September were similar to August, +2.9% y/y.

Fig 1: Japan PPI & CPI Y/Y

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok