Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

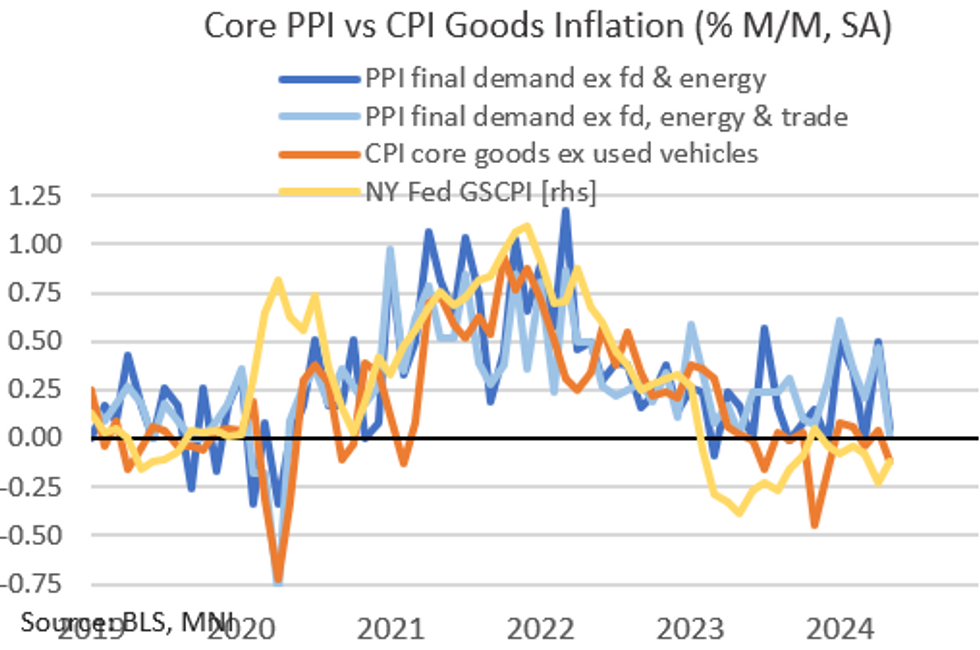

May's producer price data came in much softer than expected across most categories, with the headline PPI index (final demand) falling 0.25% M/M from +0.52% prior (unrevised), and vs +0.1% consensus.

- Ex-food and energy PPI grew just 0.05% M/M (0.50% prior), with the "core" PPI measure of ex-food/energy/trade services basically flat at +0.01% M/M (down from 0.47% prior, revised up 0.05pp), the lowest since April 2020.

- In the notable categories for core PCE, PPI components are unlikely to change the disinflationary story in the core CPI reading, and could even suggest some downward adjustments depending on analysts' assumptions. PPI airline passenger services contracted 4.3% (after -3.6% prior, -3.6% in May CPI), auto insurance grew 1.1% M/M (after 0.1% prior, -0.1% in May CPI).

- Categories without direct equivalents in CPI were, on net, set to soften PCE vs CPI: portfolio management/investment advice was down 1.8% M/M (after 4.4% prior), healthcare services ticked up 0.2% (after 0.1% prior, 0.3% in May CPI).

- Overall this is a very soft report in its own right, with the core PPI reading the lowest since the beginning of the pandemic, helping confirm the disinflationary impulses seen in the surprisingly low May CPI print and suggesting that soft core goods CPI can continue.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok