Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWEDEN

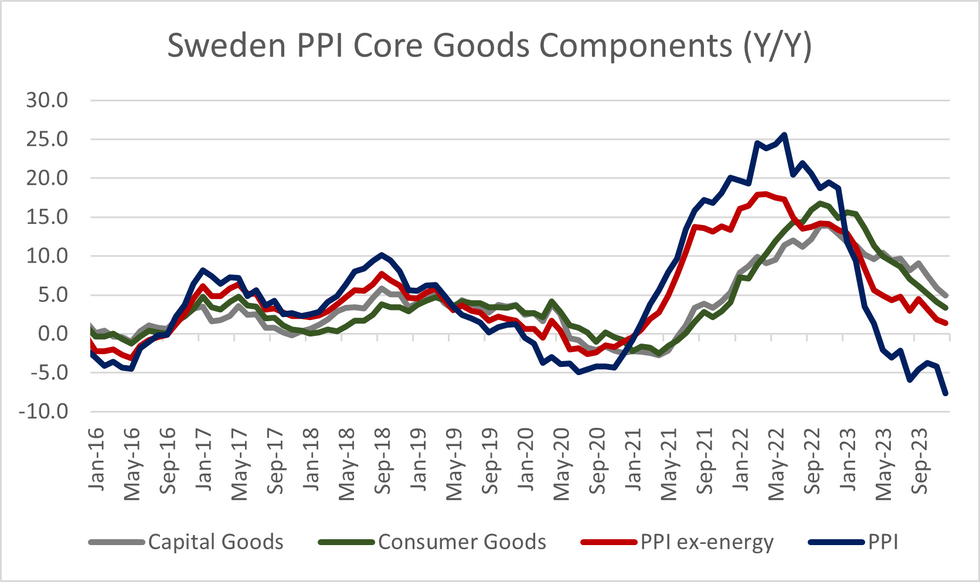

Swedish December PPI signalled that further disinflation in core goods CPI is likely in the near-term, with the PPI ex-energy index disinflating to +1.4% Y/Y (vs +1.9% prior), the third consecutive monthly fall.

- Both consumer and capital goods annual inflation rates fell, but remain positive at +3.4% Y/Y (vs +4.1% prior) and +5.0% Y/Y (vs +5.9% prior). Swedish goods (ex-energy) CPI was 4.0% Y/Y in December, down from a peak of 9.4% Y/Y in December '22.

- However, ongoing tensions in the Red Sea could pose an upside risk to future PPI prints. We will look to see if these concerns are noted in the January PMI round.

- All pipeline prices reported in today's data (export prices, import prices and domestic supply) were deflationary in annual and monthly terms.

- The pace of deflation in Swedish headline PPI accelerated for the second consecutive month in December, to -7.7% Y/Y (vs -4.2% prior). There was no consensus for this release. The NSA monthly price change was -1.6% M/M (vs +1.4% prior).

- Producer prices on energy related products fell -37.6% Y/Y in December (vs -26.0% prior), while lower prices for crude oil and refined petroleum products were reported on the month.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok