Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

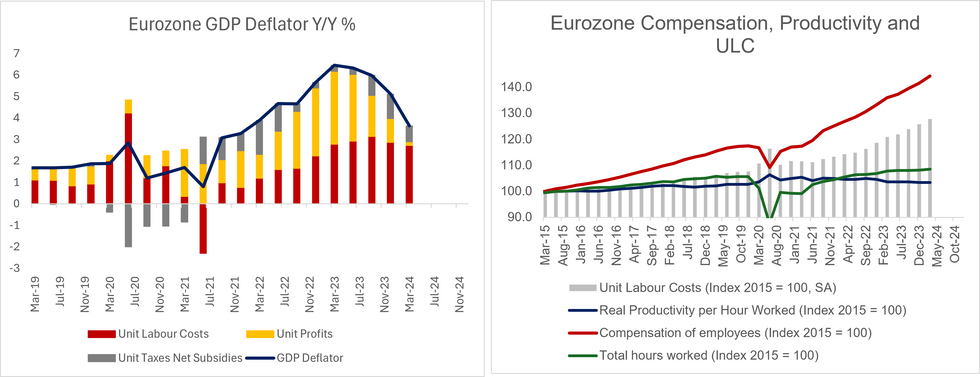

The Eurozone Q1 GDP deflator rose 3.63% Y/Y, moderating from 5.12% in Q4 2023 and the Q1 2023 high of 6.45%.

- In line with the ECB’s expectations and indications from the national-level data released over the past few weeks, a moderation in unit profits (-0.8% Q/Q, 0.4% Y/Y) drove the decline in deflator growth, while unit labour costs remained strong (1.6% Q/Q, 5.7% Y/Y).

- Overall, unit labour costs contributed 2.72pp to the 3.63% GDP deflator growth (vs 2.87pp prior), with unit profits contributing just 0.18pp (vs 1.10pp prior).

- Surprisingly, the 3.63% deflator growth is quite a bit below the 4.1% forecast in the ECB’s June macroeconomic projections (which, as a reminder, were compiled by Eurosystem staff and not ECB staff).

- This appears to be driven by unit taxes net of subsidies, which rose 7.0% Y/Y in Q1 (vs Eurosystem staff forecast of 7.5%). The forecast errors for unit labour costs and unit profits were 0.1pp and -0.2pp respectively.

- At 5.7% Y/Y, unit labour costs moderated a touch from the 6.0% seen in Q4. Real productivity per hour worked was -0.3% Y/Y in Q1 (vs -1.1% prior), while hours worked rose 0.6% Y/Y (vs 1.2% prior). Improvements in these two metrics will be required alongside a moderation in compensation to help unit labour costs soften further in the quarters ahead.

- While the strong compensation per employee data (5.05% Y/Y vs 4.92% prior) contributed to elevated unit labour costs, the growth largely reflects agreements that compensate employees for the loss of purchasing power seen over the past few years. Improving real wages should help underpin consumption in the quarters ahead, and contribute to a recovery in economic activity.

- The ECB’s June projections note that: “As growth in unit labour costs moderates, unit profit growth is expected to recover somewhat from 2025, helped by a robust economic recovery and strengthening productivity growth.”

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok