Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US OUTLOOK/OPINION

Tuesday's strong September retail sales control group reading (which is an input to GDP) of 0.6% M/M has spurred some upward revisions to Q3 GDP estimates, not least yesterday's Atlanta Fed GDPNow from 5.15% to 5.44%.

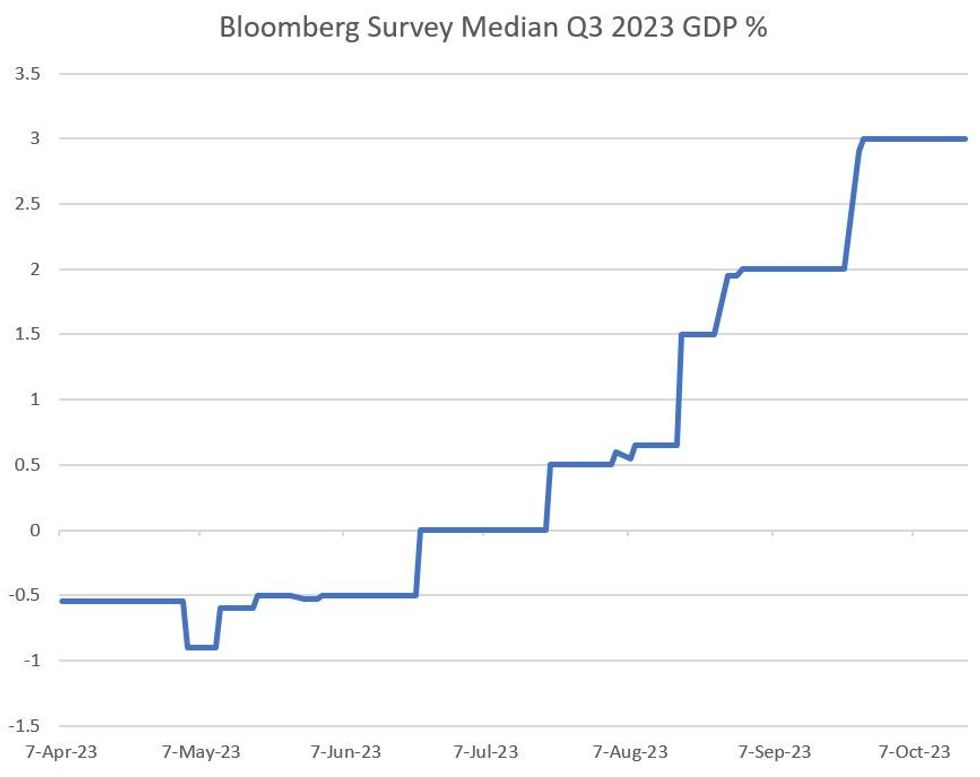

- Expectations are building that Q3 annualized GDP will come in well above the 3.0% BBG September survey median and 2.1% in Q2, and in any case well above potential growth - led by strong private consumption and residential investment, with government consumption and net exports also likely boosting the headline figure.

- Post-retail sales, Deutsche Bank upped its estimate from 4.1% to 5.2%; JPMorgan similarly, from 3.5% to 4.3%; Goldman Sachs from 3.7% to 4.0%. CIBC noted potential upside risks to their 3.9% projection but also noted that the strength in consumption momentum "implies a very strong start to GDP growth in 23Q$, where we had expected a slowdown just below 1%).

- We get the Q3 advance GDP reading on Oct 26 - less than a week from the FOMC decision on Nov 1 and in the midst of the pre-meeting blackout period for Fed speakers.

- A blowout number won't spur a November hike but will be hard for the FOMC to ignore in the deliberations and communications, with participants at the Sept meeting having seen Q3 growth running at a "solid" pace which may be understating the case.

- There hasn't been a 3%+ GDP reading since 2021 and as recently as June the Bloomberg median expectation was negative.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok