Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

MNI (Australia) A reminder that key China data prints are out tomorrow. Q3 GDP prints, along with September activity data.

- For GDP, base effects will impact the y/y print, as Q3 last year was inflated versus Q2 as Shanghai emerged from lockdown. The market expects 4.5% y/y growth, versus 6.3% in Q2 (forecast range 3.5%-5.2%). The q/q number should get more focus. The consensus is 0.9% (0.8% prior, with a forecast range 0.6%-1.5%).

- Sep IP is forecast at 4.4% y/y (prior 4.5%, forecast range is 3.2-4.9%).

- Sep retail sales is forecast at 4.9% y/y (prior 4.6%, forecast range is 4.3-6.5%)

- Both fixed asset investment (forecast 3.2% ytd y/y) and property investment (forecast -8.9% ytd y/y) are expected to print near August outcomes. We also get property sales. There is no consensus for this print, but the prior was -1.5% ytd y/y.

- The Sep jobless rate is expected to hold at 5.2%, unchanged from August levels.

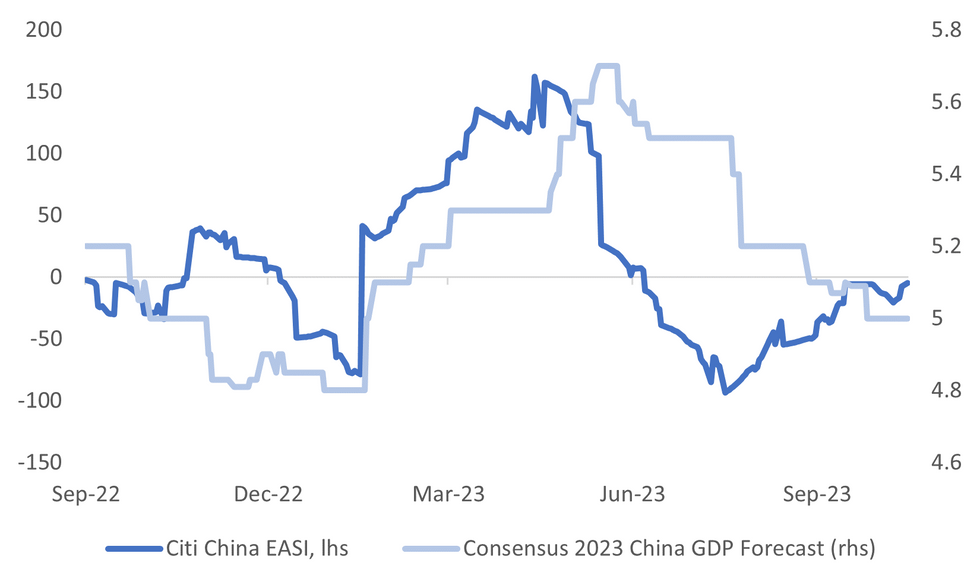

- Recent China data outcomes have, on balance, shown some modest upside momentum relative to expectations. The chart below overlays the Citi China EASI against consensus 2023 GDP growth expectations (BBG).

- Arguably we will need to see further positive surprises to see fresh upside momentum in growth expectations. Still, such upside surprises may need to be meaningful to put local assets (equities/FX) on a firmer footing.

- Markets have generally been left underwhelmed by efforts to boost the growth backdrop/outlook in recent months.

Fig 1: Citi China EASI Versus Consensus 2023 GDP Growth Expectations

Source: Citi/MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok