Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

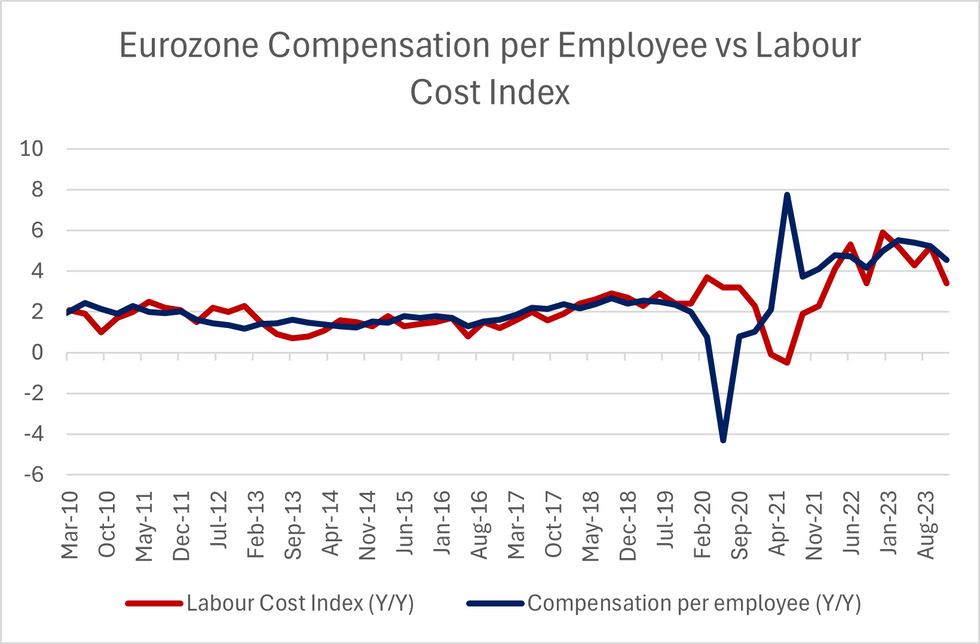

The Eurozone Labour Cost Index (LCI) moderated to 3.4% Y/Y in Q4 (vs a downwardly revised 5.2% prior). This release doesn’t add much more to what we already knew from the Q4 national accounts data, and the ECB are much more focused on forward-looking wage indications for Q1 '24, e.g. the Indeed wage tracker (which we wrote on yesterday) and their in-house negotiated wage trackers.

- The LCI is calculated as the ratio of total labour costs (wages and salaries plus non-wage costs) and hours worked.

- In contrast to the compensation per employee data from the national accounts, the LCI release contains industry level information, which would usually be of great interest to the ECB.

- For example, the 3.4% Y/Y print was dragged down by "public administration and defence" component, which was 1.8% Y/Y (vs 3.5% prior). This component was also the reason Italian labour costs fell 0.1% Y/Y (vs 2.0% prior), falling 3.9% Y/Y.

- Amongst services firms, labour costs were 4.1% Y/Y (vs 5.7% prior), while industry and construction costs rose 4.2% Y/Y (vs 5.8% prior).

- But being released with a 3.5-month lag, it's not a release markets are concerned about in the grand scheme of things (the Q1 '24 print is due on June 17, 2 weeks after the ECB's June 6 meeting).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok