Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

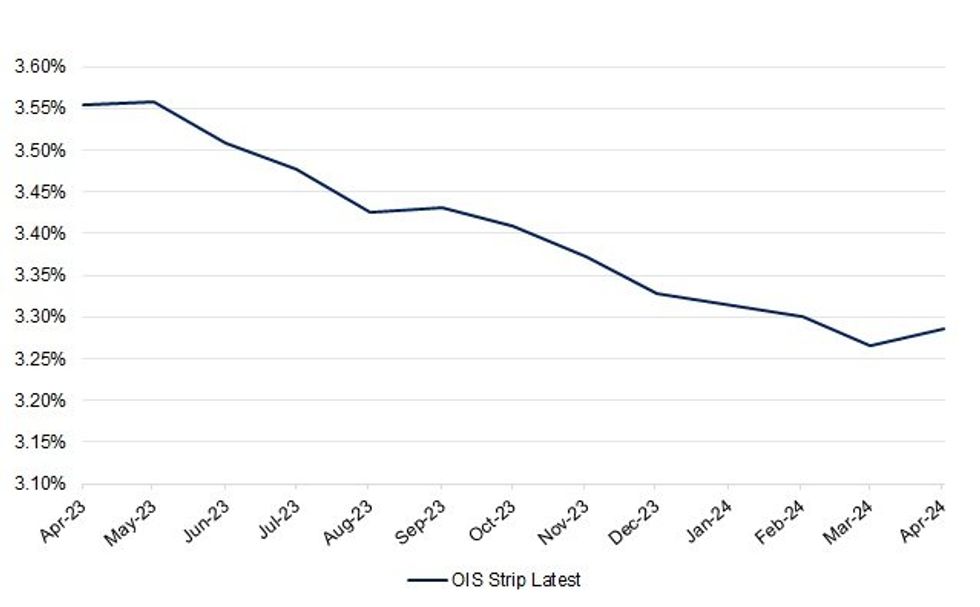

Fallout from the SVB collapse leaves the RBA-dated OIS strip calling time on the RBA’s rate hiking cycle, with 1-2bp of easing now priced for next month’s central bank gathering, while a 25bp cut is now essentially fully priced for the Bank’s December meeting (RBA-dated OIS covering meetings from August currently all price more than a 50% chance of such a step).

- A softer NAB business confidence reading (moving into negative territory) will do nothing to push back against this pricing, given that the RBA included it on the list of must-watch data re: monetary policy assessment. The survey collator noted that “while we expect inflation likely peaked in Q4, price growth remains elevated and the survey suggests that while global goods-side pressures have abated somewhat, there has been less evidence of easing in services-side pressures. NAB continues to expect a more material slowdown in demand, but this will likely come later in 2023 when the full effect of rate rises has passed through.”

- U.S. CPI data (due Tuesday, NY Time) will be key for the short-term outlook of market pricing re: global monetary policy settings.

Fig. 1: RBA-Dated OIS Strip

| OIS Strip Latest | |

| Apr-23 | 3.56% |

| May-23 | 3.56% |

| Jun-23 | 3.51% |

| Jul-23 | 3.48% |

| Aug-23 | 3.43% |

| Sep-23 | 3.43% |

| Oct-23 | 3.41% |

| Nov-23 | 3.37% |

| Dec-23 | 3.33% |

| Feb-24 | 3.30% |

| Mar-24 | 3.27% |

| Apr-24 | 3.29% |

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok