Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

INR

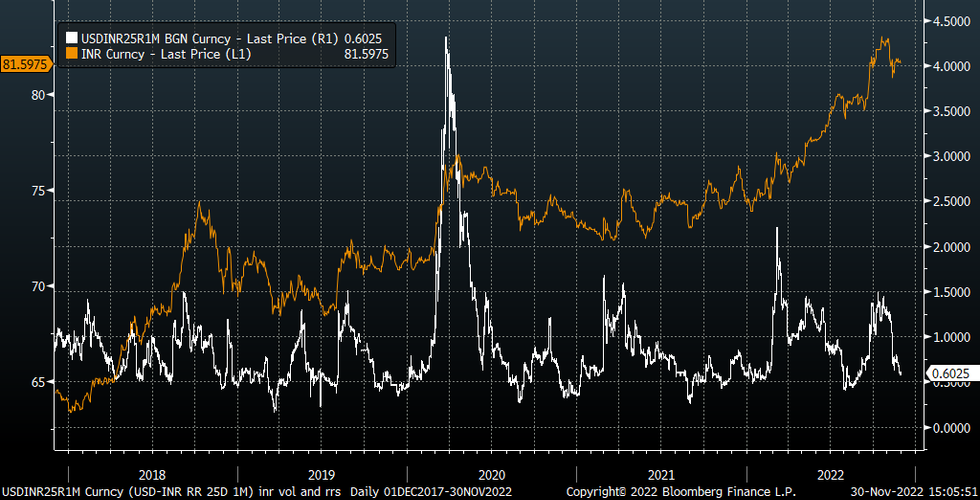

USD/INR has drifted lower since the open (last 81.60) but remains within ranges of the past few weeks (roughly 81.50 to 81.90). Equities are up modestly, tracking higher for the 7th straight session. The Nifty has hit fresh record highs, but this isn't imparting a positive bias on INR, relative to the rest of the region. The INR NEER remains close to recent lows near 68.50 (J.P. Morgan index).

- Not surprisingly, the 1 month implied vol is trending lower, but is seeing some support sub 6%.

- 1 month risk reversals have followed a similar path, but are arguably closer to cyclical lows, at least in a relative sense, see the chart below. Moves below 0.5000 in the risk reversal have not been sustained in recent years.

- Q3 GDP is due to print later, with the market looking growth at 6.2%, versus 13.5% in Q2. Part of the pullback reflects base effects, as last year's Q3 number was boosted as the economy emerged from lockdown conditions.

- This comes ahead of next week's RBI decision, where there is some sense the pace of tightening is likely to slow.

Fig 1: USD/INR Spot & The 1 month Risk Reversal

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok