Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

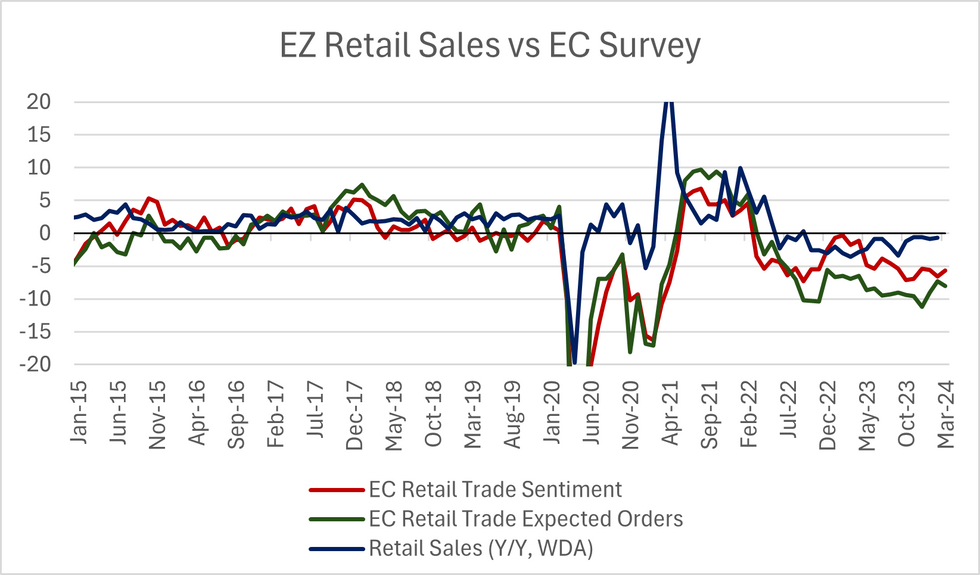

Eurozone February retail sales were -0.7% Y/Y WDA (vs -0.8% cons). January’s reading was revised 0.1pp higher to -0.9% Y/Y. On a monthly basis, sales were -0.5% M/M SA (vs -0.4% cons, 0.1pp downwardly revised 0.0% prior).

- All major subcomponents saw negative growth on an annual and monthly basis, though sales of non-food products rose to -0.1% Y/Y (vs -0.7% prior).

- At a country level, Germany saw the largest M/M fall in sales volumes (-1.9% M/M), while Belgium saw the largest Y/Y fall (-6.8% Y/Y).

- Retail sentiment in the EC’s business survey has been in contractionary territory for over 2-years now, though the March reading improved a touch to -5.7 (vs -6.6 prior).

- However, expected orders from the EC’s survey fell to -8.0 (vs -7.3 prior) in March, leaving little optimism for a pickup in sales volumes in the coming months.

- Analysts currently expect Eurozone Q1 household consumption at 0.7% Y/Y, above the 0.4% Y/Y forecast seen in late-2023.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok