Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

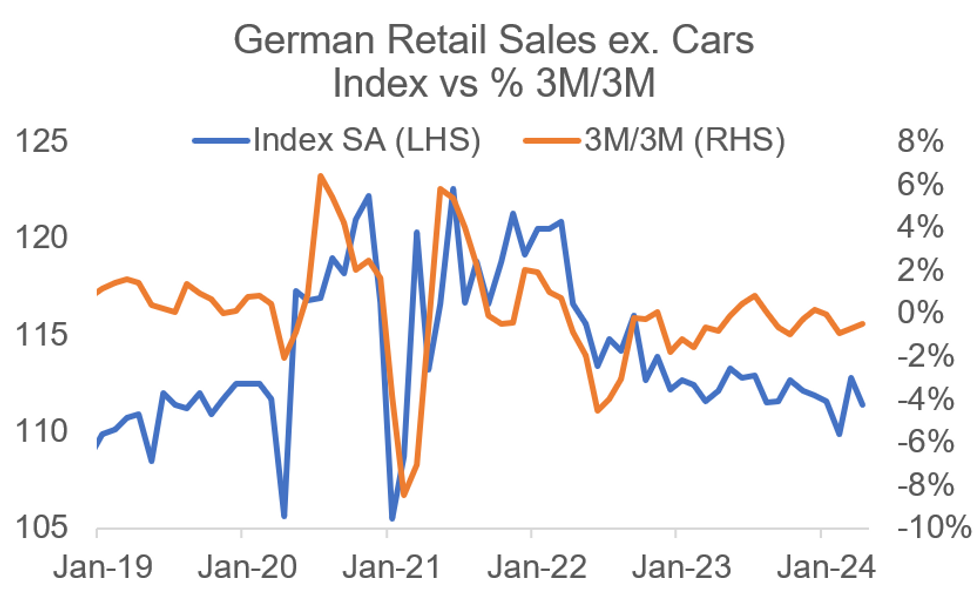

German retail sales (excl. cars) were weaker in April, declining by 1.2% M/M (real and seasonally- / calendar-adjusted; vs -0.3% cons; +2.6% prior, revised from +1.8%) and -0.6% Y/Y (calendar adjusted; vs +1.0% prior, revised from +0.3%).

- The upward revisions mean that the miss vs consensus was less severe than it seems on first sight.

- Food sales were -2.2% M/M, non-food sales -0.8%. April's data thus appears to be driven by a partial reversal of March's strong food turnover (+3.9% M/M), which was likely underpinned by the early Easter holiday this year.

- Looking into the details of the main non-food categories, internet and mail order sales inclined 2.9% M/M, while elsewhere, sales broadly declined vs March.

- Specifically, "sport equipment, publishing products, and toys" printed at -1.4% M/M (vs 2.8% prior), "furniture, Hi-Fi, and IT equipment" printed -2.0% M/M (vs 1.9% prior), and fuel sales came in at -3.6% M/M (vs +1.2% prior).

- The data suggests an overall rather weak start into Q2 for German consumer spending, which overall declined by 0.4% Q/Q (SA) in Q1 (vs +0.4% Q4) and contributed a negative 0.2pp to quarterly real GDP growth.

- Looking ahead, consumer spending is projected to pick up during the remainder of 2024, likely underpinnded by strong Q1 real wage gains, with MNI's collation of sellside analysts standing at +0.6% Y/Y for Q2 and +0.9% Y/Y for Q3/4. These estimates were mostly upwardly revised during the last month.

MNI, Destatis

MNI, Destatis

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok