Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

From our Fed preview, a few reminders of what to expect for the decision at 1400ET/1900UK below.

- Decision: Hold Federal Funds Rate range at 5.25-5.50%, leave QT policy unchanged. No dissenters expected.

- Statement: Potential for some tweaking of the opening paragraph to acknowledge slowing in nonfarm payrolls growth, but not market-moving. Inflation description unlikely to be changed ("Inflation remains elevated"). Would be a moderate surprise if they removed/altered the paragraph on banking sector risks but again, unlikely to be market-moving.

- If the Fed explains that it is holding rates steady but does not specify it is doing so "at this meeting" as it did in June when it was signaling a "skip" rather than the start of a prolonged hold, it could be considered a dovish development.

- Forward guidance ("In determining the extent of additional policy firming that may be appropriate to return inflation to 2%..." is expected to be unchanged - altering "the extent of" or "additional policy firming" would probably be done in a dovish direction.

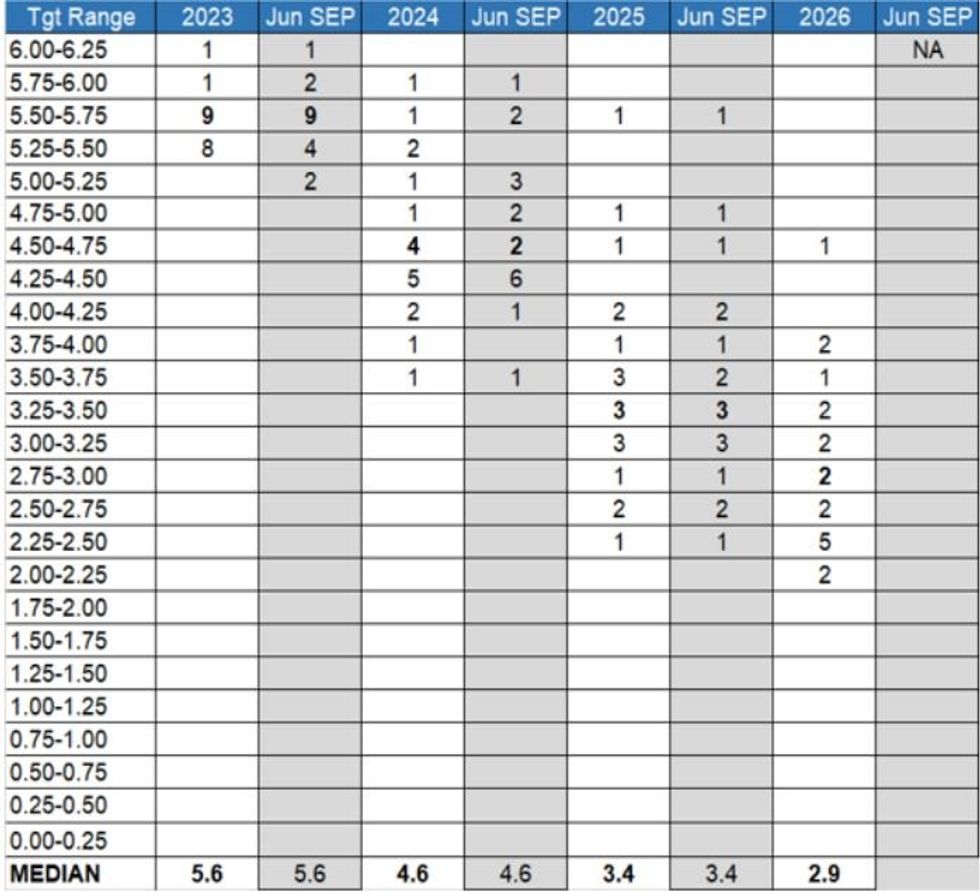

- Dot Plot: Most focus at the meeting will be on the Dot medians, which are broadly expected to be unchanged from June's projections with most focus on downside risks to 2023 (moving from 5.6% to 5.4% to signal the expected end of the hike cycle has arrived), with 2024's focus on upside rather than downside risks (some analysts see the median rising to 4.9% from 4.6%). Either way, the distributions of dots vs June's will be eyed for any shifts.

- 2025-26 dots are considered less important, though there is some interest in whether the longer-run dot will rise from 2.5% to signal FOMC participants see a higher neutral rate.

- The table below shows how MNI generally expects the September (white column) projections to look, with medians at the bottom vs the June SEP, and the number of participants in each column (we assume 19 dots vs 18 in June's)..

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok