Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

While the rate decision, Dot Plot, and Statement will be the most closely-scrutinized aspects of next week's FOMC release, a few areas of the updated economic projections also bear watching.

- The inflation forecasts will be watched in part because FOMC officials have been increasingly putting emphasis on the restrictiveness of policy as it relates to the spread of Fed Funds over PCE inflation, rather than just the level of rates outright.

- This approach paves the way for nominal rate cuts starting next year without reducing "real" restrictiveness. The "spread" between the Fed funds rate median in the Dot Plot (expectations for which we will cover in a note later this week) and the forecast inflation rate will be a key focus next week, we expect.

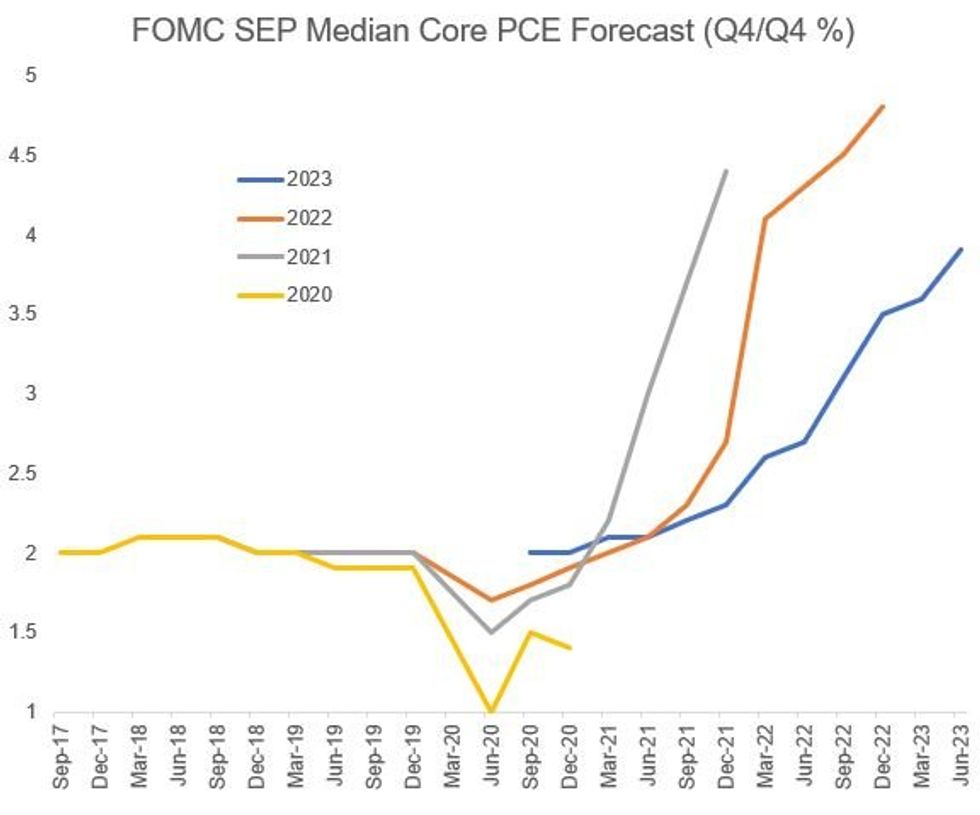

- June's projections saw headline PCE of 3.2% in 2023 and 2.5% in 2024, with core of 3.9% in 2023 and 2.6% in 2024 (figures are % chg Q4/Q4).

- MNI would not be surprised by a minimal change to 2023-24 headline, with softening incoming data offset by the consideration of rising energy prices.

- As for core, barring a major surprise in Wednesday's CPI report, the recent softening in Y/Y readings likely means June's projection is due a downward revision from 3.9% towards 3.5-3.6% (though again 2024's is unlikely to be much changed).

- This would mark the first time the SEP has lowered a core PCE forecast for the current year since 2020 (see chart). 2024 could be nudged lower as well.

- Note BBG analyst consensus for 2023 = 3.1% headline / 3.6% core; 2024 = 2.3% for headline / 2.4% core (i.e. below the FOMC's current projections).

Source: Federal Reserve, BBG, MNI

Source: Federal Reserve, BBG, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok