Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

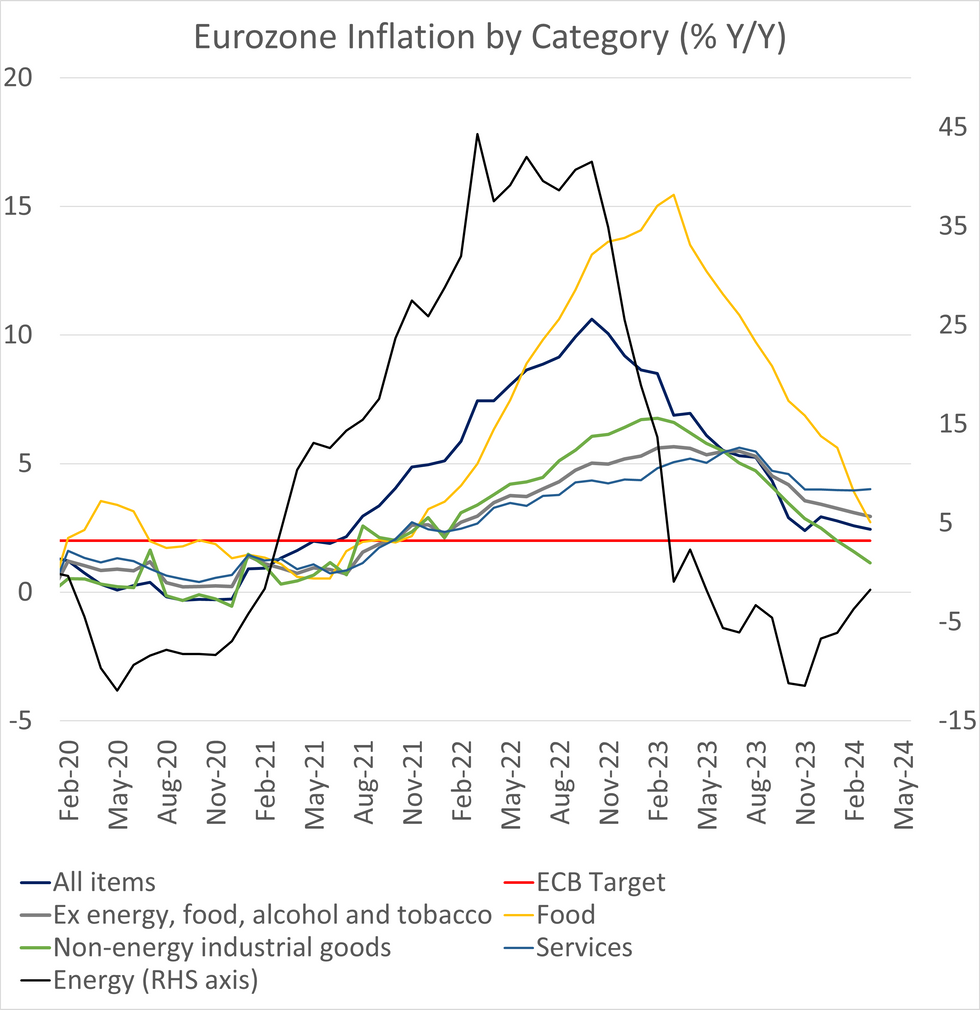

Eurozone March flash headline and core inflation both printed below consensus on a rounded basis, in line with MNI’s tracking based on the national data released over the past week.

- The release includes several strong NSA M/M readings across key categories. The ECB’s seasonally adjusted series (released later today) should provide a better indication of actual sequential pressures in March, though previously noted calendar effects may skew the interpretation somewhat.

- Headline HICP was 2.4% Y/Y (vs 2.5/2.6% cons, 2.6% prior) and 0.8% M/M (vs 0.6% prior). On an unrounded basis, headline was 2.44% Y/Y and 0.76% M/M.

- Core HICP was 2.9% Y/Y (vs 3.0% cons, 3.1% prior), below 3% Y/Y for the first time since March 2022. On an unrounded basis, core was 2.946% Y/Y and 1.10% M/M.

- As telegraphed by some of the major Eurozone countries’ data (e.g. Germany, Italy), services inflation remained sticky, printing at a rounded 4.0% Y/Y for the fifth consecutive month. A full analysis of the role that calendar effects related to the Easter weekend timing will have to wait for the final release on April 17.

- Non-energy industrial goods continued to moderate on an annual basis to 1.1% Y/Y, but saw a notably strong 1.9% M/M reading (although again, not seasonally adjusted).

- Food and energy inflation behaved as expected, with the former pulled lower by base effects (unprocessed food inflation was -0.4% Y/Y in March) and the latter seeing negative base effects continue to fade (energy HICP was -1.8% Y/Y vs -3.7% prior).

- At a country level, annual HICP fell in 9 countries, and was the same or higher in the remaining 11.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok