Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SINGAPORE

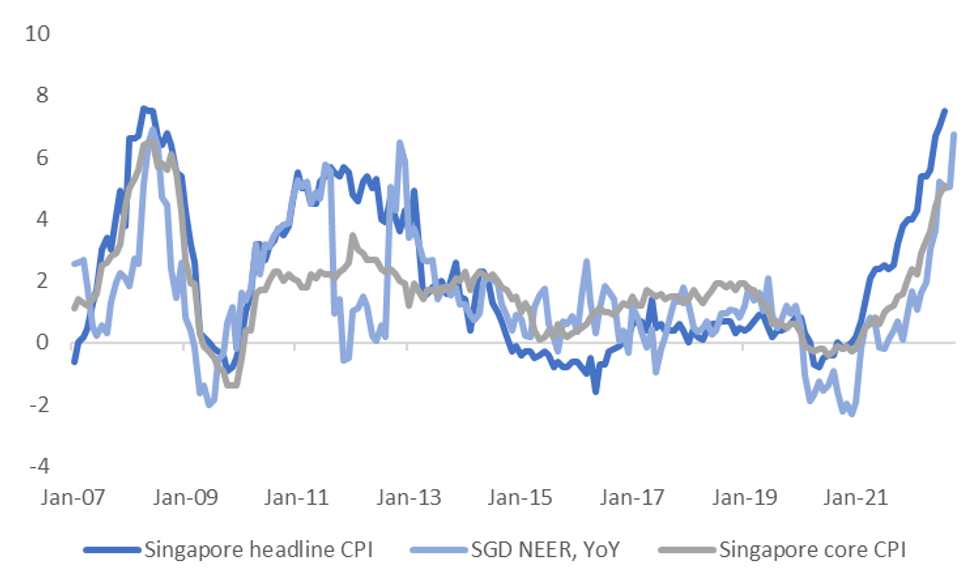

Singapore September inflation data prints late today (6am BST, 1pm local time). The market expects headline CPI to ease back to +0.4% m/m, from +0.9% m/m in August. This would leave the y/y print at 7.5%, unchanged from the previous month. Core inflation is expected to nudge up though, to 5.3% y/y, from 5.1% in August.

- Lower oil prices are expected to help transport costs, but food prices may move the other way. For core, re-opening and stronger domestic demand pressures is fuelling upside momentum.

- Y/Y inflation surprises have been skewed to upside this year. In the past 6 months the cumulative y/y surprise for headline inflation has been +1.45ppts, for core +0.8ppts.

- The recent MAS tightening has bought SGD NEER y/y momentum closer to headline inflation pressures, according to Goldman Sachs estimates, see the chart below. We update the official SNEER, from the MAS, with implied moves from the GS SGD NEER estimate for the past 2 weeks to generate the latest y/y print in the chart below.

Fig 1: SNEER Y/Y & Singapore Inflation Trends

Source: Goldman Sachs/ MAS/ MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok