Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

AUSTRALIA

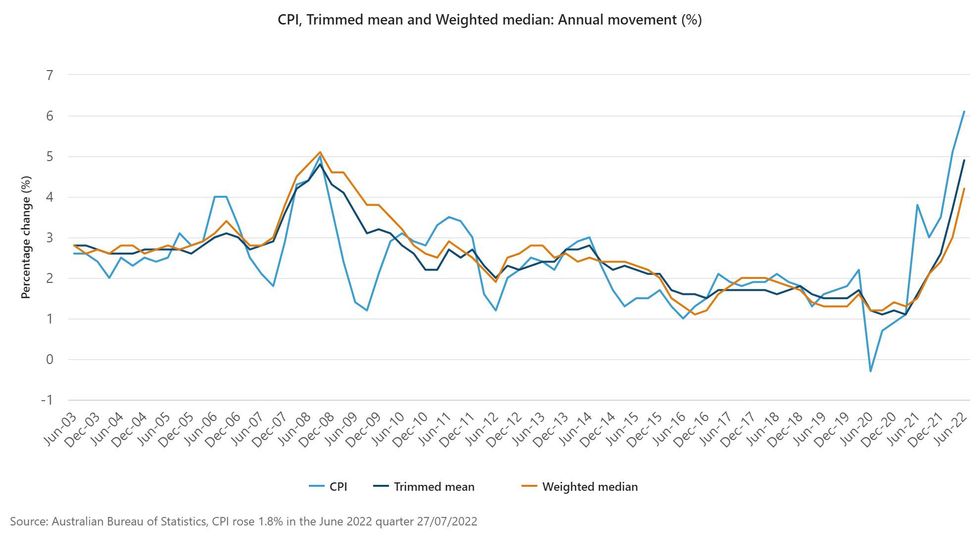

Q2 CPI data provided a miss in headline terms, printing +6.1% Y/Y vs. the BBG median of +6.3%, accelerating from the +5.1% seen in Q1. The ABS noted that “the most significant contributors to the rise in the June quarter CPI were new dwellings (+5.6%) and automotive fuel (+4.2%).”

- "Shortages of building supplies and labour, high freight costs and ongoing high levels of construction activity continued to contribute to price rises for newly built dwellings. Fewer grant payments made this quarter from the Federal Government's HomeBuilder program and similar state-based housing construction programs also contributed to the rise”

- Still, a firmer than expected trimmed mean print (the RBA’s preferred measure of underlying inflation in this data suite) was observed, +4.9% Y/Y vs. the BBG median of +4.7% & Q1 print of +3.7%, with the ABS noting that “annual trimmed mean inflation was the highest since the series commenced in 2003 and annual goods inflation was the highest since 1987, as the impacts of supply disruptions, rising shipping costs and other global and domestic inflationary factors flowed through the economy.”

- Markets have pared back the modest pricing of a supersized 75bp hike in immediate reaction to the release, with a 50bp move still full priced given the elevated levels of inflation and continued tightening of the Australian labour market, in addition to Governor Lowe’s guidance re: the need for further steady rate increases.

Fig. 1: Australian Headline, Trimmed Mean & Weighted Median CPI Y/Y (%)

Source: ABS

Source: ABS

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok