Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

UK DATA

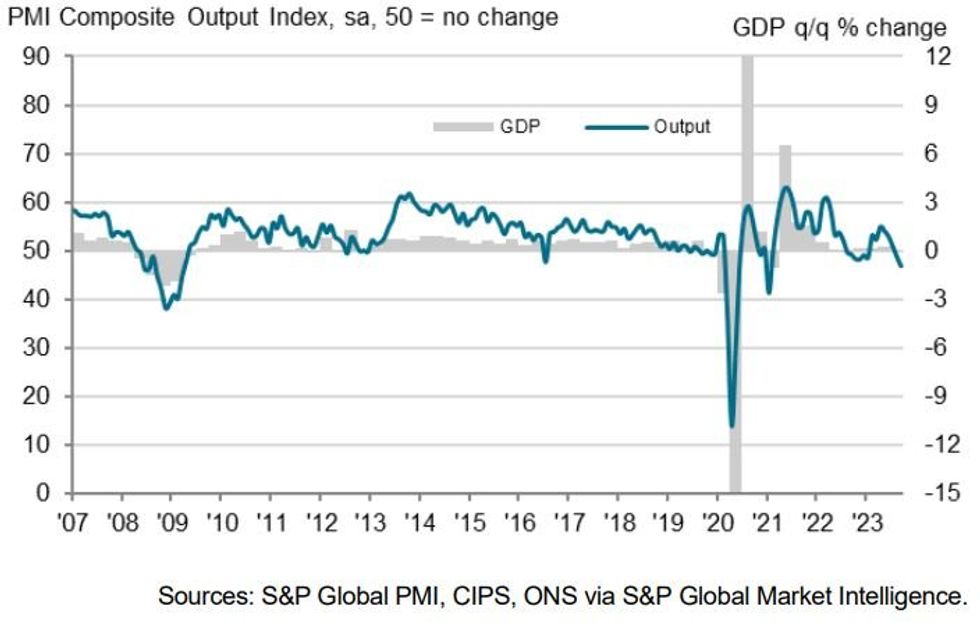

The UK September flash composite PMI was 46.8 (vs 48.6 prior; 48.7 expected) - a 32-month low. Services printed at 47.2 (vs 49.5 prior; 49.4 expected) - also a 32-month low - while manufacturing was 44.2 (vs 43.0 prior; 43.2 expected).

- The BoE MPC noted in its September meeting minutes that they had access to these flash figures prior to public release. The miss in the services print may have been a contributing factor to their decision to hold rates yesterday. Key notes from the release are:

- "Weaker demand due to cost-of-living pressures and higher borrowing costs were cited by survey respondents, alongside cutbacks to spending among clients in the real estate and construction sectors"

- "Manufacturing production continued to decrease more quickly than service sector output, but the gap narrowed considerably in September."

- "Service providers reported the steepest fall in new work since November 2022. Subdued business and consumer demand was attributed to elevated economic uncertainty, rising interest rates, and constraints on nonessential spending."

- "A number of firms continued to cite staff shortages and recruitment difficulties as factors that had limited their business capacity."

- "Solid declines in staffing levels were seen in both the manufacturing and service sectors, with the respective index for the latter posting in negative territory for the first time in 2023 to date."

- "September data pointed to the slowest rise in private sector business expenses since January 2021."

- "Average prices charged by private sector companies increased at a robust pace in September. This was driven by the service sector and mostly linked to higher operating costs, especially salary payments."

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok