Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SPAIN DATA

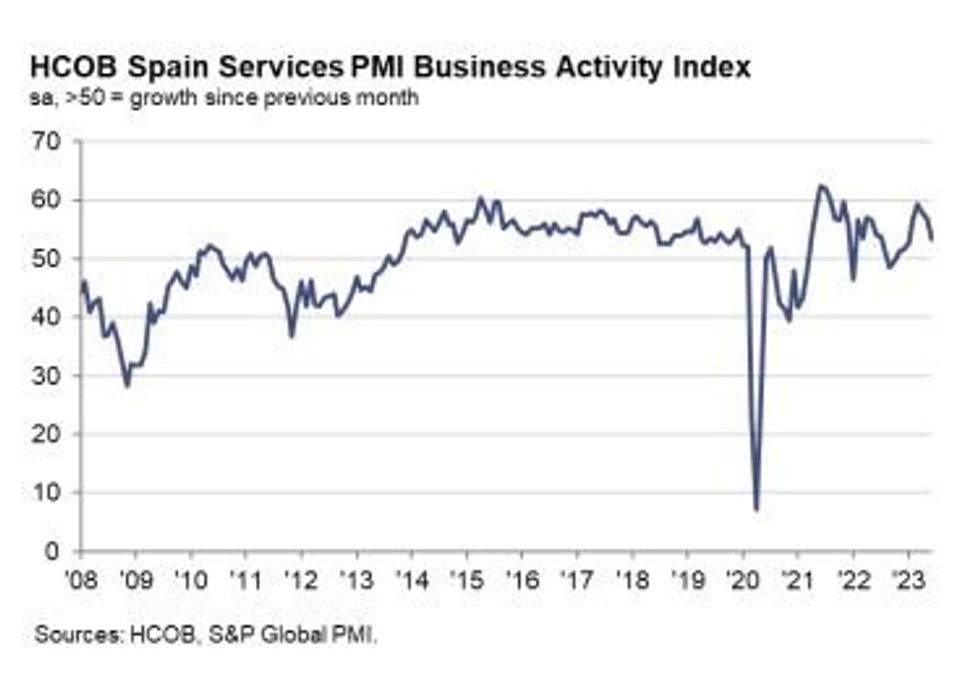

Spanish Services PMI disappointed in June with a drop to 53.4 from 56.7 prior (and vs 55.7 expected), pulling the Composite reading down to 52.6 from 55.2 (54.2 expected).

- This was the weakest Services print since January, with the HCOB/S&P Global report pointing to a "healthy demand environment" albeit slowing rates of expansion in the key categories of activity, new business, and employment.

- Inflation pressures continued to ease (input and output cost inflation) though remained at elevated levels, with "strong wage pressures" the "principal driver" of inflation. Firms "continued to partly transfer increasing costs on to their clients and subsequently signalled another solid increase in their charged prices" but "the rate of input cost inflation was the softest in just over two years and the increase in selling prices was the least pronounced since October 2021."

- Despite rising backlogs and capacity constraints, employment growth fell to a 4-month low (albeit amid 9 consecutive months of expansion).

- The report hints at potential one-off factors negatively impacting the reading ("in some cases ... local and general elections hampering activity"), and suggests that July's general elections may result in further uncertainty dragging on activity. Even so, Spanish services companies' 12 month outlook for activity continued to improve on demand optimism.

- Overall this report was a little soft but the economic outlook remains solid (2023 median GDP growth expectation is 2% vs 1% coming into the year).

Source: HCOB, S&P Global

Source: HCOB, S&P Global

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok