Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

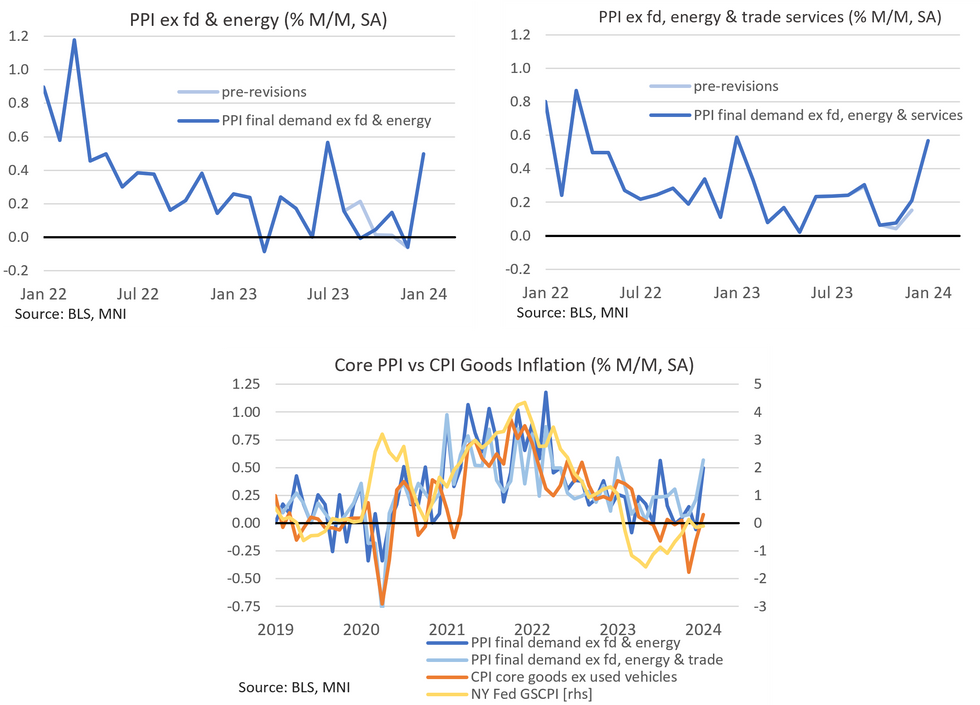

Headline final demand PPI printed at its highest SA monthly rate since August '23 in January, with the unrounded 0.33% M/M print easily overshooting the 0.1% M/M consensus (vs -0.15% prior after Wednesday's revisions).

- The core metrics overshot consensus by a larger margin. PPI ex-food and energy at 0.50% M/M (vs 0.1% cons, -0.06% prior) brings the 3mma annualised rate to 2.42% (vs 0.56% prior). Perhaps the one encouraging factor is the 6mma annualised rate, which still moderated a touch to 1.61% (vs 1.75% prior).

- Excluding food, energy and trade, both the 3mma and 6mma annualised rates rose in January. The former to 3.50% (vs 1.41% prior) and the latter to 2.99% (vs 2.30% prior).

- The most scrutinized areas though will be those that feed into the Fed's preferred measure of inflation: PCE.

- At a first glance, airfares and vehicle insurance both appear soft relative to Tuesday's CPI counterparts, while medical services seem similarly high.

- Recall that sell-side analyst expectations for core PCE ranged from 0.24-0.34% M/M post-CPI Tuesday. We will provide an update on changes to analyst's core PCE forecasts following today's PPI data in due course.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok