Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

JPY

JPY remains the weakest link in the G10 FX space. We have pulled back from overnight highs at 145.00 but dips sub 144.00 remain supported (last at 144.20). The focus remains on upside targets in the pair, as the sell-side consensus is that intervention risks are still fairly low at this stage, as the currency remains in line with fundamentals.

- Upside projections in USD/JPY remain firm. 145.28 and 146.03 are Fibonacci projections, while support is back down at 142.71, early lows from yesterday.

- On a short term basis, USD/JPY looks a little high relative to US yields, particularly the 10yr, but we would likely need to see a much larger divergence before the Japan authorities decided the yen was moving out of line with fundamentals.

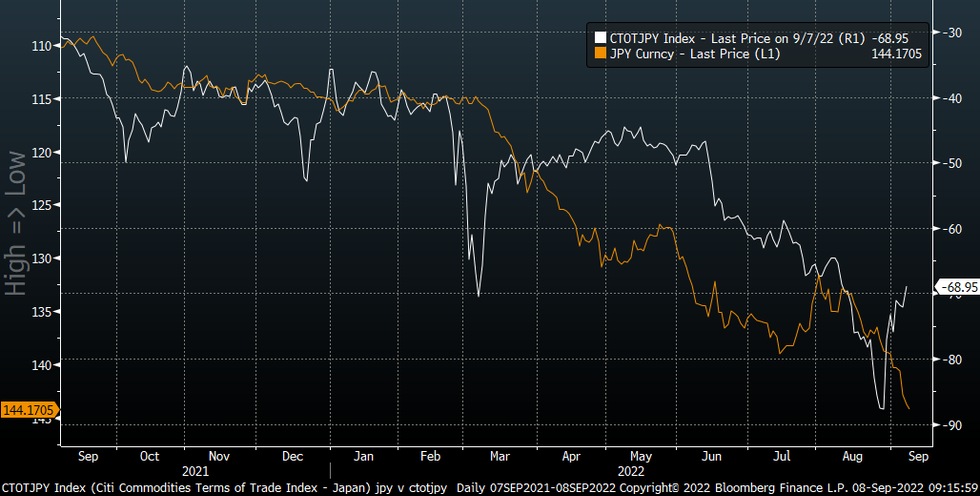

- The same can be said for JPY and the Citi terms of trade (ToT) proxy, see the chart below. The ToT measure improved further overnight, albeit from low levels, as energy commodity prices fell.

- Again, though we probably need to see a larger wedge emerge before the authorities would look to act. Also, the correlation between this ToT measure and JPY is not as strong as compared with yield differentials.

- Domestically, the data calendar is busy today. Q2 GDP revisions are on tap soon, with the market expecting some upside, due to better business investment. Also out is July BoP data, with the trade deficit expected to widen.

- Japan investor flows are also out, which will be in focus given on-going JPY moves, then later the Eco Watchers survey prints.

Fig 1: Citi Japan Terms Of Trade & USD/JPY

Source: Citi/MNI - Market News/Bloomberg

Source: Citi/MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok