Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

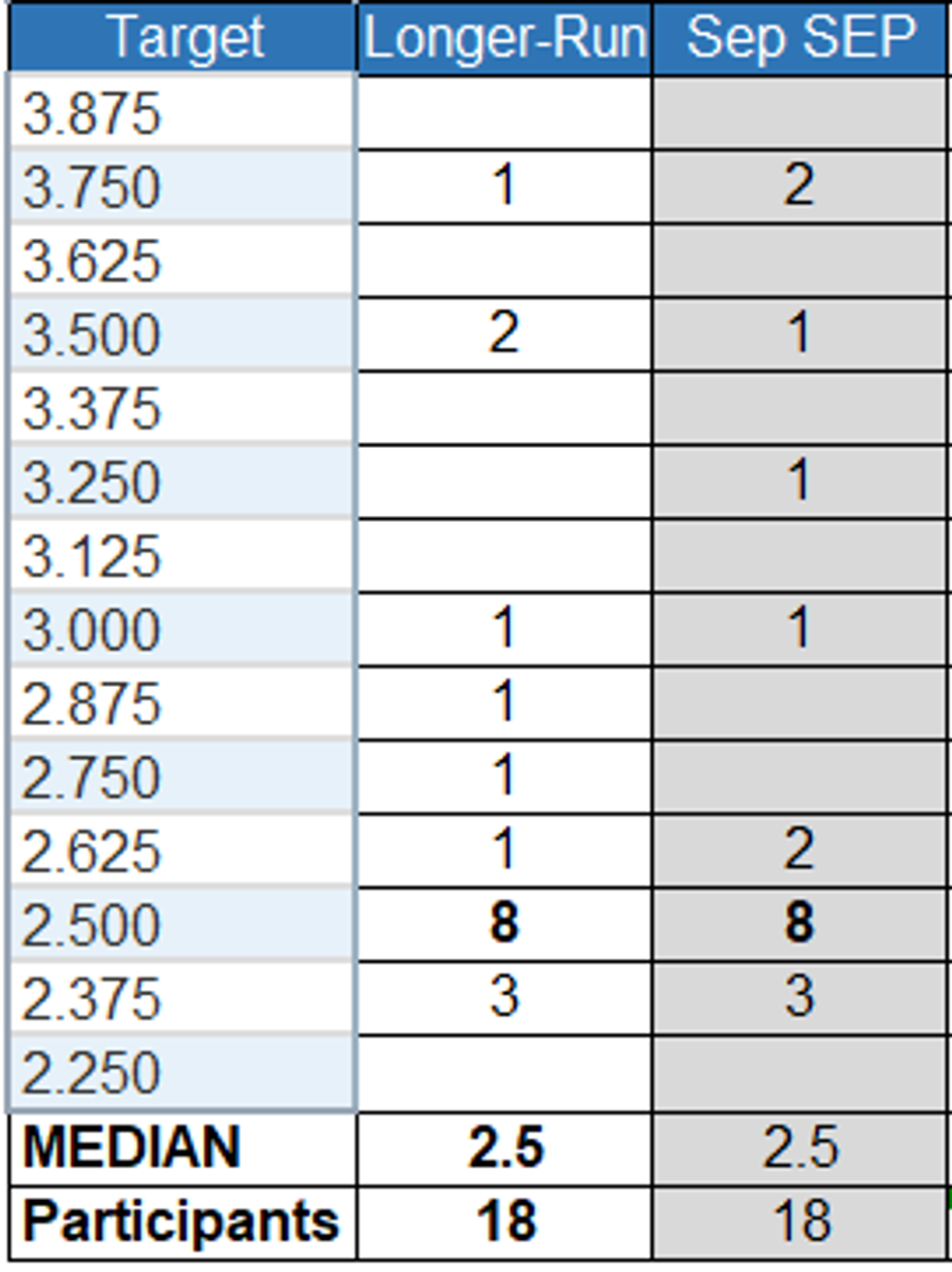

An overlooked outcome of December's FOMC materials is that the longer-run Fed funds rate dot distribution fell in versus September. From the perspective of the “central tendency” of the forecasts listed in the SEP table, this fell to 2.5-3.0% from 2.5-3.3%. This represents a surprisingly dovish outcome, particularly given that multiple analysts thought there was at least a good chance that the median dot would rise at this meeting.

- The highest longer-run dot in December’s projections was 3.75%; with 2 at 3.50%; 8 at 2.50% formed the median, with 3 at 2.375% below that. The remaining 6 dots were in the middle (2.6% to 3.0%).

- In September, there were 2 dots at 3.75%, so somebody's dropped lower (probably to 3.50% which only had 1 entry previously); the 3.25% dot has migrated lower as well, potentially to 2.875% or 2.75%. The bottom 11 dots were unchanged (2.375% and 2.50%) but one has migrated up from 2.625%, perhaps to 2.75% which previously was blank.

- It's hard to interpret what this means for any individual participant, but as a Committee, it looks like concerns over the longer-run neutral rate being much higher have dissipated somewhat as inflation data has softened since the September meeting.

Source: MNI, Federal Reserve

Source: MNI, Federal Reserve

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok