Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

Banking system reserves have fluctuated heavily over the past two months, but between ongoing QT and takeup of the Reverse Repo facility, sit about $1T below the Dec 2021 peak.

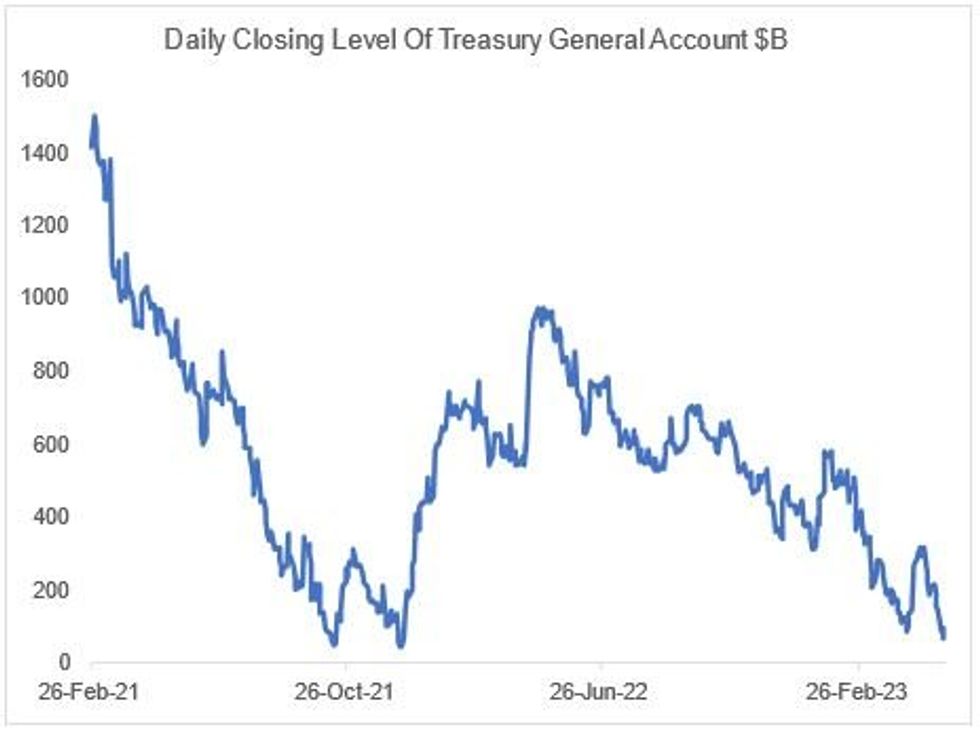

- One factor buoying reserves in recent weeks is the ongoing debt ceiling impasse, which has seen the Treasury’s General Account (TGA) at the Fed depleted to $68.3B as of Wednesday’s close, the lowest amount of the year and vs $316B at the end of May. All else equal, a lower TGA balance means more bank reserves, and vice versa.

- While the TGA will fluctuate in the weeks ahead, falling cash levels put focus on the Treasury’s warning that the “x-date” could arrive as soon as June 1.

- That said, an informal MNI client poll run earlier this week saw no respondents expect an outright default, with an 80/20 split between those expecting a short-term stop gap versus a long-term debt ceiling increase. And there's the potential for a near-term deal between Republicans and Democrats on raising the debt limit.

- If there is a resolution by early June, and the Treasury can resume borrowing, it’s expected to quickly replenish its cash pile by issuing sizeable amounts of T-Bills – with an end-of-June cash balance assumption of $550B (per the latest quarterly Refunding update), that could be on the order of a half-trillion quickly. Some analysts see the bill issuance running up to $1T in the coming quarters.

- Unless there is a sudden drop in takeup of RRP– which looks unlikely – reserves could drain out of the system quickly as the Treasury rebuilds its cash pile, putting renewed pressure on system liquidity.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok