Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

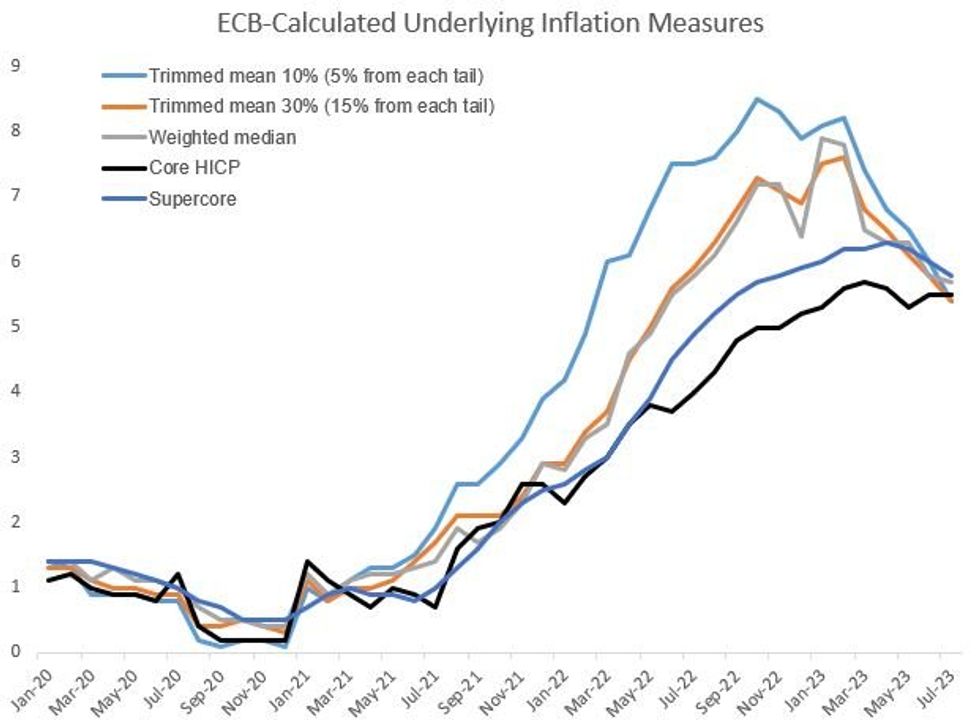

While today's release of final July Eurozone CPI confirmed a stubbornly strong Y/Y core HICP figure (5.5% Y/Y for a 2nd consecutive month, albeit partly on base effects and other statistical factors), underlying measures that are now available look relatively more disinflationary.

- A research bulletin published by ECB staff shortly after the July flash data pointed to multiple measures of inflation momentum waning, particularly in services (a point MNI made in our July Eurozone Inflation Insight).

- Their preferred metric overall, Persistent and Common Component of Inflation (PCCI, a model-based approach), corroborated this through June. July's PCCI should be published soon, but for now, we have the ECB's Supercore measure, which posted the lowest level (5.8%) in July since November 2022.

- Other measures released today, including trimmed means (which exclude extreme movers within the inflation basket), paint a similar picture.

- Trimmed mean at 10% dropped from 6.0% Y/Y to 5.4%, the lowest since Feb 2022, and to 30% it fell from 5.8% to 5.4%, lowest since May 2022. It's the first time those measures have printed below Core HICP Y/Y since February 2021.

- The weighted median measure at 5.8% Y/Y remains above core, and is coming down more slowly than the trimmed means, but is at the lowest level since November 2022.

- Pending the PCCI data, we see the non-core underlying data as cautiously encouraging for the ECB going into the September decision - while there is a long way to go, the granular July data offer another suggestion that inflation momentum is waning.

Source: ECB, MNI

Source: ECB, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok