Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Focus today on US Job Openings (for Dec) at 3pm Lon./10am ET; the consensus 8750k would leave openings to unemployed ratio at 1.4* - unchanged from Nov.* As headlines suggested $IG yest. surpassed the historic Jan 2017 to see $188b in issuance (MTD). Only one issuer is expected today ahead of macro calendar that stays busy for the remainder of the week. Issuance in Jan has had little impact on spreads & yesterday's $19.5b showed little signs of exhaustion with strong books and 3bps in NIC's.

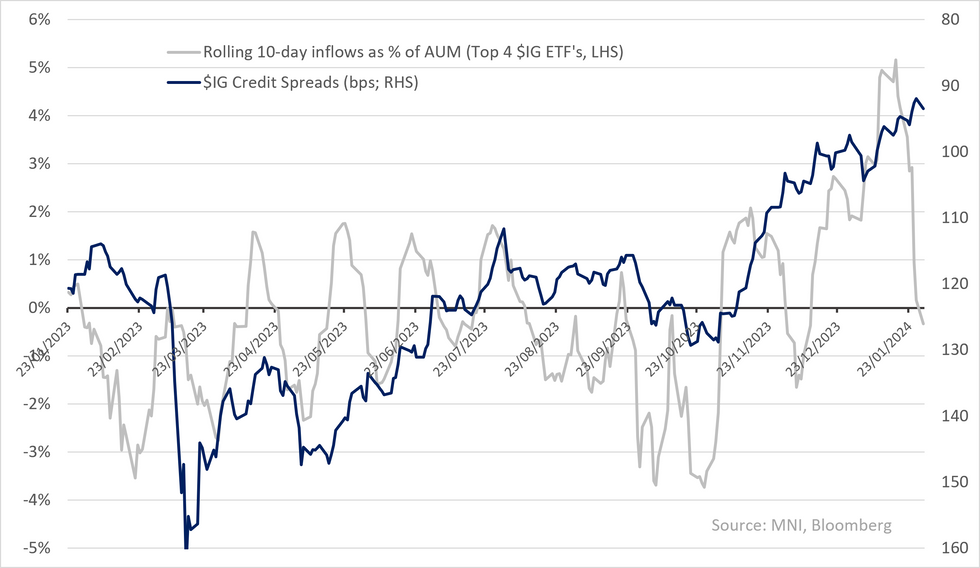

ETF flows have moderated now (below) but as analysts have flagged high level of s in cash/money market funds do point to potential support for inflows to return. Secondary did move wider yesterday; $IG/HY cash +1.5/+2.4, clear bear steepening (long-end +2.3bps) - books in primary yest. showed some signs of skew to the long-end though not as noticeable as sessions late last year.

CDX Opened +0.5/+4 wider & its dragged iTraxx towards unch now. S&P futures moving lower (-0.1%). Euro equities were flat this morning - no clear mover among the sectors either. Earnings focus is after the close on tech names (Microsoft, Alphabet, AMD) though we do have $IG & €IG issuers UPS, Pfizer & General Motors up this morning.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.