Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CNH

CNH is on track to record its firstly weekly gain vs. the USD in 7 weeks. However, this is all due to broader USD weakness, with domestic challenges/policy divergence still underscoring the headwinds for the currency.

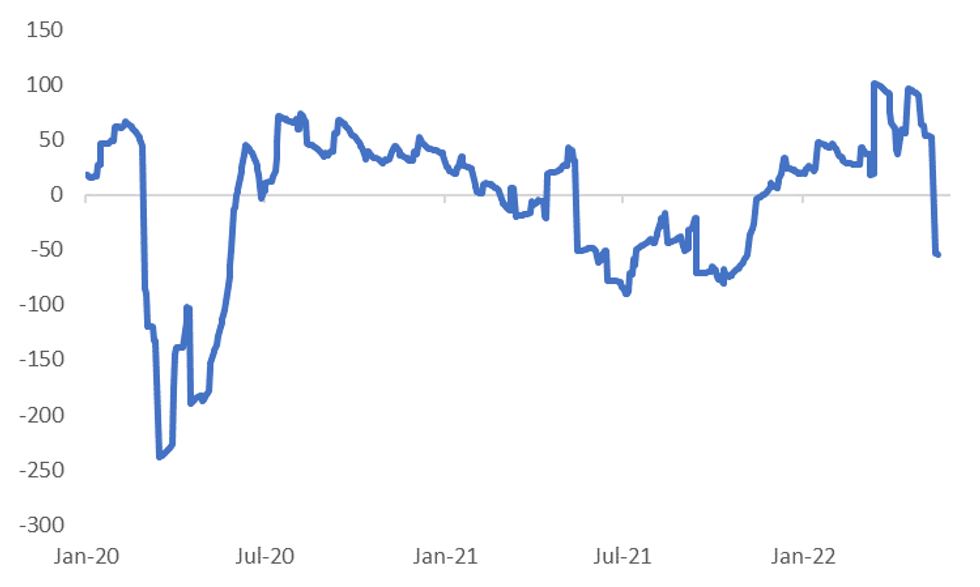

- This week's much weaker than expected China data has seen the Citi economic surprise index plunge, see the first chart below.

- A number of sell-side economists have cut their full year Chinese growth forecasts as a result. Standard Chartered, Citi and Goldman Sachs pushed their projections down to the low 4% region for '22 GDP growth. Previous estimates were 4.5-5.0%.

- While the covid situation appears to be gradually improving on the ground in China, there is scope for setbacks and the zero-covid stance suggests a rapid return to normal activity levels is unlikely.

Fig 1: Citi Economic Surprise Index Falls Sharply, Prompting Growth Downgrades

Source: Citi, MNI - Market News/Bloomberg

Source: Citi, MNI - Market News/Bloomberg

- A weaker growth backdrop should keep the policy bias still centered on easier settings. Today's 15bp reduction in the 5-yr LPR is testament to this.

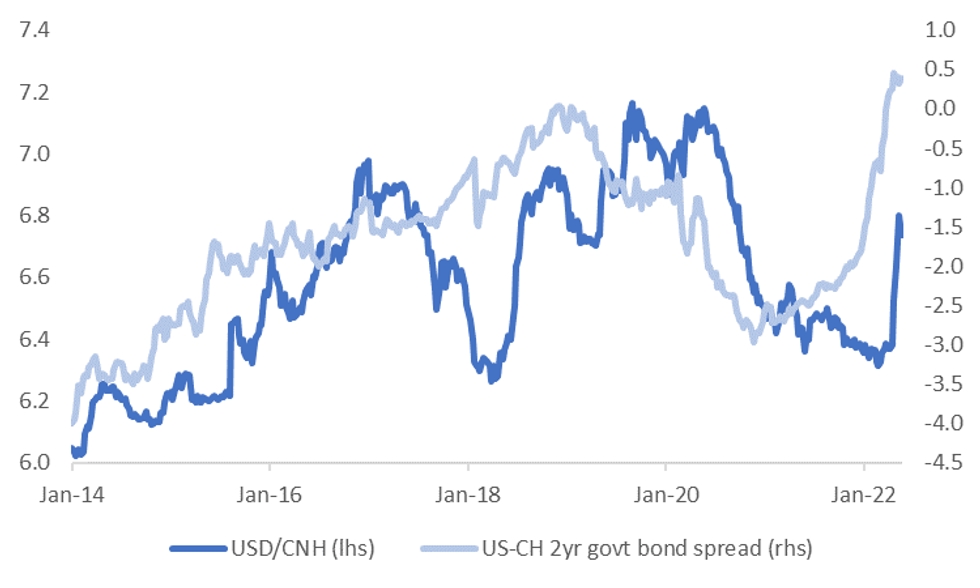

- The second chart below is the US-CH 2yr government bond yield differential overlaid against USD/CNH. The spread has come a long way and Fed hiking expectations have plateaued to a degree, but it is difficult to see the policy bias swinging sharply back in CNH's favor in the near term.

- The authorities also don't appear to be leaning against depreciation pressures strongly either, at least judging by the shift in this week's fixing bias (a point we highlighted in an earlier post).

- Such a backdrop should leave USD/CNH dips well supported, particularly ahead of the 6.7000 level, although as the past week has demonstrated, the broader USD trend remains critical.

- There is still scope for CNY to underperform on a cross basis, given the NEER is elevated by historical standards. Even after the recent correction ( -4%) we are still some 12% above the lows seen in 2020.

Fig 2: USD/CNH & US-CH 2yr Spread

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok