Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CNH

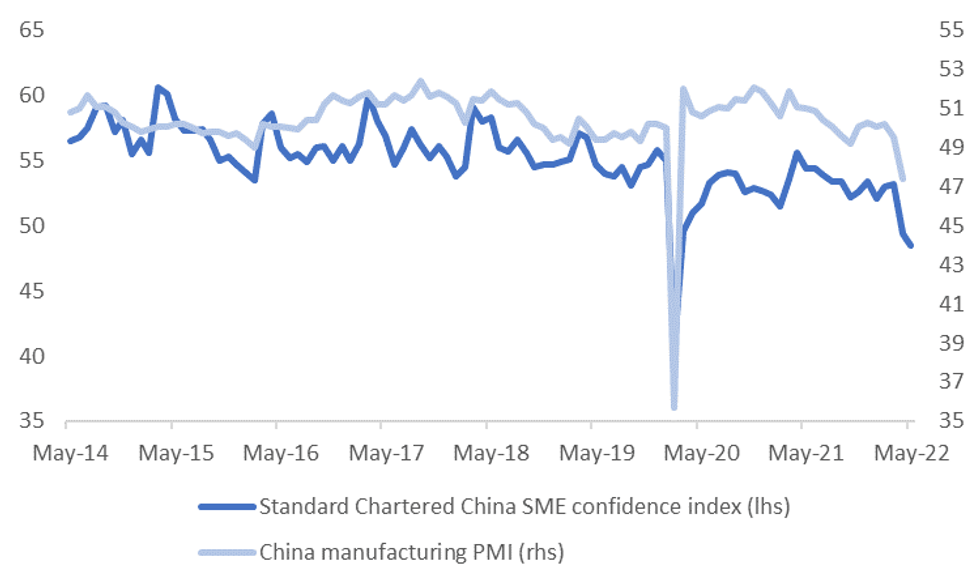

China growth concerns have been front and centre today. The next major data releases are at the end of the month, coming in the form of the PMI surveys. At this stage consensus forecasts point to improvement over the previous month's readings (slower rates of contraction foreseen in the official readings, alongside modest expansion in the Caixin manufacturing reading), but will this be realized?

- The Standard Chartered SME survey, which covers over 500 SMEs, has already printed for May. It showed a further deterioration, coming in at 48.50 from 49.4 in April.

- This doesn't suggest a trough has been reached yet, while the detail was also soft, with new orders dipping to 45.6 (versus 54.6 back in March).

- This survey has a reasonable directional correlation with headline PMI surveys, see the chart below. With the official manufacturing PMI the correlation in the last few years is 67% (using 3 month rates of change in both series).

- If we look at the pre-Covid period the correlation is still a reasonable 48% (from 2014 to end 2019). These correlations are lower for the non-manufacturing PMI. We get higher correlations with the Caixin PMIs but these have a shorter sample period, only since 2019.

- The Standard Chartered SME survey result arguably adds some downside risks to PMI expectations. The clear caveat being that the SoE sector could be doing more heavy lifting at present, which is unlikely to show up in the Standard Chartered survey, but could show up in the official PMI prints.

Fig 1: China Manufacturing PMI and Standard Chartered SME Survey

Source: Standard Chartered/MNI - Market News/Bloomberg

Source: Standard Chartered/MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok