Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CROSS ASSET

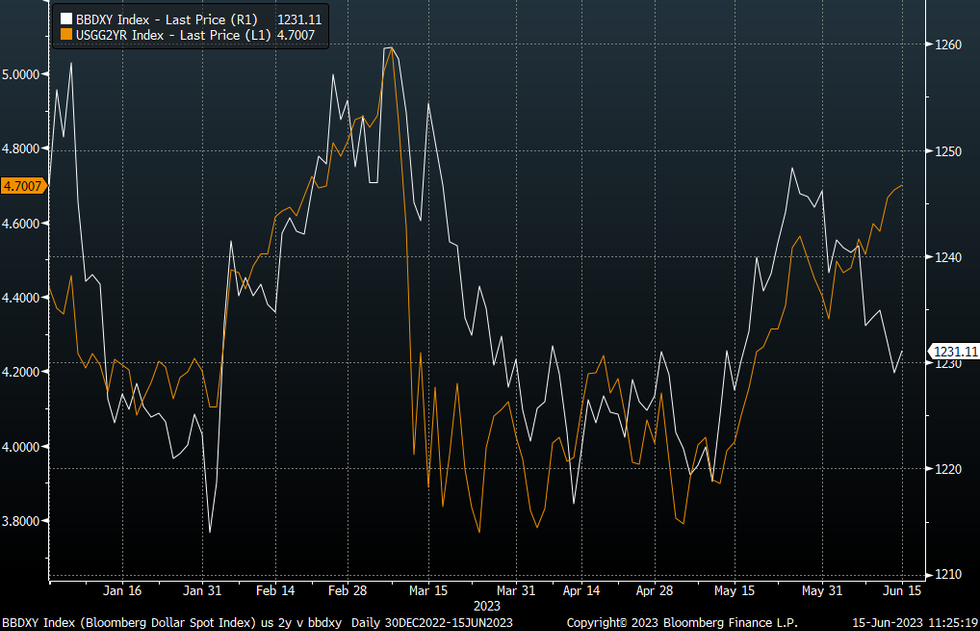

The greenback has been in recent dealing as Asia reacts to yesterdays FOMC meeting and hawkish rates guidance. Spillover into tsys and equities is limited thus far with US Tsy Yields only ~1bp higher across the curve and e-minis flat. Still the BBDXY has lagged this recent run higher in short term US yields, so we may be seeing some catch up from that standpoint.

- The Yen is the weakest performer in the G-10 space at the margins, USD/JPY is up ~0.4% firming above ¥140.50.

- The Antipodeans are pressured, AUD/USD is down ~0.3% and NZD/USD is down ~0.4% as Kiwi extends post Q1 GDP losses.

- A break above 7.1800 in USD/CNH to fresh highs for this cycle is also aiding the broader USD bid. As expected the 1yr MLF rate was cut to 2.65%.

Fig 1: BBDXY Versus US 2yr Government Bond Yield

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok