Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

USD

The USD has moved off cycle highs observed late last week. In this short update we look at the risks surrounding USD performance, particularly against the low yielders/safe havens, with the potential for the USD to be undermined by a run of weaker data outcomes.

- The DXY has eased away from the 105.00 level from late last week and now sits in the low 104.10/15 region.

- Market expectations around Fed policy in early 2023 have remained range bound for much of the past week. As we noted last week, a flatlining of Fed expectations could take away a key source of support for USD/JPY. The subsequent dip in USD/JPY has proven to be fairly shallow though, as better risk appetite in equities has kept yen crosses supported for the most part over recent sessions.

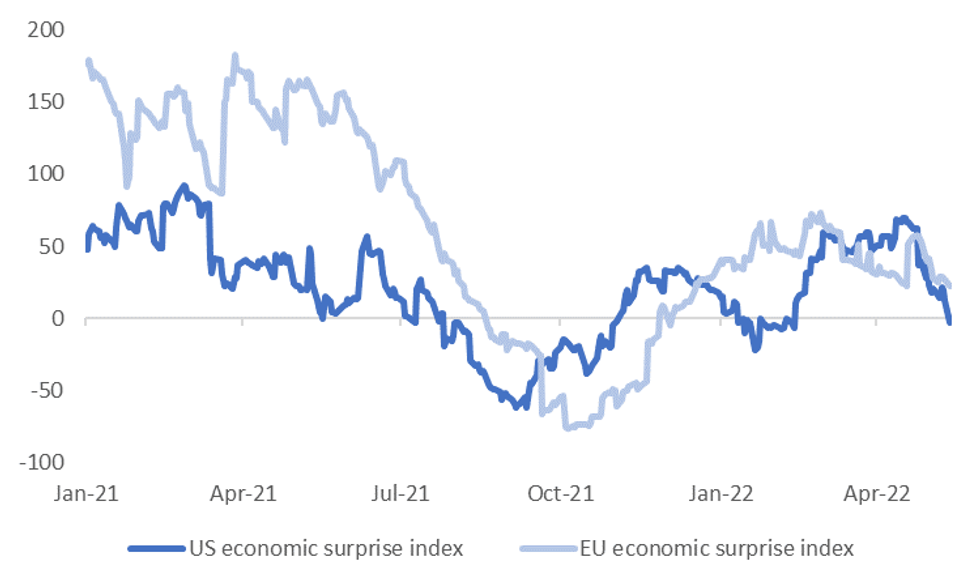

- It is possible a plateauing of Fed expectations is feeding into weaker USD sentiment elsewhere. Last night’s very weak empire manufacturing print helped send the Citi US economic surprise index sub 0. This is the first time we have been below this level since mid February. The US economic surprise index is now falling more quickly than the equivalent EUR measure, see the first chart below.

Fig 1: Citi's US Economic Surprise index Dips Back Below 0

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

- The Empire manufacturing index has a 73% correlation with the US ISM, but we also get the Philly Fed survey later this week (19th), which will provide a further update on the state of business sentiment. There has already been considerable focus on the tightening in US financial conditions and how this will impact US economic activity. The second chart below plots the Goldman’s US financial conditions index against the US ISM.

Fig 2: Goldman's US FCI & US ISM

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

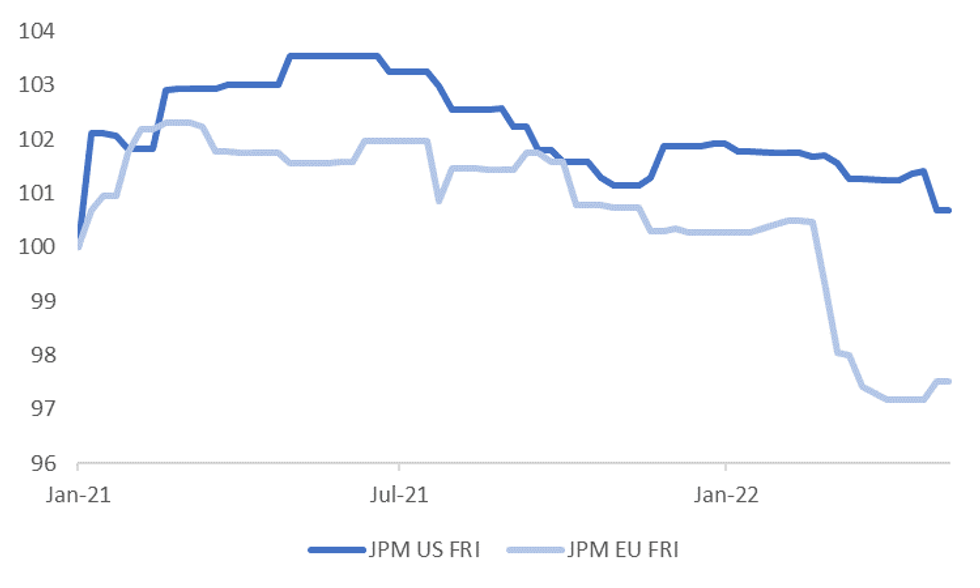

- Year to date, J.P. Morgan economists have revised down their economic projections for the EU area more so than the US, see the third chart below. This is hardly surprising given the Ukraine conflict and its impact on the EU area outlook. Still, if we have a bout downside surprises in US data relative to expectations, will the US growth outlook play catch up to the downside?

- All else equal, if we see US growth expectations being revised down it can act as a cap on market expectations for the Fed, which is a risk to be mindful of in terms of USD performance against the low yielders/traditional safe havens going forward.

Fig 3: J.P. Morgan's Economic Forecast Revision Indices (FRIs)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok