Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

COMMODITIES

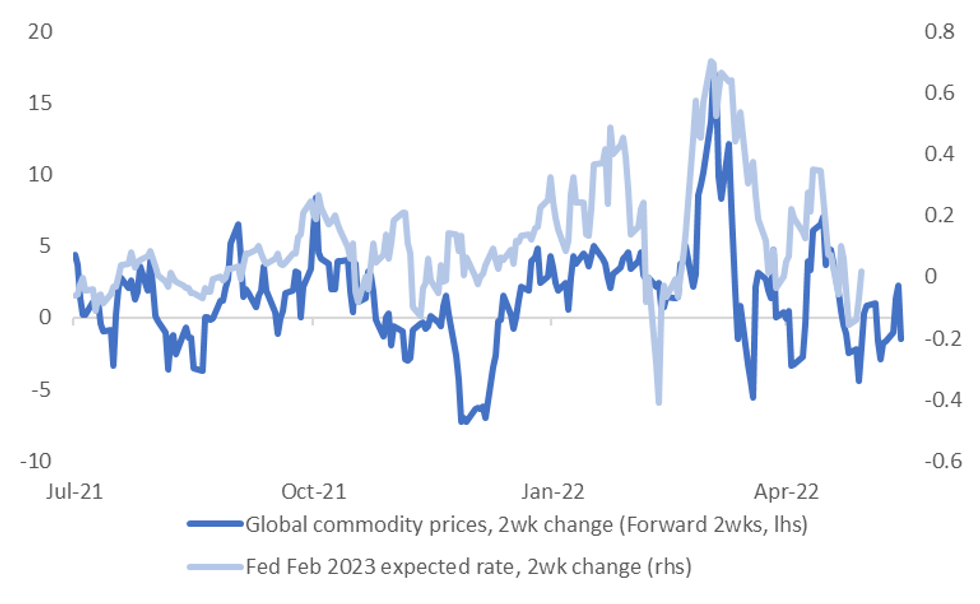

Risks to US data outcomes appear skewed to the downside, which should bias US growth and Fed expectations lower. However, commodity prices are still showing a decent leading relationship over Fed expectations.

- Thursday will likely see the focus for US data watchers fall on the latest Philly Fed survey. The market looks for a 15.0 headline print, versus 17.6 previously. Also out is jobless claims data and existing home sales.

- As we noted earlier in the week, the Citi US economic surprise index is back 0 for the first time since mid February We have stayed below this level even after firmer U.S. retail sales data.

- JPM economists have also revised down their US growth forecasts, citing tighter financial conditions. This will be reflected in the JPM forecast revision index (FRI), which is updated with a lag.

- Waning US growth expectations should flatten out Fed tightening expectations, all else equal, particularly over the medium term.

- However, an important offset in the near term is commodity price action. The chart below overlays the 2 week change in spot commodity prices and the 2 week change in the expected Fed funds rate in Feb 2023.

- Interestingly, the correlation is stronger between the two series when we lead commodity prices by 2 weeks. Since the the start of the year that correlation is 56%.

- Greater downside risks to US/global growth should ultimately weigh on commodity prices, but supply chain pressures, which have become more pronounced in recent months, see this link, are providing an important offset.

Fig 1: Commodity Price Changes & Fed Expectations

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok