Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

USD

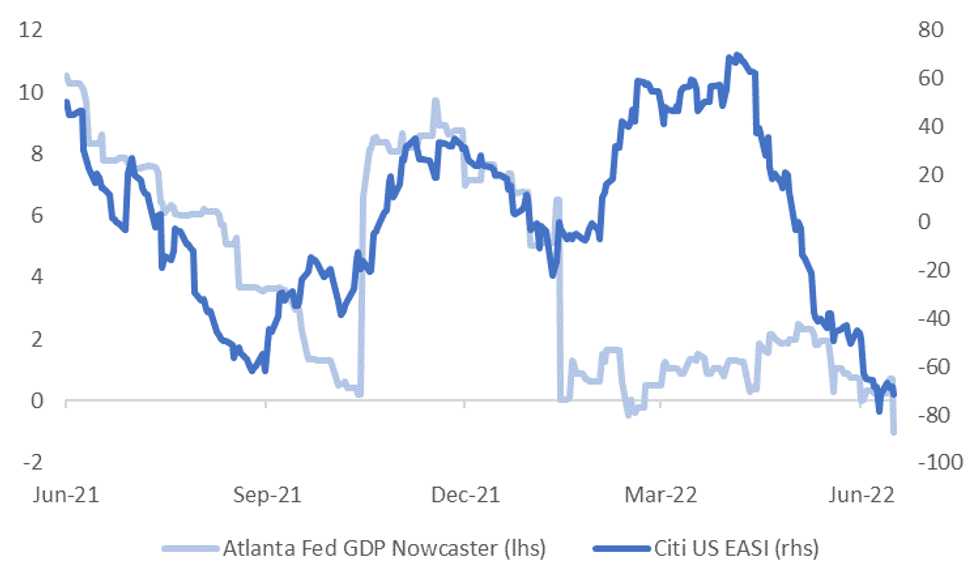

The uptick in U.S. data momentum has proven to be short-lived. The Citi US EASI has rolled back over, although remains above recent lows. Thursday saw a sharp move down in the Atlanta Fed GDP Nowcaster, to -1%, see the first chart below.

- Important data prints continue Friday, with the ISM manufacturing print in focus. Our simple estimate, based off the Philly Fed and Richmond Fed survey readings, remains sub 50 (49.3), even after the Richmond Fed was revised higher for June.

- As we noted last month, the regional Fed surveys have generally been painting a more bearish picture relative to ISM outcomes in recent months. The consensus estimate sits at 54.5. versus 56.1 last month.

Fig 1: Atlanta Fed GDP Nowcaster dips to -1%

Source: Citi, Atlanta Fed, MNI - Market News/Bloomberg

Source: Citi, Atlanta Fed, MNI - Market News/Bloomberg

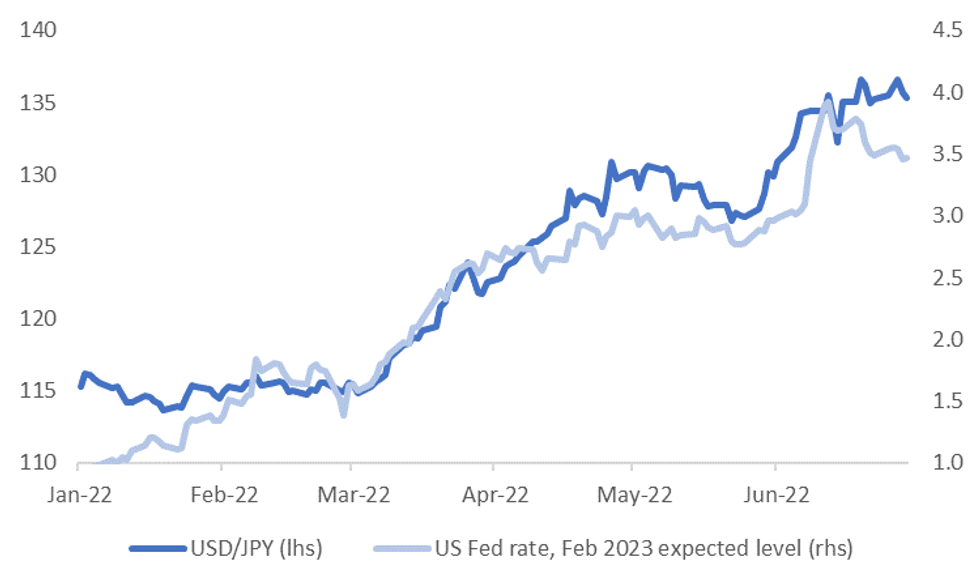

- The impact of weaker data outcomes has been quite clear for US yields. Market pricing for the Fed policy rate is shifting lower, particularly the further we get into 2023.

- Yields have also moved lower elsewhere though. EU-US 2yr spreads are down this week, while steady in terms of UK-US spreads. Not surprisingly, the differential with Japan has contracted.

- The second chart below is USD/JPY versus the expected Fed funds rate in early 2023.

- Even with USD/JPY correcting down from the 137.00 level, it still looks too elevated, at least according to this metric. JPY is outperforming against the rest of G10 FX bloc today.

Fig 2: USD/JPY & Fed Expectations

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok